Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Learn what proof of reserves proves, what it misses, and how to read a crypto reserve report.

Proof of reserves is a way for a crypto custodian to show it holds assets that are meant to back customer balances.

A good reserve report can reduce uncertainty before you keep coins with an exchange, lender, stablecoin issuer, or another custodian. But it only answers part of the trust question. You still need to know which liabilities are included, when the snapshot happened, and what sits outside the report.

Proof of reserves means a crypto custodian shows evidence that it holds assets backing user balances. The custodian might be an exchange, lending platform, stablecoin issuer, broker, or any service that holds customer funds instead of letting users control their own keys.

The word “reserves” is the key. It does not just mean a wallet has coins in it. It means those assets are supposed to stand behind customer claims, such as BTC, ETH, stablecoins, or other balances shown inside accounts.

In crypto, a proof of reserves report usually has two sides. One side shows assets the custodian controls, often through public wallet addresses or signed wallet messages. The other side shows a snapshot of what users are owed.

That snapshot is normally tied to one moment in time. If your account balance was 1 ETH then, the report should include a privacy-preserving way to show that your 1 ETH was counted in the customer-balance total.

The result is not magic accounting dust. It is a transparency method. It lets users check whether reported assets line up with reported obligations. It also shows where the platform still asks for trust.

So the proof of reserves meaning is simple: show the coins, show the customer claims, and explain the gap between those two numbers clearly enough that users can inspect it.

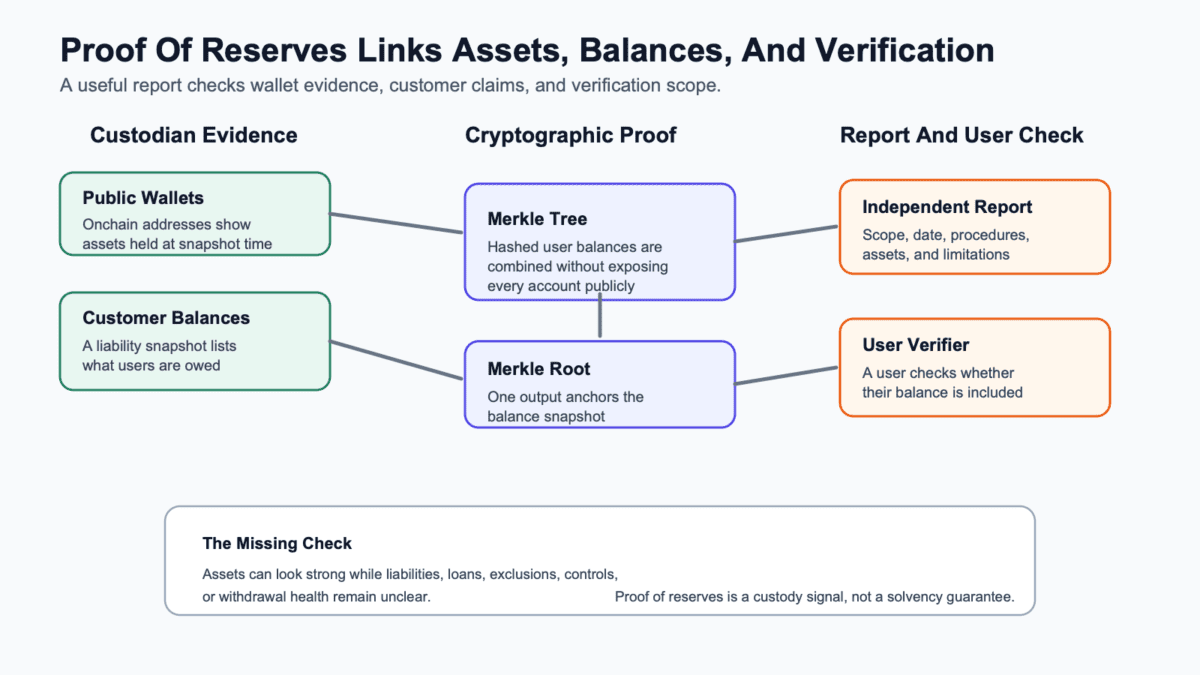

Proof of reserves works by combining asset evidence, customer-balance data, cryptographic hashing, and an independent review process. The goal is to prove inclusion and backing without publishing every user’s private account balance.

