Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Internet Capital Markets (ICM) meaning, Solana context, token risks, and buyer checks.

Internet Capital Markets (ICM) are on-chain markets where assets can be issued, funded, traded, and settled through internet-native rails instead of traditional broker, bank, venture, or IPO systems.

The phrase sounds institutional, but crypto uses it in several messy ways. It can describe a market-structure idea, a Solana thesis, a launchpad-token meta, a category of ICM coins, or one specific token called Internet Capital Markets.

So the first job is simple: identify which version is in front of you before a slick chart talks you into doing portfolio gymnastics.

Internet Capital Markets (ICM) means crypto-native capital formation and trading on public networks. In the broad version, assets are issued on-chain, buyers fund or trade them directly, and settlement happens through wallets, smart contracts, pools, or order books.

That broad idea is bigger than any app or ticker. It can include startup tokens, creator coins, tokenized assets, stablecoin settlement, private-market access, DeFi launchpads, or public trading venues. The common thread is that the market forms online first, instead of passing through a bank syndicate, broker, venture allocation, or exchange listing committee.

Crypto also uses ICM as shorthand for a Solana story. In that version, Solana is pitched as the network that can host faster, cheaper, more liquid capital markets. That is a chain thesis, not a guarantee that every ICM token has substance.

The confusion starts when the same label appears on token launchpads and market trackers. Some ICM tokens are early public launches around an idea, app, creator, or brand. Some trackers group “ICM coins” as a market category. A separate token may even use the Internet Capital Markets name or ICM ticker.

That naming overlap matters. Someone learning the concept can land on a price page and assume the ticker represents the whole movement. A trader chasing a ticker can think they are buying a piece of a new financial system. Sometimes they are only buying a token with a good outfit and a short attention span.

Use the label by context:

| Meaning | What The User Should Check |

|---|---|

| Broad on-chain capital markets | What asset is being issued, traded, or settled on-chain. |

| Solana infrastructure thesis | Whether the claim is about network speed, fees, liquidity, or app design. |

| ICM launchpad tokens | What the token gives holders besides tradability. |

| Token-category tracker | Whether the page lists many ICM coins rather than defining the term. |

| Internet Capital Markets ticker | Whether the page is about one token, not the whole concept. |

That context check comes first. Before asking whether ICM is good or bad, ask which meaning is in front of you. A broad capital-market idea can be useful while a specific launchpad token is still weak, overhyped, or legally unclear.

