Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Revenue token meaning, payout routes, and risk checks.

A revenue token is a crypto token whose value is tied to project income through payouts, buybacks, burns, staking rewards, or treasury growth.

The phrase sounds tidy, but crypto rarely gives tidy labels a quiet life. A revenue token can mean a direct revenue share, a fee-funded reward token, a buyback story, a real-yield claim, or a specific asset such as Revenue Coin RVC.

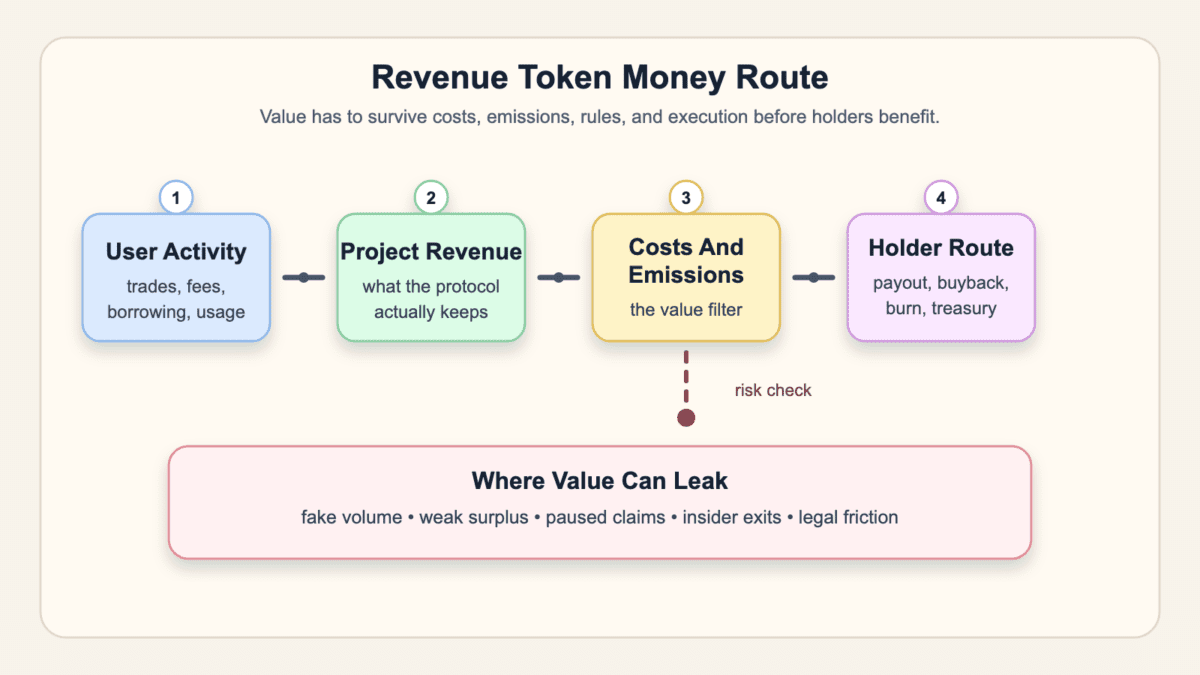

So the useful question is not only what the token is called. It is whether real revenue reaches holders after costs, emissions, lockups, governance votes, and legal limits. Trace that route before a shiny payout story gets your wallet involved.

A revenue token in crypto usually means a token whose value story depends on income from a project, protocol, app, asset, or service. That income may reach holders directly, or it may support the token through buybacks, burns, staking rewards, or treasury growth.

Projects use the label loosely, so the mechanism matters more than the name. A revenue token can describe several routes:

The same phrase can point to a broad tokenomics label, an explicit revenue-sharing token, a revenue participation token, a real yield token, or a token tied to one product’s income.

That difference is more than wording. It changes what you are buying. A token can be linked to revenue without giving you a legal claim on income. It can also have protocol fees without sending value to tokenholders.

It also does not prove several things:

Use a simple plain-English check: find the money, then follow it. If the route stops at a treasury, a governance promise, or a vague “future utility” line, the revenue token claim still needs proof.