The asset side usually starts onchain. A custodian lists wallet addresses or signs messages from wallets to show control over specific reserves. For BTC, ETH, and many tokens, anyone can inspect those addresses on a block explorer.

The liability side is more sensitive. A platform cannot publish a full list of names and balances without creating a privacy disaster. So it often hashes user balances into a Merkle tree, which compresses many entries into one Merkle root.

Here is the plain workflow:

| Step | What The User Learns |

|---|---|

| Wallet Evidence | The custodian appears to control certain onchain assets at snapshot time. |

| Balance Snapshot | Customer claims are counted for the report’s chosen date and scope. |

| Merkle Tree | Individual balances are hashed into a privacy-preserving structure. |

| Merkle Root | One output represents the whole included balance set. |

| Independent Report | A third party checks procedures, scope, and reported results. |

| User Verifier | A user can test whether their balance was included. |

_Proof of reserves is strongest when the asset evidence and liability snapshot are both clear._

A Merkle proof lets one user check their own inclusion path. It should show that their hashed balance connects to the published Merkle root. That helps detect omitted accounts, at least when enough users actually verify.

The independent role varies. Some reports use accountants, some use security firms, and some use internal dashboards. The label matters less than the scope. A narrow check can still produce a neat PDF with a weak answer.

Proof of reserves can show whether an exchange or custodian controls assets that match the report’s stated scope. That is the useful part, and it should not be dismissed just because the method has limits.

For users, the first value is visibility. A report can point to public wallet addresses, reserve ratios by asset, a snapshot date, and a user-verification tool. That gives you more to inspect than a brand promise and a polished dashboard.

Useful signals include:

The best reports separate assets by coin. If BTC reserves look fully backed but a smaller token is excluded, that should be visible. Aggregated totals can hide weak coverage because one overfunded asset may make another gap look smaller.

Timing also changes the signal. A report from last week is more useful than one from last year. A dashboard that updates often is better than a stale snapshot, but frequency only helps when the scope is still strong.

Public exchange transparency dashboards can also give a useful scale check across major custodians. Still, a large wallet balance does not answer the liability question unless the report also shows what users are owed.

Use proof of reserves as a custody transparency layer. It can show that assets existed and were controlled at a specific time. It cannot, by itself, show every claim against those assets.

Proof of reserves misses the hardest part of custody risk when it fails to cover liabilities, debts, asset quality, operational controls, and withdrawal health. A pile of coins means less when other claims quietly rank ahead of users.

Liabilities are the missing half. If an exchange shows $1 billion in assets but owes users, lenders, counterparties, and affiliates more than that, the reserve number can still look comforting while the business is fragile.

The PCAOB warned that proof-of-reserve reports are limited and should not be relied on like full financial statement audits. That warning fits the everyday user problem: a narrow report can sound official while leaving out key solvency questions.

Use this split when reading any report:

| What PoR Can Show | What It Cannot Prove |

|---|---|

| Assets controlled at a snapshot time | All liabilities and off-balance-sheet obligations |

| Wallet ownership or signed control | Whether assets were borrowed before the snapshot |

| Included customer balances | Whether excluded accounts change the result |

| Reserve ratios by listed asset | Asset quality, liens, loans, or legal claims |

| User balance inclusion | Ongoing withdrawal health after the report |

| Report scope and procedures | Full business solvency or management honesty |

The snapshot problem is especially sharp. A platform could borrow assets before a report, move funds after it, or exclude parts of the business from scope. Proof of reserves gets weaker when those boundaries are vague.

Operational risk sits outside the Merkle tree too. A custodian can have assets and still freeze withdrawals, mishandle keys, face legal restrictions, or lose access during an incident. Users feel all of those failures the same way: they cannot get their funds out.

That is why proof of reserves cannot prevent every hard rug style failure. It may create warning signs sooner, but it does not stop a platform from failing after the snapshot.