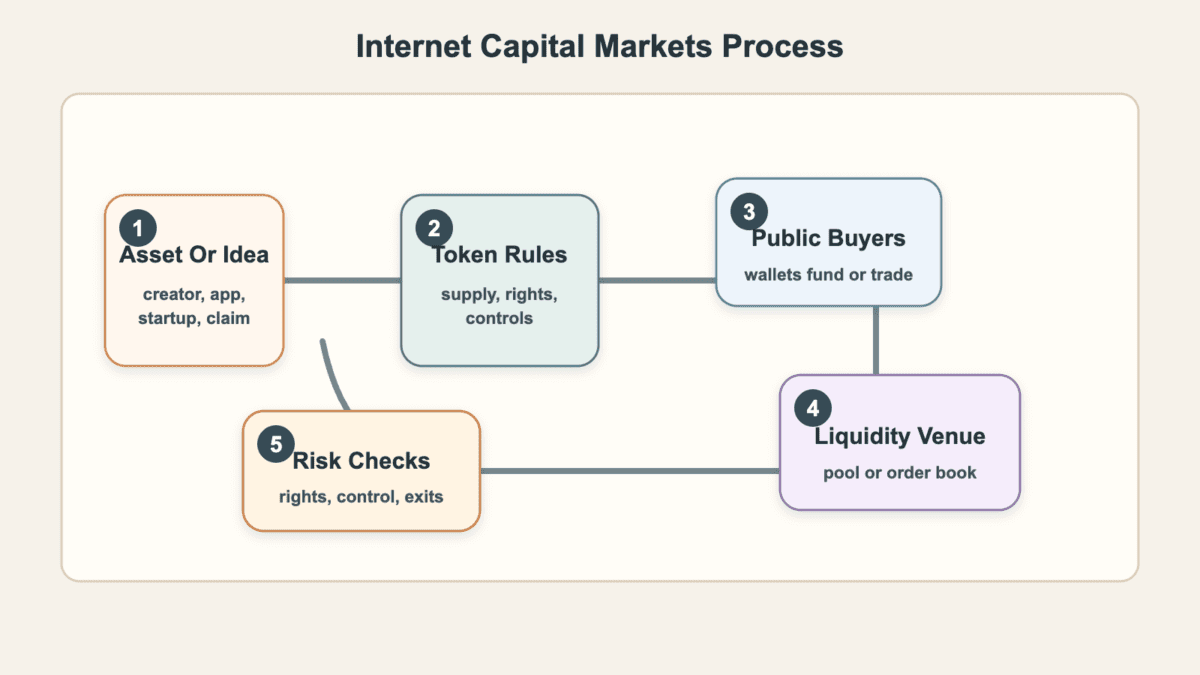

Internet Capital Markets (ICM) work by moving issuance, funding, trading, and settlement into smart contracts and public market venues. The path usually starts with an asset or claim. A token contract defines the rules, buyers interact through wallets, and liquidity forms on a pool, order book, or launchpad route.

Simple does not mean safe. A token contract can represent a clear regulated asset, a governance claim, access to an app, a points-like promise, future revenue rights, or nothing beyond a tradable asset. The market may price all of those with the same excitement for a few hours. Reality usually sends the invoice later.

An ICM-style launch often starts with an idea, app, creator, startup, or meme wrapped in a token. The issuer chooses a mint route, token standard, supply design, initial distribution, and public trading venue. Sometimes a launchpad automates much of that process.

Believe and Launchcoin are useful historical examples because they show how the phrase became tied to fast public token formation. They are examples of the launchpad meta, not a recommendation to buy any related asset.

The first real check is what the token controls. If it only trades around attention, holders may own exposure to sentiment and nothing more. If it claims governance, revenue, access, or equity-like rights, those claims need documents, contract logic, legal structure, and a route for enforcement.

Early ICM token trading can use bonding curves, pools, or other launchpad mechanics. A bonding curve changes price as buyers enter or leave. A liquidity pool lets traders swap against token and quote-asset reserves. DEX routing then finds a path through available liquidity.

This is where the crypto trenches culture appears. Traders hunt early entries, monitor deployer wallets, watch holders, and try to leave before the pool gets crowded. Some find real opportunities. Many discover that being early is not the same as being right.

Market makers and deeper pools can improve trading quality. They can reduce spreads, make exits less brutal, and help serious assets trade with less chaos. Thin pools do the opposite. A small sell can move price hard, and a crowded exit can turn a normal correction into a stampede.

An ICM token buyer may own very different things depending on the project. One token may be simple market exposure. Another may offer app access, voting, fee discounts, revenue claims, or rights tied to a regulated structure. Another may offer vibes, a ticker, and a Telegram room full of people typing faster than they think.

That range is why rights matter more than the label. A token can trade like a startup proxy without giving holders startup equity. It can be marketed like capital formation while giving buyers no claim on cash flow. It can also be a regulated tokenized asset with restrictions on who can hold it.

The cleaner the path from asset to token to liquidity, the easier it is to evaluate. The fuzzier the rights and controls, the more you are relying on market mood.

Solana is tied to Internet Capital Markets (ICM) because the current crypto usage of ICM is heavily linked to fast public token issuance and on-chain trading. For that use case, fees, speed, transaction landing, DEX liquidity, and app design are not decoration. They shape whether markets can function under pressure.

Low fees keep small trades, frequent updates, and active market making from becoming too expensive to run. Fast settlement gives traders quicker confidence that a transaction landed before the price moved. High throughput helps when crowded launches, routing, liquidations, and arbitrage all hit the chain at once.