A revenue token sends value to holders only when project income moves through a clear holder route. That route can be a payout, a claim, a staking reward, a buyback, a burn, or an indirect treasury policy.

Direct payouts are the clearest route. A project earns revenue, subtracts costs, and sends a defined share to eligible holders. That can feel closest to a dividend, but the legal and technical setup decides the rights.

Claimable rewards add more steps. A holder may need to stake, lock, vote, meet KYC rules, pay gas, claim within a window, or approve a contract. When that happens, careful wallets and approval hygiene become part of the revenue route, not a side quest.

Buybacks and burns are more indirect. The project uses revenue to buy the token, burn supply, or add treasury support. That can help holders if the buying is real, repeatable, and large enough to matter against sell pressure.

The checks change by route:

| Route | What The User Should Check |

|---|---|

| Direct payout | Who is eligible, which asset pays, and what rule controls the share? |

| Staking reward | Does the reward come from revenue or new token emissions? |

| Buyback | Is the buyback onchain, recurring, and funded by actual surplus? |

| Burn | Does lower supply offset emissions, unlocks, and weak demand? |

| Treasury accrual | Can holders benefit, or does value stay trapped in governance? |

| Fee switch | Is the switch active, or only a future vote? |

The table hides one ugly detail: each route can fail quietly. A payout can pause. A buyback can shrink. A burn can be cosmetic. A treasury can grow while tokenholders see nothing.

That is why a promise to share revenue is not the same as money arriving in your wallet.

Revenue token, revenue-sharing token, and revenue participation token are related terms, but they do not always describe the same legal or technical model. The difference comes down to how explicit the revenue link is.

A revenue token is the broadest phrase. It can mean almost any token whose value story depends on project income. A revenue-sharing token is usually more direct because it suggests that some revenue or fees are shared with holders.

A revenue participation token often appears in glossary-style explanations for a narrower model where holders participate in a defined revenue stream. That still does not create one universal rule. Crypto projects, tokenized asset issuers, DeFi protocols, and creator-economy platforms can use similar phrases for very different structures.

| Term | Plain-English Difference |

|---|---|

| Revenue token | Broad label for a token linked to project income or fee capture. |

| Revenue-sharing token | More explicit claim that revenue or fees flow to holders. |

| Revenue participation token | Often framed as holder participation in a defined revenue stream. |

| Real yield token | Usually points to rewards funded by earned fees or income. |

| Governance token with fees | May depend on a vote, fee switch, or treasury policy. |

Read the label last, not first. A “revenue-sharing token” with no active payout can be weaker than a boring token with a live buyback policy.

A “revenue participation token” may require contracts, offchain records, or transfer limits that do not appear in a price chart. Labels help you sort the claim. Documents, contracts, dashboards, and distributions tell you what exists.

Revenue token and real yield overlap when holder rewards come from actual protocol revenue or fees. They separate when the token depends on emissions, future governance, or vague value capture instead.

Real yield in DeFi usually means yield backed by economic activity. Traders pay fees, borrowers pay interest, validators earn rewards, or users pay for a service. Those flows can fund rewards without leaning mostly on freshly issued tokens.

A revenue token can produce real yield when earned revenue funds its payout route. But a revenue token can also rely on buybacks, burns, treasury growth, or a fee switch that has not turned on yet. That is why farming rewards and APY language need a source check before the rate earns trust.

Use the split below when a token pitch talks about revenue and yield in the same breath:

| Revenue-Backed | Emissions-Backed |

|---|---|

| Rewards come from fees, interest, or project income. | Rewards come mainly from new token supply. |

| Payout depends on usage and surplus. | Payout depends on incentive budgets. |

| Lower revenue can reduce rewards. | Lower token price can crush APY value. |

| Holders can trace who paid. | Holders may only see who got diluted. |

| Sustainability depends on demand. | Sustainability depends on continued issuance. |

Neither side is automatically good or bad. Emissions can bootstrap a new market. Revenue can also fall when volume fades. The point is to know which engine is paying.

