Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A plain-English guide to concentrated liquidity, fees, ranges, and LP risk.

Concentrated liquidity is a decentralized exchange pool design where liquidity providers choose the price range where their capital stays active.

That design can make swaps cheaper near the current price because more liquidity sits where trades actually happen. But it also turns liquidity provision into active market work, where range choice, volume, price movement, and rebalancing decide whether the fees were worth it.

Concentrated liquidity means LP capital is placed inside a chosen price band. A liquidity provider, often shortened to LP, supplies two assets to a decentralized exchange pool and chooses where that capital should work.

That active range is the part beginners should not skip. A full-range pool may be simpler because the LP does not express a tight price view. Concentrated liquidity asks the LP to pick where trading is likely to happen, then accept the result when price moves away from that guess.

This is different from generic “more liquidity.” The key word is active. Capital only helps traders and earns pool fees while the market price sits inside the LP’s selected range.

Think of it as assigning capital to a working zone inside the pool. Traders get useful depth only where LPs have placed active liquidity. LPs get fee exposure only while their chosen band is being used.

That makes concentrated liquidity a pool mechanic, not a market slogan. It does not mean one protocol controls most liquidity, and it does not mean “exit liquidity.” It means a specific LP position has boundaries.

Keep three distinctions separate:

A simple example helps. An ETH/USDC LP might decide most trading will happen between $3,000 and $4,000 per ETH. Inside that band, the LP’s capital supports swaps and can earn fees. Outside it, the position becomes inactive until price returns or the LP adjusts it.

The promise is capital efficiency with a steering wheel attached, not free yield. The steering wheel is useful only if the driver knows the road, the fuel cost, and when to pull over.

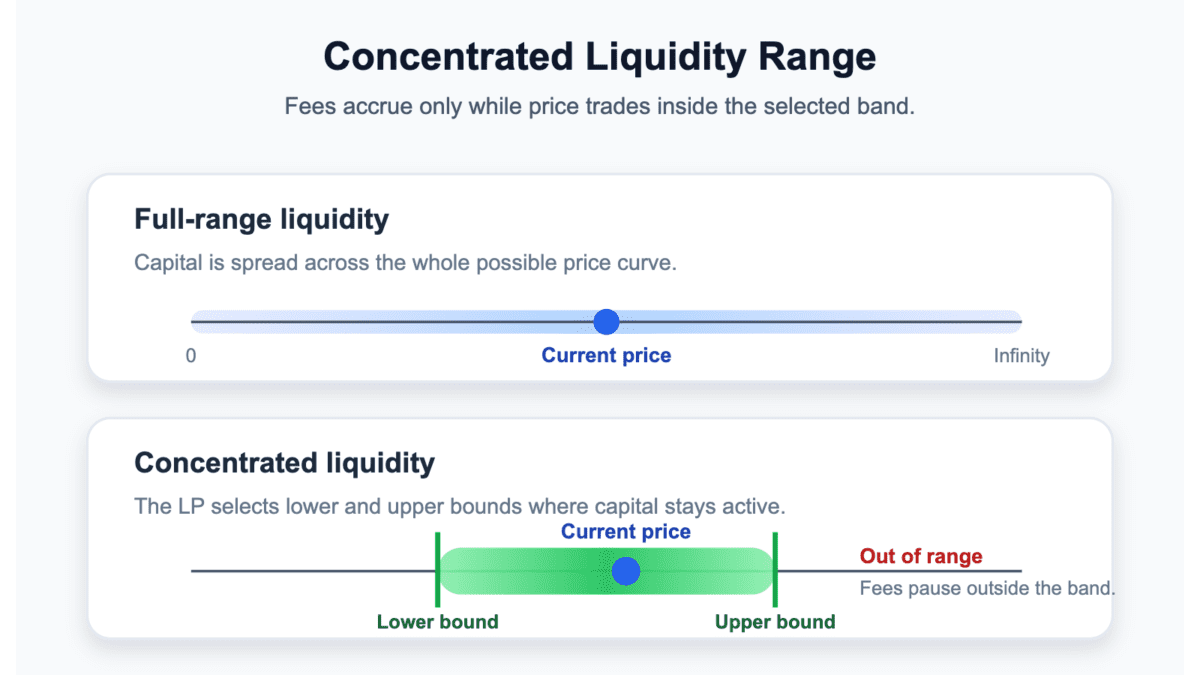

Concentrated liquidity works by letting LPs choose a lower and upper price bound for a position. While the pool price trades between those bounds, the position is active and can earn swap fees.