That is the pro-Solana case in plain English: if a network can handle many low-cost transactions with enough reliability, more market activity can happen directly on-chain. Builders can create launchpads, order books, routing tools, vaults, compliance assets, and trading apps without forcing every action through slow off-chain rails.

ICM also depends on market microstructure, so the technical roadmap deserves attention. Anza’s Internet Capital Markets Roadmap says Solana’s current consensus model provides finality in 32 slots, about 12.8 seconds, while Alpenglow would target 1-2 slots, roughly 150 milliseconds. It also groups Solana work around items such as Asynchronous Program Execution, Application-Controlled Execution, and multiple concurrent leaders. For most users, the useful part is the outcome, not the acronym.

Alpenglow is about finality and confirmation speed. Faster finality can reduce the waiting period between a trade and confidence that it is settled. Asynchronous Program Execution aims to let more work happen in parallel, which can help busy apps avoid bottlenecks. Application-Controlled Execution gives apps more say over how their own transactions are ordered and handled.

Multiple concurrent leaders point to a world where the network can process more activity through more than one block producer path. In market terms, that can affect transaction landing, order fairness, spreads, and the ability of market makers to provide depth without being picked apart by latency and chaos.

Those are real infrastructure questions. They still do not make every Solana ICM token safe. A faster road helps serious traffic and reckless driving alike. The chain can improve settlement while a token still has fake links, thin pools, hidden holders, or no rights beyond a chart.

So read Solana ICM claims in two layers. First, infrastructure: can the network support better capital markets? Then, asset quality: does this specific token deserve the market it is getting? That second question is where many wallets get hurt.

Internet Capital Markets (ICM) sit between old fundraising routes and crypto-native trading routes. That is why comparisons get messy. ICM can look like an ICO when a token launches early. It can look like a meme coin when attention drives price. It can sound like an IPO when people talk about public capital formation. It can overlap with tokenized stocks when real-world assets move on-chain.

The useful comparison is what buyers get, how liquidity forms, what disclosures exist, and what recourse remains if the promise breaks. Slogans about old finance versus crypto do not answer any of that.

Here is the cleaner split:

| Route | What Changes For The Buyer |

|---|---|

| ICO | Buyers may get early token exposure, often with limited disclosure and high execution risk. |

| IEO | An exchange adds venue screening, but buyers still depend on token rights and listing quality. |

| DeFi launchpad | Public access can be fast, while liquidity and contract risk stay close to the surface. |

| Meme coin | Attention may be the product, so exits depend on crowd behavior more than cash flow. |

| Tokenized stock | The token should map to a legal asset claim, eligibility rules, custody, and disclosures. |

| VC round | Access is limited, disclosure may be private, and liquidity usually arrives much later. |

| IPO | Public shares come with formal disclosure, regulation, broker access, and legal shareholder rights. |

| ICM token | The buyer must verify rights, liquidity, controls, and whether the token is more than market exposure. |

ICM can improve access. It can let more people see and trade assets earlier. It can also compress the time between an idea and a liquid market until diligence barely has time to put on shoes.

That speed is both the blessing and the trap. Traditional routes are slow, gated, expensive, and full of insiders. Crypto routes can be open, global, and liquid from day one. But openness does not create disclosure by itself. Liquidity does not create legal rights. A ticker does not create a business model.

Tokenized stocks are a different branch. If a token truly represents a stock, fund, bond, private-market claim, or real-world asset, the hard questions become custody, eligibility, issuer status, transfer restrictions, and legal enforceability. That looks less like a meme launch and more like financial plumbing.

ICM launchpad tokens usually live closer to the speculative end. Some may become useful apps or communities. Others may just be attention markets. The difference rarely appears in the ticker. It appears in documents, contracts, liquidity, team behavior, and whether real users show up after the chart cools down.

Internet Capital Markets (ICM) risks start with speed. If a token can be created, promoted, bought, and dumped quickly, the market can punish anyone who confuses access with quality. Faster capital formation also creates faster mistakes.

