Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A plain-English guide to RFQ trading in crypto.

RFQ means request for quote. In crypto trading, it is a workflow where you ask liquidity providers for a firm or time-limited price before accepting a specific trade.

Outside trading, RFQ can mean procurement paperwork or a request for qualifications. In crypto, the useful meaning is trading-specific. You ask for a price first, then decide whether the quote is good enough to accept.

That sounds simple. The trap is in the details. RFQ can help with large trades, thin liquidity, options, OTC desks, and DeFi routes, but only when you understand quote expiry, spread, settlement, and who stands behind the price.

RFQ in crypto trading means asking for a quote on a specific trade before sending the order for execution. You define what you want to buy or sell, the size, and sometimes the venue, settlement asset, or expiry window.

The person asking is usually called the requester, taker, client, or trader. The responder is usually a market maker, liquidity provider, dealer, or trading desk. The venue can be a centralized exchange, OTC platform, prime broker, DeFi protocol, DEX aggregator, or API layer.

The quote is the price offered for that exact trade. It may be firm, which means it can be accepted under the platform’s rules before expiry. Or it may be indicative, which means it is more of a price estimate than a tradable commitment.

The quote window is short for a reason. Markets move. A provider does not want to promise a price forever while BTC, ETH, funding rates, or options volatility runs away in the background. Crypto is not famous for waiting politely.

A clean example: a trader wants to sell 20 BTC into USDC without walking through a public order book. The trader sends an RFQ. Several liquidity providers return prices. The trader compares the all-in result, accepts the best valid quote, or lets the request expire.

That is different from clicking a market order. A market order takes available liquidity immediately. An RFQ asks, “What price will you give me for this whole trade right now?” That distinction is the point.

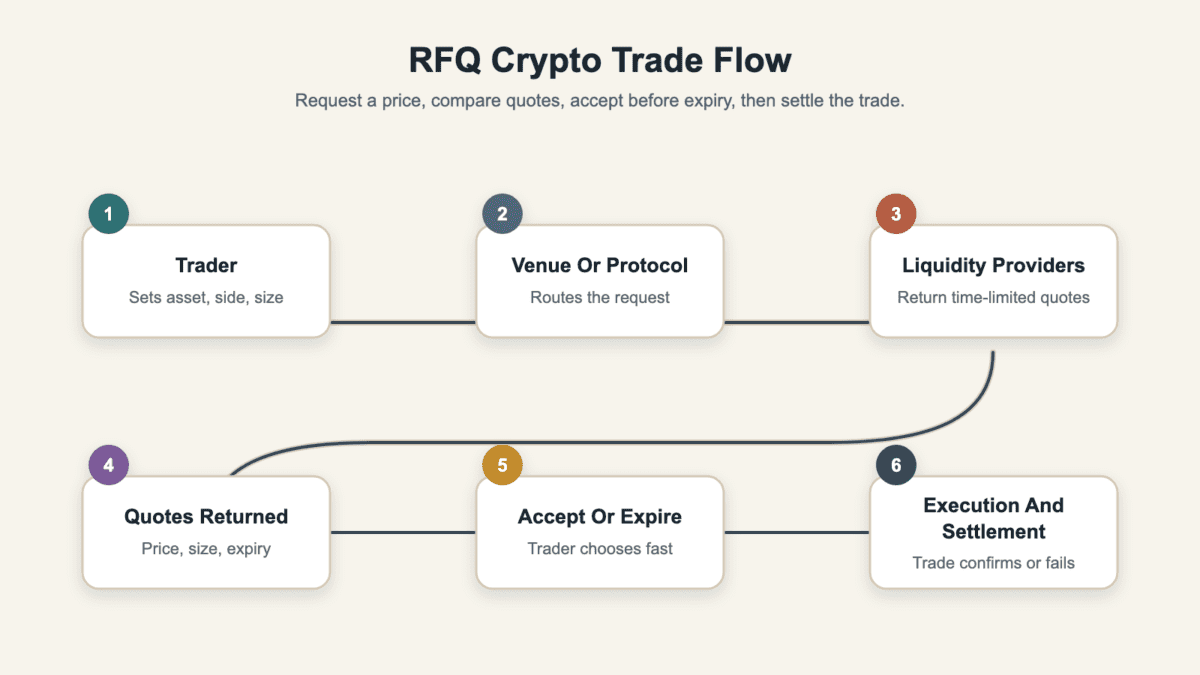

An RFQ crypto trade works by turning one intended trade into a short quote request before execution. The trader sends details, providers answer, and the trader accepts a quote or lets it expire.

