Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Understand recursive leverage before copying a DeFi loop.

Recursive leverage is a DeFi borrowing pattern where users redeposit borrowed assets to increase crypto exposure or yield.

It can look fully collateralized on a dashboard, which is the trap. Every loop adds debt, tightens the liquidation buffer, and makes the exit more complicated than the entry screen suggests.

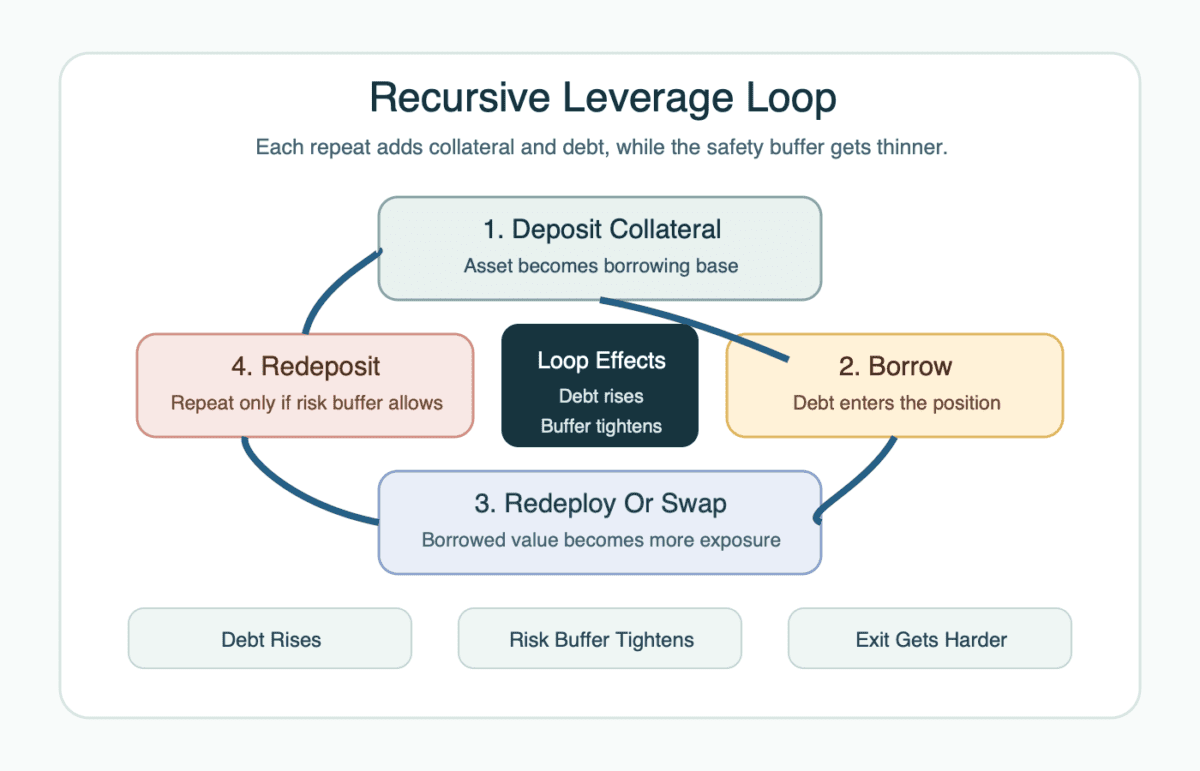

Recursive leverage in crypto is a repeated DeFi borrowing cycle. A user deposits collateral, borrows against it, redeploys the borrowed asset, and deposits again to increase exposure or yield.

The position may still be overcollateralized after each round. But overcollateralized does not mean low risk. It means the protocol has collateral it can liquidate if the account crosses the danger line.

Recursive leverage turns one borrowing action into the input for the next one. One deposit supports one loan. That loan becomes more collateral or exposure, and that new collateral supports another loan.

The pattern often starts with a simple idea:

That cycle is why the position can grow without adding fresh capital. It is also why the debt grows. The account is not magically earning more from the same risk. It is carrying more risk inside a larger loop.