In a full-range AMM, liquidity is spread across all possible prices. That makes the position simpler, but a lot of capital may sit far from normal trading. In the Uniswap model, Uniswap Developers describes concentrated liquidity as capital allocated inside custom price ranges, with inactive liquidity outside the chosen interval.

The position life cycle is short, but each step matters:

Ticks and bins are protocol words for price steps. You do not need the math first. You need the behavior.

The labels translate cleanly:

A tick-based pool divides price into small steps, then lets LPs choose boundaries. A bin-based pool groups liquidity into discrete price buckets. Both are ways to answer the same practical question: where should this capital be available for trades?

When price moves through the selected band, the pool gradually swaps one side of the pair into the other. That is why concentrated liquidity can feel odd to beginners. The dashboard may show a pool position, but the economic exposure is changing under the hood.

Concentrated liquidity and full-range liquidity solve the same pool problem with different tradeoffs. Full range is broader and usually easier to maintain. Concentrated liquidity is more targeted and more sensitive to price movement.

In a literal full-range setting, the LP covers the entire possible price curve. That can be blunt, but it is easy to understand. The position stays available across the pool instead of switching off when price leaves a narrow band.

Concentrated liquidity gives up that simplicity for focus. The LP tries to place capital where trades are likely to happen. If the range is right and volume is real, the same deposit can do more work. If the range is wrong, the position can sit inactive while the market keeps moving.

| Choice | Main Tradeoff |

|---|---|

| Full-range liquidity | Lower maintenance, but capital may sit far from normal trading activity. |

| Wide concentrated range | More active coverage, but usually less fee density than a tight range. |

| Tight concentrated range | Higher fee density if price stays inside, but more rebalancing risk. |

| Multi-range setup | More control, but more monitoring and recordkeeping. |

The beginner mistake is assuming concentrated automatically means better. Concentrated means narrower. Narrower can be useful when the LP has a clear range view, enough trading volume, and a plan for price leaving the band.

Full-range liquidity can still be the better learning setup. It may earn less fee density, but it removes one major decision: where to place the bounds. For a first LP position, fewer moving parts can be worth more than a prettier APY.

The choice is really about maintenance. Full range asks less from the LP. Concentrated liquidity asks for range selection, monitoring, and sometimes rebalancing. That extra work is the price of the extra precision.

Traders care about concentrated liquidity because it can create deeper liquidity near the current price. More depth near the trade path can reduce slippage, which is the gap between the expected swap price and the final execution price.

Stable pairs show the idea clearly. If USDC/USDT mostly trades near one dollar, capital placed near that range can be more useful than capital spread across prices the pair may never touch.

But depth is local. A pool can look large on a dashboard and still give poor execution if active liquidity is thin near the current price. Traders need the depth where the swap actually routes, not somewhere else on the curve.

The trader experience changes by pair:

A SOL/USDC pool can have strong liquidity near the current price in the morning and thin liquidity after a sharp move. If LPs do not move or add ranges, trades can still get ugly.

Low volume can also disappoint both sides. A range can be active but quiet. In that case, traders may not see much depth improve, and LPs may not collect enough fees to justify the risk.

So concentrated liquidity can improve execution, but only where active ranges exist and trades keep happening. A dashboard with a pool name is not a guarantee of good fills. Crypto has a special talent for making a neat interface hide a messy market.

Before a large swap, check the route, expected price impact, and pool depth near the current price. If the quoted output moves hard when trade size rises, the pool is telling you the active liquidity is thinner than the headline suggests.

Liquidity providers use concentrated liquidity because it can make their capital work harder inside a chosen range. If most trading happens inside that band, the LP may earn a larger share of fees than they would with the same capital spread everywhere.

The appeal is fee density. Instead of funding prices that may never trade, the LP puts more weight near the expected market. That can be powerful on pairs with steady volume and a believable range.

This is why concentrated liquidity often appears beside yield farming incentives. A pool may pay swap fees, reward tokens, or both. Ask where the return comes from, not how large the APY tile looks.

LPs usually use concentrated liquidity for a few practical reasons:

A narrow range is a market view. It says, “I think trading will happen here.” A wider range says the LP wants more room and less babysitting. A multi-range setup says the LP is trying to shape exposure across several zones.

The return is not the APY tile by itself. Fees, rewards, price movement, gas, rebalancing, and tax records all pull on the final result. A concentrated liquidity strategy only worked if the LP is better off after those costs, not just busier.