If a revenue token uses both revenue and emissions, separate them. A 20% displayed reward funded half by fees and half by new supply is a very different beast from a 20% reward fully funded by surplus. Same number, different teeth.

A revenue token is not automatically a dividend, stock, or equity claim because token rights depend on structure, documents, jurisdiction, and how value reaches holders. Similar cash-flow language can hide very different rights.

The instinct makes sense. If a project earns money and sends some of it to tokenholders, that can look like a dividend. If a token gets buybacks, it can feel like shareholder value. If a DAO controls a fee switch, it can sound like public-company governance after three coffees and a Discord vote.

But equity has legal rights that a crypto token may not have. Shareholders may have rights around ownership, voting, disclosure, transfer, and remedies. Tokenholders might have governance votes, contract claims, revocable rewards, offchain eligibility rules, or no direct claim at all.

The SEC staff statement on tokenized securities keeps the warning narrower: structure and holder rights still matter, and a token wrapper does not skip securities-law analysis.

For buyers, this is not a legal conclusion. It is a narrower warning. Do not assume revenue wording gives you ownership. Check what the token actually grants:

Tax treatment can also change by country and structure. A payout, a staking reward, a token burn, and a capital gain may not land the same way. “Not tax advice” is a boring sentence, but here it earns its keep.

When a revenue token starts sounding like stock, slow down. The closer the claim gets to income rights, profit share, or tokenized securities, the more the fine print has to carry.

To check whether a revenue token has real revenue, trace the source, the accounting, and the holder route before looking at price or APY. Fees alone are not profit, and profit alone is not tokenholder value.

Start with the revenue source. A credible claim should name who pays and why. Traders may pay fees, borrowers may pay interest, or users may pay for storage, compute, games, creator content, data, or another service. If the answer is only “community demand,” keep digging.

Then separate gross fees from net surplus. A protocol can collect large fees while paying most of them to liquidity providers, validators, affiliates, creators, or service operators. Tokenholders may receive a leftover amount, a fixed share, or nothing.

Run this checklist before buying, staking, or locking:

That last point is where bagholder risk enters. A revenue narrative can attract late buyers after earlier holders have already gained from points, airdrops, private rounds, or cheap supply. The project may still be real, but your entry can be late.

Transparency also has levels. Public dashboards help, but they are not enough if the definitions are vague. “Revenue” can mean gross fees, net protocol revenue, treasury income, creator revenue, or something else. Use the project’s definition, then test whether value actually reaches holders.

A good revenue token should make the value route easier to explain over time. If each update adds a new reward layer, new lockup, new token, and new exception, the math may be getting foggier instead of stronger.

Revenue token risks begin when the story moves faster than the money route. A project can have real fees, impressive dashboards, and active users while the token still loses value.

Fake or circular revenue is the first risk. A project can generate activity through incentives, wash-like behavior, referral loops, or mercenary farming. If users only show up because rewards exceed costs, the revenue can vanish when the subsidy stops.

Emissions are the next leak. A token can receive buybacks or payouts while new supply, insider unlocks, or reward emissions create stronger sell pressure. In that case, revenue is a bucket under a leaking roof.

Execution can also fail. Admin keys, upgradeable contracts, oracle issues, bridge risk, paused claims, delayed buybacks, and changed reward rules can all break holder value. Revenue does not protect you from bad plumbing.

Liquidity adds another problem. A polished revenue story can pull in late buyers who become exit liquidity for earlier holders. The chart may look clean until sellers test the order book.

Quiet failure is often harder to spot than a dramatic collapse. A project may stop updating dashboards, reduce distributions, delay fee switches, or bury buyback changes in governance chatter. That pattern can become soft-rug risk when promises fade without one obvious exploit.

Keep these weak spots in view:

> If you cannot see where the yield comes from, you may be standing closer to the yield source than you think.

That line is not a law of markets. It is a useful smell test. If the answer to “who pays?” is unclear, do not let the revenue token label do the thinking.