Read a proof of reserves report by checking date, scope, liabilities, independent review, user verification, and withdrawal behavior in that order. A slick page helps only when the underlying scope is clear.

Start with the date. If the report is old, the strongest number on the page may describe a world that no longer exists. Crypto balances move fast. Platform stress can move faster.

Then check the asset scope. Does the report cover BTC only, major assets only, all customer assets, fiat balances, wrapped tokens, staked assets, and pending withdrawals? Exclusions are not always bad. Hidden exclusions are the problem.

Use this sequence before trusting the headline ratio:

Liability coverage deserves extra attention. A proof of reserves audit label can sound broad, but the work may be an agreed-upon procedure, a dashboard check, or a narrow attestation. If the report only shows wallets, you still do not know the full claims stack.

A stale or selective report can also become a soft rug signal. Not every stale report means fraud, but slow transparency decay often shows up before everyone agrees the warning was obvious.

The user verifier is helpful, but it has limits. It can show your balance was included in the reported tree. It usually cannot prove every other customer was included, that all liabilities were counted, or that the custodian stayed healthy after the snapshot.

Proof of reserves examples differ by business model. Exchanges, lenders, stablecoin issuers, public companies, and real-world-asset issuers can all publish reserve information. The reports may look similar, but they are not proving the same thing.

Exchange proof of reserves often focuses on customer crypto balances and onchain wallets. Users often check names such as Binance, Kraken, OKX, Bybit, Crypto.com, and similar custodial platforms. Availability changes, so a permanent proof of reserves list can go stale quickly.

These example types are more useful than a frozen ranking:

| Example Type | What To Check |

|---|---|

| Merkle-Tree Exchange PoR | Can users verify their balance and inspect the asset scope? |

| Public-Company Reporting | Are audited financial statements separate from any reserve page? |

| Stablecoin Reserve Attestation | Which assets back the tokens, and how often is the report updated? |

| Oracle-Fed Reserve Feed | Does the feed update often, and who supplies the data? |

| Platform With No Current PoR | Is there another credible disclosure path, or only marketing language? |

| Stale PoR Page | Does the platform explain why reporting stopped or changed? |

The same brand can also publish more than one transparency artifact. A reserve page, audited financial statement, monthly attestation, wallet dashboard, and status page all answer different questions.

For a normal user, the useful habit is to compare the report type with the custody promise. If a platform asks you to leave assets there, its transparency should explain assets, liabilities, limits, and the exit path in plain language.

Proof of reserves differs from audits, attestations, and proof of solvency because each label covers a different question. The labels sound official, but the answer for users can be very different.

A financial statement audit reviews a company’s financial statements under formal standards. A proof of reserves report may instead review specific procedures, such as checking wallet balances and customer snapshots at one time.

This table separates the labels:

| Term | What It Means For A User |

|---|---|

| Proof Of Reserves | Evidence that assets back included customer balances at a stated time. |

| Proof Of Liabilities | Evidence about what the custodian owes to customers and others. |

| Proof Of Solvency | A broader claim that assets exceed liabilities after scope and quality checks. |

| Attestation | A third-party assurance report tied to a defined subject and standard. |

| Agreed-Upon Procedures | Work where management defines procedures and the report lists findings. |

| Financial Statement Audit | A broader audit of financial statements, controls, and disclosures. |

“Audited PoR” is the phrase to slow down on. It may mean an accountant checked a narrow reserve procedure. It may not mean the whole business was audited, every liability was checked, or the platform was solvent.

Proof of solvency is the stronger idea users usually want. It needs assets, liabilities, asset quality, timing, and exclusions. Some designs combine Merkle-tree liabilities with reserve proof, but implementation details decide whether the result is strong.

The clean reading is simple. Proof of reserves can support a solvency claim, but it is not the same claim. If a platform blurs those terms, read the limitations before the headline percentage.

Proof of reserves is moving toward more frequent reporting, better liability proofs, privacy-preserving verification, and clearer custody disclosures. The direction is useful. The details still decide the strength.

More frequent reporting is the obvious path. A monthly or live-style feed can reduce stale-snapshot risk, especially for assets that are easy to verify onchain. But frequent asset updates still need liability coverage.