If that market view is wrong, the position can stop earning fees while still carrying token exposure. That is why serious LPs compare the pool result against simply holding the two assets.

Concentrated liquidity risk starts with impermanent loss, but it does not end there. LPs collect fees while taking price movement risk, and a tighter range can magnify that tradeoff.

If one asset trends hard, the position can end up holding more of the weaker side of the pair. That can happen even when the LP earned fees along the way. A market rotation can push capital away from one side of a pair and leave the range stale.

The main risk checks are worth naming before any deposit:

LVR, or loss versus rebalancing, is the advanced version of the same warning. In plain English, arbitrage traders can capture value when prices move and LPs provide stale liquidity. You do not need a formula to know the takeaway: fees are not net profit until price movement and costs are counted.

Concentrated liquidity goes out of range when the market price leaves the LP’s selected band. The position stops earning new swap fees until price returns or the LP changes the range.

The token mix also shifts. If price moves up, the position may become mostly the quote asset. If price moves down, it may become mostly the base asset. That can feel like being slowly swapped into the side you did not want more of.

The LP then has three basic choices:

Each choice has a cost. None is magic, despite what a bright APY tile may imply.

Concentrated liquidity can beat holding a crypto asset, but it can also lag badly. The result depends on fees, price path, range choice, costs, and whether the LP wanted both assets in the first place.

Trending markets are the hard case. If ETH, BTC, or SOL runs strongly in one direction, an LP may end up with more of the asset that underperformed. That is the practical bagholder risk inside some LP positions.

Compare the LP result against three baselines:

Fees can offset that drag, but they are not guaranteed to do so. A good LP review compares fee income against the value of simply holding the tokens.

Concentrated liquidity appears under several protocol names. Uniswap v3 and v4 use ticks. Solana traders often see CLMM, Whirlpools, or DLMM. The words differ, but the core idea is still range-based liquidity.

A concentrated liquidity market maker, or CLMM, is an AMM that lets LPs place capital inside selected ranges. Orca Whirlpools and Raydium CLMM use that kind of language. Meteora’s DLMM uses bins, which are price buckets instead of tick boundaries.

For a user, the interface language should translate into one question: where is my capital active? If the screen says ticks, bins, ranges, or active liquidity, it is still asking the LP to decide which prices deserve capital.

The protocol wording usually translates like this:

| Protocol Word | Plain-English Meaning |

|---|---|

| Tick | A price boundary used to define a range. |

| Bin | A discrete price bucket used in a DLMM. |

| Active liquidity | Capital currently usable for swaps. |

| CLMM | A range-based concentrated liquidity AMM. |

| DLMM | A bin-based version of concentrated liquidity. |

Protocol names help you read interfaces, but they are not endorsements. The same range logic can be useful on one pair and brutal on another. A stable pool with steady volume is not the same problem as a new token with jumpy price action.

Read the pool screen before the brand story. Look for the pair, fee tier, range, active status, historical volume, and withdrawal path. If a vault manages the range for you, also check the strategy fee, permissions, manager, and contract risk.

The logo can explain where the tool lives. It cannot tell you whether the range fits the asset. That part stays with the LP.

Concentrated liquidity makes sense when the LP has a clear reason for the range and enough discipline to manage it. It fits best when the pair is liquid, the assets are understood, and trading volume is real.

Stable pairs are often easier to reason about because price usually moves inside a narrow band. Volatile pairs can still work, but they need a stronger thesis and more monitoring. That is where a conviction play needs evidence, not just “green candle, vibes confirmed.”

The range should have a reason. Maybe the pair is stable. Maybe the LP expects sideways trading. Maybe the position is a small test used to learn the interface. “The APY is high” is not a range thesis.

Good-fit conditions usually include:

Automated vaults can help with range management, but they do not remove risk. They move some work to a strategy contract or manager, then add new questions about fees, custody, permissions, and failure modes.

Position size should match the learning curve. A small LP position can teach how fees, range status, and token mix move. A large first position turns the lesson into a stress test.

Concentrated liquidity makes the most sense when the user can explain the pair, the range, the fee source, and the exit plan in plain language. If one of those pieces is missing, the setup is not ready yet.

Concentrated liquidity is the wrong tool when the user only understands the APY number. It is also a poor fit when the pair is illiquid, the token is fragile, or the position size is too large for the user’s risk budget.

The worst setup is a tiny pool, a volatile token, a tight range, and a user who cannot explain either asset. A full-port deposit into that setup is not confidence. It is one chart move away from financial slapstick.