A centralized example is Coinbase Exchange, where an eligible RFQ order moves through a request, provider quotes, acceptance or rejection, expiry, and fill notification. Other venues can use different rules, but the core flow is similar.

The sequence usually looks like this:

That flow can be fast. The quote may last only a few seconds, depending on the asset and venue. Read the expiry before you trust the number.

After acceptance, the platform rules matter. Some RFQ products fill immediately. Some need settlement steps. Others may reject, cancel, or fail. Common causes include quote expiry, insufficient margin, compliance blocks, or a liquidity provider that cannot complete the fill.

So RFQ is not only “get a price.” It is request, quote, accept, execute, and settle. Each verb has its own failure mode.

RFQ shows up wherever a trader needs a quoted price for a specific crypto trade instead of blindly taking the next available pool or order-book price. That can happen on centralized venues, on-chain routes, institutional desks, retail tools, or APIs.

The common thread is control. RFQ is useful when trade size, complexity, liquidity, or privacy makes a simple market order too blunt. A tiny ETH swap does not need a dealer parade. A block trade, options structure, or thin pair might.

Centralized exchange RFQ appears inside exchange tools that route quote requests to approved liquidity providers. The exchange sits between the trader and the responders, then applies its own rules for eligibility, expiry, execution, and reporting.

This setup can suit larger spot trades or accounts that already meet venue requirements. It may also require account access, API setup, support approval, or higher account tiers. The user sees a clean quote screen, but the venue still controls the rulebook.

OTC and prime brokerage RFQ is often used for larger trades, treasury moves, custody-linked flows, and institutional execution. The trade may not touch a public order book in the same way a normal market order does.

Kraken, Coinbase Prime, Binance OTC, and similar services are common examples of the category. No single venue is the answer by default. OTC RFQ usually combines price, relationship, compliance, custody, and settlement into one workflow.

Options and multi-leg RFQ helps when one simple order cannot express the trade. A trader may want a strike, expiry, direction, settlement asset, and combined package price instead of several separate fills.

This is why RFQ appears in options products and structured trading screens. It lets responders quote the whole structure. That can reduce legging risk, but it also means the trader must understand margin, expiry, and payoff before accepting.

On-chain RFQ and DEX aggregator routes use market-maker quotes inside a DeFi swap flow. Instead of relying only on AMM pools, the route may ask professional liquidity providers for a price, then settle through a smart contract.

0x-style RFQ routes, Jupiter-style RFQ tabs, and intent-based fills sit in this family. The user still needs to check the wallet signature, minimum received, chain, token contract, and failed transaction behavior. “On-chain” does not mean “free of homework.”

RFQ is one execution route, not a universal upgrade. Compare it by what the trade needs: speed, price certainty, public liquidity, private negotiation, automation, or control over the final fill.

Different routes solve different problems. A deep order book may beat RFQ for a small trade. An AMM can be cleaner for a simple on-chain swap. A limit order may be best when time is not urgent.

| Route | Best Fit And Trade-Off |

|---|---|

| RFQ | Best for specific size, thin liquidity, block trades, options, and quotes that must be accepted before expiry. The trade-off is reliance on venue rules and responder quality. |

| Public Order Book | Best for visible bids, asks, depth, and active price control. The trade-off is market impact when your order eats through thin levels. |

| AMM Swap | Best for simple on-chain swaps with available pool liquidity. The trade-off is pool price impact, slippage settings, and public transaction exposure. |

| OTC Desk | Best for larger relationship-driven trades, settlement help, or negotiated execution. The trade-off is less transparent comparison unless you request multiple quotes. |

| Convert Tool | Best for small, fast account-balance conversions. The trade-off is hidden spread and limited control over execution details. |

| TWAP Execution | Best for splitting size over time. The trade-off is time risk if the market moves against the schedule. |

| Limit Order | Best when you know your price and can wait. The trade-off is no guaranteed fill. |

Use RFQ when the quote has a real reason to exist. That reason might be size, complexity, weak public depth, or a need for one all-in price. If the route is only hiding the spread behind a tidy screen, slow down.