The next improvements usually fall into a few buckets:

Zero-knowledge proofs are especially interesting because they can prove something about a dataset without exposing the whole dataset. For proof of reserves, that could mean better ways to prove customer-balance totals while protecting account privacy.

For users, the useful upgrade is auditability without turning every account into public baggage. A better system should let more people verify inclusion, let outside reviewers recompute totals, and make missing liabilities harder to hide.

The risk is buzzword drift. A platform can say “real-time,” “oracle,” or “zero knowledge” while still giving users a narrow answer. New methods should make reports easier to verify, not harder to question.

Expect proof of reserves to become more normal for custodians. Also expect users to ask sharper questions. That second part is the real upgrade.

Proof of reserves becomes easier once you separate custody, liquidity, and trust signals. The report answers one custody question. Related concepts explain what can still go wrong around it.

Start with wallets if you want the self-custody alternative. A wallet does not make crypto risk disappear. It changes who controls the keys and who must prove reserves.

Then look at exit liquidity when a platform or product depends on later users, thin liquidity, or confidence that can vanish under pressure. Reserve transparency helps, but liquidity stress can still punish users who leave too late.

Merkle trees explain the inclusion proof. Zero-knowledge proofs explain where private verification may improve. Rugs explain why transparency must arrive before trust collapses, not after everyone is already refreshing a withdrawal page with cold coffee and a worse mood.

Use related concepts to sharpen the question, not to create a link pile. The core question stays the same: can the custodian show assets, include liabilities, and let users verify enough to make a better custody choice?

Proof of reserves in crypto is evidence that a custodian holds assets intended to back customer balances. It usually combines onchain wallet proof, a customer-balance snapshot, and a report explaining scope and limitations.

The strongest version also includes liabilities. Without liabilities, the report may show assets without showing the full claims against those assets.

Proof of reserves does not prove an exchange is solvent by itself. Solvency depends on assets, liabilities, asset quality, debts, legal claims, withdrawal access, and business controls.

A strong proof of reserves report can support a solvency claim when liabilities are included. A weak one only shows part of the asset side.

Proof of reserves is not the same as a financial statement audit. A PoR report may test specific wallet balances, snapshots, or procedures, while an audit has a broader accounting scope.

The wording around “audit” is where users often overtrust the report. Always read what was checked, who checked it, and what was excluded.

Merkle trees help proof of reserves by letting a platform include many user balances in one cryptographic structure. Each user can check whether their balance connects to the published Merkle root.

That protects privacy better than publishing every account balance. It still depends on the snapshot being complete and honestly prepared.

Proof of reserves can reduce blind trust, but it cannot prevent every exchange failure. It may expose missing assets sooner when reports are strong and users actually verify them.

It cannot stop hidden liabilities, bad controls, fraud after the snapshot, legal restrictions, or withdrawal freezes by itself.

Some platforms do not publish proof of reserves because their systems, legal structure, asset mix, or reporting process may not support a clean public proof. Others simply choose less transparency.

That absence is not automatic proof of insolvency. But it should push users to look for other disclosures, withdrawal reliability, financial reporting, and custody details before leaving funds there.

Start with proof of reserves as one custody check, then compare it with the platform’s wider risk signals. A report can help you decide where to keep funds, but it should not be the only evidence you use.

Set a personal threshold before stress arrives. A small trading balance, a payroll-sized stablecoin balance, and long-term savings should not depend on the same level of trust. The larger the balance, the stronger the reporting and withdrawal evidence you should require.

Use a short routine before depositing or leaving serious balances on a custodian:

If the platform fails two or more checks, lower your exposure before you need a heroic exit. Keep trading balances separate from long-term holdings. Do not use a reserve report as permission to ignore basic withdrawal hygiene.

Then compare the report with behavior. Are withdrawals normal? Are support queues exploding? Did the platform stop updating a once-prominent reserve page? Did exclusions grow without a plain explanation?

Proof of reserves is best used early. It gives you a reason to ask better questions before stress arrives. Once withdrawals are paused, even the cleanest old snapshot becomes yesterday’s weather report: interesting, but not enough to get your funds out.