APY-only pitches are the loudest warning. A high number can come from temporary rewards, thin trading, or a token that the LP would never want to hold. The pool can look profitable until price leaves the band or reward emissions fade.

Avoid concentrated liquidity when these signs show up:

Good concentrated-liquidity risk control should make the boring choice look acceptable. Sometimes the right move is full range, a wider band, a tiny test position, or no LP position at all.

Monitoring limits count too. If you cannot check the range, understand the token mix, or record the transactions, the strategy may be too demanding. Passive investors often need fewer moving parts, not a more exciting pool.

There is no shame in skipping a pool. The market will always offer another yield tile. Your capital does not have to audition for every one of them.

Checking a concentrated liquidity position starts before the wallet connects. The goal is to know what has to go right, what can go wrong, and what you will do when price leaves the neat rectangle on the screen.

Use a calculator as a sanity check, not a profit machine. A concentrated liquidity calculator can model ranges, fees, and price paths, but it cannot guarantee future volume or protect you from weak tokens.

Start with the pair, not the yield. If you would hate holding one side, the range is already suspect. Concentrated liquidity can quietly move the position toward the asset the market is selling.

Run through this checklist before depositing:

Then compare the plan with a simpler baseline. What happens if you just hold both assets? What happens if you use a wider range? What happens if volume drops for a week? The deposit should still make sense after those boring questions.

Then write one sentence before entering: “I exit or rebalance if…” If that sentence is impossible to finish, the position is not ready. The market will finish it for you, and it charges for editing.

The best checklist answer is not always “deposit.” Sometimes it is “watch the pool first,” “use a smaller size,” or “wait until the range thesis is clearer.”

Related terms for concentrated liquidity help separate pool mechanics from the slang and farming language around them. Use these concepts as context, not as a shopping list.

Start with the terms that change how an LP reads the position:

LP farm and PVP language can still appear around these pools. Farm talk usually points to deposits plus incentives. PVP talk usually points to harsh execution, faster traders, or stale ranges.

Farming incentives still connect to concentrated liquidity when fees and reward tokens are bundled into one return story. But incentives do not fix overconcentration, unwanted exposure, or a weak exit plan.

A badly sized LP range can turn a market view into a position the user did not mean to hold. That is the whole point of learning the mechanic before chasing the number.

Concentrated liquidity is a way for LPs to place pool capital inside a selected price range. The position earns fees only while the market price trades inside that range.

Concentrated liquidity is usually not passive income. A user still has to choose a pair, set a range, monitor fees, handle rebalancing, and compare results against simply holding the assets.

When concentrated liquidity leaves the range, the position stops earning new swap fees. The LP may wait, withdraw, or rebalance, and the position may now hold mostly one side of the pair.

Concentrated liquidity can be riskier than a full-range pool because range choice adds another way to be wrong. The risk is not only impermanent loss. It also includes costs, volume, contracts, vaults, and taxes.

Concentrated liquidity can beat holding crypto when fees outweigh price movement and costs. It can also underperform in a strong trend, especially if the LP ends up holding more of the weaker asset.

Concentrated liquidity can create tax issues because deposits, withdrawals, claims, swaps, and rebalances may all need records. Rules vary by jurisdiction, so users should track every action and use qualified tax help when needed.

Start with concentrated liquidity as a learning exercise, not a yield shortcut. Pick a liquid pair, use a small position, and watch what happens when price moves toward each side of the range.

Before connecting funds, make sure wallet setup and custody are boring in the best possible way. A range strategy is hard enough without adding a messy wallet, unclear permissions, or a recovery problem.

The first position should teach behavior, not prove bravery. A wide range can show how fees, price movement, and token mix interact without forcing constant rebalances. A tighter test can come later, after the dashboard stops looking like a magic-income screen.

Spend time in the interface before depositing. Change the range inputs. Watch how the expected token amounts shift. Compare a wide range with a tight range, then ask which one you could actually monitor.

Practical first steps should keep the damage small:

After a few days or weeks, compare the LP result with simply holding the two assets. If the position only looks good before costs, taxes, and opportunity cost, the lesson was useful.

Avoid outsourcing to a vault until you can explain the strategy yourself. A manager can reduce clicks, but it cannot make a bad pair good or a confused thesis profitable.

The first win is not maximum yield. It is recognizing when the position is in range, when fees are actually meaningful, and when the token mix is drifting away from what you wanted to own.

Once those pieces make sense, scale slowly or do nothing. Both are valid. Concentrated liquidity rewards clarity more than bravery, and DeFi already has plenty of people volunteering for the expensive lessons.