The main loss scenarios are familiar, but ICM makes them feel more polished. Thin liquidity can turn a modest sell into a steep price drop. Snipers and bots can enter before normal users. Creator wallets can sell into excitement. Holder concentration can put control in a few hands. Fake links and copycat contracts can drain wallets before the real trade even begins.

> Warning: an ICM label does not verify the token, the issuer, the rights, the contract, or the exit route.

Liquidity is usually the first place to look. If a pool is shallow, late buyers become exit liquidity for earlier wallets. That does not require a dramatic scam. It can happen when the first wave simply sells into a market that cannot absorb the size.

Contract and liquidity control come next. A hard rug is the ugly version: liquidity can be pulled, selling can be blocked, minting can be abused, or contract permissions can be used against holders. That is why mint authority, freeze authority, upgrade authority, liquidity locks, and contract verification matter.

Some failures are slower. A soft rug can look like fading communication, missed promises, abandoned development, quiet wallet selling, or a creator who keeps the token alive just enough to drain belief. No single candle tells the whole story, but the pattern gets expensive.

Creator selling also needs nuance. Not every sell is a rug. Teams need funding, early holders take profit, and markets correct. The problem is hidden supply, unclear allocations, poor disclosure, and selling into a thin pool while public messaging stays bullish. That is where “normal market behavior” becomes a trust problem.

Wallet safety sits beside market risk. Launchpad links spread fast, and fake contracts can look convincing. DMs, support accounts, copied websites, and transaction prompts can all target users who are moving quickly. The faster the market, the more valuable a calm second check becomes.

Regulatory and tax risk also belong in the stack. If a token claims revenue, equity, or financial rights, legal status matters. If it trades only as a token, taxes can still apply when you swap, sell, bridge, or claim. ICM can feel like a new market category, but your local rules may see a taxable trade, a security, or an unregistered offering question.

The practical takeaway is blunt: inspect the exit before admiring the entry. If you cannot explain who can sell, where liquidity sits, what permissions remain, and what holders own, the ICM label has not done enough work.

Researching an ICM token before buying means checking the asset, contract, people, liquidity, rights, and wallet path before you trade. You are not trying to predict the future. You are trying to avoid obvious traps before they become expensive lessons with screenshots.

Start with the official source, then verify it outside the marketing loop. Get the contract address from the project’s primary channel and compare it with a block explorer, DEX listing, and credible market page. Do not trust ticker names, chart screenshots, forwarded links, or replies from people cosplaying as customer support.

Work through the checks in this order:

Wallet setup deserves its own pause. Risky launches are easier to manage with a dedicated trading wallet, limited balances, and careful approval hygiene. If you need a broader custody refresher, CryptoProcent’s crypto wallets section is a better next stop than signing a mystery transaction from a promoted link.

Creator identity is another signal, not a verdict. An anon dev can ship real work, and a doxxed founder can still disappoint holders. The difference is accountability. Check whether the creator has a history, a public code trail, prior launches, clear communication, and wallets that match the story.

Then look at liquidity like a seller, not a buyer. A chart can rise on small buys if the pool is thin. Ask what happens when several wallets sell at once. Check depth around your intended exit, not just headline volume. Watch for wash-like churn, sudden holder clusters, and routes that look fine for small trades but break for real size.

Rights are the final gate. If the token claims access, governance, revenue, yield, equity, or a share in a future asset, find the exact mechanism. If the answer is a vague promise, assume you own market exposure until proven otherwise. That is not cynicism. It is reading the receipt before the kitchen closes.

Internet Capital Markets (ICM) could split into two very different paths. One path is retail launchpad culture, where creators and apps issue tokens quickly and markets decide in public. The other path is institutional tokenization, where stocks, funds, credit, stablecoins, private assets, and settlement workflows move on-chain with legal wrappers.