The best trade path is usually the one you can explain before clicking. If you cannot say where the price came from, when it expires, and what happens after acceptance, the route is still a black box.

RFQ can help with slippage, market impact, and MEV by moving price discovery away from a fully public, immediate trade path. Instead of crossing the visible book or hitting an AMM pool at once, the trader asks for a quote first.

That can reduce some ugly outcomes. A large market order may walk through several order-book levels. A big AMM swap may move the pool against itself. A public on-chain transaction may reveal size, route, and slippage tolerance before settlement.

RFQ can reduce those problems when the provider quotes the whole trade and holds the price long enough for acceptance. It can also help when a DEX route uses private or quoted liquidity instead of exposing every detail to the public mempool.

But RFQ does not remove slippage by magic. It changes where the price risk lives. The spread may already include the provider’s risk. The quote may expire. The trade may still settle through a route with its own failure points.

When liquidity is thin, a careless trader can become someone else’s exit liquidity even with a quote on screen. RFQ can improve the process, but it cannot make a bad counterparty generous.

Keep the warning narrow: RFQ can reduce visible market impact in some workflows, but it does not guarantee the best price, full privacy, or MEV-proof execution. Check the quote against another route before you accept meaningful size.

RFQ does not fix counterparty risk, venue risk, custody risk, or unclear settlement rules. It gives you a quoted trade path. It does not turn every responder into a saint with a matching engine.

The first risk is quote quality. A firm quote is stronger than an indicative quote, but only inside the rules of that platform. If the screen does not show expiry, all-in price, minimum size, or settlement behavior, you are accepting more uncertainty than the acronym admits.

The second risk is the counterparty. A liquidity provider quotes because it expects to earn spread, manage inventory, or win flow. That is normal. But crypto can turn into PVP trading when users forget the other side has incentives too.

Custody is another blind spot. Some RFQ trades settle inside a centralized account. Others involve wallets, smart contracts, custody accounts, or transfers after the trade. If the path touches self-custody, the wallet custody step still deserves attention.

Watch for these risk signals before you accept:

KYC, KYB, jurisdiction, margin, and account-tier rules can also decide access. An RFQ screen may appear simple, but the back office can still say no. That is not a bug. It is part of the venue model.

The takeaway is narrow. RFQ can improve execution in the right setting, but it does not replace due diligence on the venue, quote, counterparty, custody path, and settlement record.

Check an RFQ before you accept by confirming the trade details, the quote quality, and the settlement path while the quote is still valid. Speed helps only after the basics are correct.

Start with the asset, side, amount, and settlement currency. A quote to sell BTC for USDC is not the same as a quote to sell BTC for USD, stablecoin basket settlement, or a derivatives payoff. Small mismatches can become expensive fast.

Then compare the quote against another route. Look at a public order book, AMM quote, convert screen, or another provider when available. You are not looking for a perfect match. You are checking whether the RFQ price is reasonable after spread, size, and fees.

The practical checklist is short enough to use:

For DeFi RFQ, add wallet-specific checks. Confirm the token contract, route, signing message, minimum received, gas cost, and failed transaction behavior. A quote can look clean while the signature asks for something sloppy.

For options or structured products, add payoff checks. You need strike, expiry, settlement, margin, and combined package behavior. The quote may cover the price, but it cannot teach the payoff after you already clicked.

The best RFQ habit is boring: compare, read, accept only inside the window, and keep the record. Boring is underrated when the alternative is learning settlement mechanics during a support ticket.