Revenue Coin RVC is not the same thing as the broad revenue token concept. RVC is a specific asset that can appear on price pages, while “revenue token” is a category-like phrase used for several value-capture models.

That name collision can confuse users fast. One tab may show a price page for Revenue Coin. Another may explain revenue-sharing tokens. A third may discuss real yield in DeFi. They are not answering the same question.

Use this split when the results page mixes both ideas:

If you are researching RVC, check RVC-specific sources for its contract, network, liquidity, supply, exchange support, and current market data. Live price, market cap, and volume need fresh data, so this guide does not hardcode them.

If you are researching revenue tokens as a concept, keep RVC separate. The useful lesson is not whether one asset uses the word “revenue.” It is how any token claims to connect revenue to holders.

That distinction protects you from a common mistake: buying one coin because you wanted to understand a mechanism. Crypto has enough ways to confuse a wallet without letting a mixed set of tabs add bonus damage.

The quick fix is dull but effective. Look up the token contract or ticker when you mean RVC. Look up the mechanism, payout model, and revenue route when you mean the broader revenue token idea.

Revenue token research gets easier once the nearby concepts are separated. Bad decisions often start when several tokenomics ideas get squeezed into one comfortable label.

Governance tokens are related because many revenue routes depend on votes. A DAO may control a fee switch, treasury spending, emissions, or buyback policy. That can create value, but it can also keep value stuck behind politics.

Real yield is related because it asks whether rewards come from earned revenue instead of token inflation. Token emissions are related because they can dilute holders even while payouts look healthy.

Buybacks and burns are related because they can route revenue back into the token without direct payouts. Lockups and veToken models are related because they can decide who receives rewards and who carries exit risk.

Two CryptoProcent guides are worth keeping close:

Keep the other concepts separate in your own notes. Governance decides rules, real yield tests reward source, emissions show dilution, and lockups show who can leave. The goal is to stop one useful word from carrying five different promises.

A revenue token is not automatically the same as a dividend token. Some revenue tokens may send payouts to eligible holders, but others use buybacks, burns, staking rewards, treasury growth, or governance-controlled fee switches. The exact rights depend on the token structure and documents.

A revenue token can make money for holders through direct payouts, claimable rewards, buybacks, burns, or indirect treasury support. The key check is whether project revenue actually reaches the holder route after costs, emissions, eligibility rules, and execution risk.

Yes, a revenue token can lose value even when a project earns revenue. Token price can fall because revenue shrinks, emissions dilute holders, insiders sell, liquidity thins, claims pause, legal risk rises, or the market decides the value route is weaker than advertised.

A revenue token is a token whose value story is tied to project income. Real yield describes rewards funded by actual fees, interest, or cash flow instead of mainly new token emissions. A revenue token can produce real yield, but only when the payout source is real revenue.

Revenue Coin RVC is a specific asset, while a revenue token is a broader concept. If you are checking RVC, use RVC-specific data. If you are learning the concept, focus on how any token routes revenue to holders.

Revenue tokens are not all securities, but some structures can create securities-law questions. Explicit income rights, profit sharing, tokenized equity, transfer limits, and contractual claims can change the analysis. Read the documents and get qualified advice when the legal rights are unclear.

Start with the revenue route before you look at the chart. A revenue token only becomes useful when you can explain who pays, what the project keeps, and how any value reaches holders.

Keep the first pass small. You are not trying to value the entire protocol on day one. You are trying to reject weak claims before they turn into expensive curiosity.

Use this order:

Then look for the boring answer. If the route is clear, the token may deserve deeper research. If the route depends on future votes, fuzzy dashboards, or faith in buybacks that never happen, the label has not earned your risk.

Sizing comes after that. A tiny test position can still be too large if the token is illiquid, the claim route is confusing, or the exit depends on one thin venue. A clean revenue story should reduce uncertainty, not ask you to pretend it vanished.

Write down the first failure point before you act:

A good revenue token should make the money route easier to inspect. A weak one asks you to admire the word “revenue” and stop asking where it goes.