Both paths use internet-native rails, but they do not require the same trust model. A creator token may need attention, liquidity, and a working product. A tokenized stock needs custody, disclosures, transfer rules, eligible holders, reporting, and legal rights. Same chain. Very different burden.

The future paths look like this:

| Future Path | What Would Make It Real |

|---|---|

| Retail launchpads | Useful products, clear token rights, safer launches, and deeper liquidity. |

| Tokenized stocks | Regulated issuers, custody, disclosures, transfer controls, and real legal claims. |

| Stablecoin settlement | Reliable liquidity, compliance routes, fast settlement, and broad merchant or market use. |

| Private-market assets | Verified issuers, eligibility rules, valuation discipline, and enforceable ownership. |

| On-chain order books | Market-maker depth, fair ordering, low latency, and strong risk controls. |

| Creator markets | Real audience demand, transparent economics, and less dependence on pure hype. |

Retail ICM will likely stay noisy. Fast launches attract builders, traders, bots, promoters, and copycats. That does not make the category fake. It means the signal has to survive a market full of people trying to sell it back to you.

Institutional ICM will move slower because regulated assets need more than a token contract. They need issuers, custody, audits, compliance, eligibility checks, and rights that survive outside the wallet. That may sound boring, but boring is often what makes serious capital comfortable.

The signals worth watching are practical. Look for assets that settle real activity, issuers that disclose rights clearly, contracts that have been reviewed, liquidity that holds under stress, and user demand that continues after launch week. If the only evidence is a chart and a slogan, the market may still trade it. Just do not confuse that with capital-market progress.

Start with Internet Capital Markets (ICM) by naming the version in front of you. Are you reading about the broad on-chain market idea, the Solana infrastructure thesis, a launchpad token, a category tracker, or one ICM ticker? That one question removes a lot of bad assumptions.

Then slow the trade down. ICM is attractive because it promises faster access, public liquidity, and fewer old-market gates. Those features are useful only if the token has clear rights, clean contracts, real liquidity, and a safe wallet path.

If you are studying the infrastructure side, focus on transaction landing, settlement quality, liquidity depth, and whether serious apps can run without constant congestion. If you are studying a token, focus on rights, controls, holders, and exits. The same phrase can point to both, but the checks are different.

For a new ICM token, a small observation period can teach more than a rushed entry. Watch how liquidity reacts after the first wave, whether creator wallets move, whether volume survives outside launch hype, and whether the project keeps shipping once attention leaves. A market that needs constant noise to stay alive is already telling you something.

Use this short sequence before acting:

The best version of ICM makes markets more open and settlement more direct. The worst version gives a flimsy token an institutional-sounding label. Your job is to tell those apart before the market does it for you.

Internet Capital Markets (ICM) means on-chain systems for issuing, funding, trading, and settling assets through crypto rails. The phrase can also refer to the Solana ICM narrative, ICM launchpad tokens, token-category trackers, or one token using the ICM name.

Internet Capital Markets is not automatically the same as an ICM token. The broader term describes an on-chain capital-market model, while an ICM token may be one launchpad asset, one category listing, or one ticker with its own separate risk.

Internet Capital Markets are not just ICOs, but some ICM token launches can resemble ICO-style public fundraising. The key differences are venue, liquidity, contract design, disclosure, legal rights, and whether the token represents anything beyond tradable attention.

Solana is connected to Internet Capital Markets because current ICM usage often centers on fast, low-cost on-chain issuance and trading. Solana’s speed, fees, DEX activity, and market-structure roadmap make it a common network for that narrative, though that does not make every Solana ICM token safe.

Internet Capital Markets tokens can represent real equity only when the token is built inside a legal structure that gives holders enforceable rights. Many ICM tokens do not grant equity, revenue, or ownership, so buyers should verify the documents and contract mechanics before assuming anything.

The biggest ICM risks for traders are thin liquidity, unclear token rights, creator selling, holder concentration, fake contracts, unsafe wallet approvals, and regulatory uncertainty. The fastest way to reduce risk is to verify the contract, rights, liquidity, holders, and exit route before buying.