RFQ is not worth it when the trade is small, liquid, simple, or better served by a normal order type. If the public route is clear and cheap, an RFQ can add steps without adding value.

Small liquid trades are the obvious case. If BTC or ETH has deep order-book liquidity for your size, a limit order or careful market order may be simpler. If an AMM pool is deep enough for a modest swap, a normal aggregator route may be fine.

Tiny balances are another poor fit. RFQ is usually overkill for dust-sized balances where fees, minimum trade size, or quote overhead matter more than execution improvement. If the fee or minimum order size is larger than the execution benefit, the quote has already lost.

RFQ is also weak when the platform hides too much. If you cannot see quote expiry, spread, provider context, failed-fill behavior, or settlement details, the workflow may be giving you less control than a plain limit order.

Skip RFQ when these simpler routes already solve the job:

Use RFQ when it solves a real execution problem. Skip it when the trade is routine, the route is already clear, or the quote screen asks for trust without giving you enough detail back.

RFQ sits near several crypto market-structure terms. Knowing the adjacent language helps you read the quote screen without treating every label as a mystery button.

A market maker is a participant that quotes prices and manages inventory. A liquidity provider is the broader role that supplies tradable liquidity. In many RFQ workflows, those are the responders giving you a price.

OTC means over the counter. It is a trading channel where larger or negotiated trades happen away from a standard public order book. RFQ can be part of OTC, but RFQ is the quote workflow. OTC is the venue or service model.

CLOB means central limit order book. It lists bids and asks, then matches orders by venue rules. AMM means automated market maker. It prices swaps through pool math rather than a visible bid-ask book.

Fill-or-kill means the order must fill completely or cancel. Spread is the gap between the provider’s buy and sell economics. Settlement is the final movement or accounting of assets after execution.

Two adjacent terms help with judgment. In thin markets, PVP trading is the reminder that the other side has incentives too. For tiny leftovers, dust in crypto explains why some balances are too small for quote hunting.

On-chain RFQ adds smart contracts and wallet signatures to that vocabulary. The quote may come from a market maker, but the final act still depends on chain, contract, gas, and signing details.

RFQ in crypto means request for quote. It is a trading workflow where you ask one or more liquidity providers for a price on a specific trade, then accept the quote or let it expire.

RFQ means request for quote in trading. It usually means the trader asks a dealer, market maker, or liquidity provider for a quoted price before deciding whether to execute the trade.

RFQ is not the same as OTC trading. RFQ is the quote request workflow. OTC is a trading channel, often used for larger or negotiated trades. Many OTC desks use RFQ, but RFQ can also appear on exchanges, DEX aggregators, and API routes.

RFQ does not remove slippage in every case. It can reduce quote drift or visible market impact when a provider gives a firm, time-limited price. But the spread, quote expiry, venue rules, and settlement path still decide the real result.

Yes, an RFQ can fail after acceptance if the quote expired, account checks fail, margin is insufficient, settlement breaks, the venue rejects the fill, or the platform rules allow cancellation in that situation. Read the product rules before using serious size.

Yes. On-chain RFQ usually involves wallet signatures, smart contracts, gas, token approvals, and blockchain settlement. Exchange RFQ usually settles inside a centralized venue account. Both use quotes, but the execution and custody paths are different.

Start with RFQ only when it solves a real trade problem: size, thin liquidity, complex structure, quote certainty, or a route where public execution could be costly. Do not use it because the acronym sounds professional.

Test the workflow with a smaller amount when the venue allows it. Compare the quote against a normal order book, AMM route, or convert screen. If RFQ does not improve the all-in result, the simpler path may be better.

Then slow down at the exact moment the interface tries to speed you up. Quote timers can make a normal check feel urgent. That helps the provider. Your job is to know what you are accepting before the timer starts shouting.

Use this final check before accepting:

For larger trades, add a second pass after the fill. Compare the execution report with the quote, confirm settlement, and record any support path. A clean RFQ process should leave a trail you can understand later.

If you cannot verify the quote, route, or settlement path, wait. The best RFQ trade is not the fastest click. It is the one where the price, rules, and risks are clear before the timer runs out.