Crypto users often call recursive leverage a loop. Research notes and protocol-risk discussions may call it recursive lending or recursive borrowing. That wording shows up around Aave, Morpho, stablecoin loops, liquid staking tokens, Pendle PTs, and one-click DeFi tools.

Those names point to the same core mechanic. “Looping” is the wallet-user phrase. “Recursive leverage” is the cleaner risk term because it names the debt hidden inside the repeated borrow-and-redeposit pattern.

The wording matters when someone frames the trade as passive income. A stablecoin loop, Aave looping setup, or liquid-staking loop may have a yield goal, but the engine is still debt. The loop is not free yield wearing a nicer jacket.

Recursive leverage works by recycling borrowed value back into a lending market. Each repeat increases supplied collateral and borrowed debt, while the account’s health factor, LTV, or risk score leaves less room for mistakes.

Protocols do not all calculate risk in the same way. Some show a health factor. Others show loan-to-value, collateral factor, liquidation threshold, or a similar risk metric. The names vary, but the pressure is the same: more debt leaves less room for price, rate, and liquidity shocks.

The sequence is plain:

| Loop Step | What Changes |

|---|---|

| Deposit collateral | The protocol recognizes an asset that can back borrowing. |

| Borrow against it | Debt appears, and the account now has a liquidation line. |

| Redeploy or swap | Borrowed value becomes more exposure, yield collateral, or another position leg. |

| Redeposit and repeat | Collateral and debt both grow while the safety margin shrinks. |

Common versions use the same loop with different weak points:

Any edge can vanish. Borrow APR can rise, supply APY can fall, rewards can end, and swap costs can eat the margin. Gas and slippage also compound through the loop. A clean dashboard can hide a messy unwind.

The deeper issue is exit complexity. Opening several loops may feel like one action, especially through an automation tool. Closing them can require repaying debt, withdrawing collateral, swapping assets, and repeating the process while markets move.

DeFi users use recursive leverage to turn one asset base into a larger position, a higher-yield setup, or a reward-farming trade. Those motives are not identical, and mixing them is where trouble starts.

The main motives usually look like this:

Each motive fails in a different way:

Conviction may explain why someone wants more exposure. It does not remove the liquidation path.

So the first check is motive, not loop count. If the goal is long exposure, define the loss boundary. If the goal is yield, calculate net return after borrow APR, fees, slippage, gas, and reward timing. If the goal is points, admit that points are promises until they become liquid value.

The dangerous version starts with an APY screenshot and works backward. That is how a trade becomes a debt machine with a marketing department.

Recursive leverage shows up wherever users can borrow against collateral, redeploy value, and borrow again. The pattern is not tied to one chain, protocol, or token type.

The venue changes the weak point. Aave and Morpho loops often depend on lending-market parameters. ETH and LST loops depend on collateral relationships. Stablecoin and PT loops may look calmer, but they move risk into rates, redemption, maturity, and liquidity.

Aave looping is the most familiar example for many users. A user supplies collateral, borrows within the allowed range, redeploys the borrowed asset, and keeps watching health factor.

Morpho and similar lending venues can support the same pattern. The details differ by market, collateral type, oracle, liquidation threshold, and available liquidity. A loop that looks safe in one market may be reckless in another.

ETH-correlated loops often use assets such as wstETH, weETH, rsETH, or WETH. The appeal is clear. If the assets usually move together, the loop may look less volatile than borrowing stablecoins against ETH.

“Usually” is doing a lot of work there. LST and restaking loops can still face depeg risk, liquidity stress, oracle moves, staking-yield changes, and borrow-rate spikes. A close relationship between assets can narrow price risk, but it can also encourage users to run thinner buffers.

Stablecoin looping may feel safer because both sides often aim for dollar value. But the risk moves to borrow APR, peg quality, issuer confidence, redemption paths, and whether incentives stay large enough.

Pendle PT loops, ERC-4626 vault tokens, RWA tokens, and other yield-token loops add another layer. Maturity dates, exchange-rate accounting, redemption windows, and thin markets can all decide whether the loop reaches its expected endpoint.

Use this map to compare the weak point:

| Loop Type | Main Risk To Check |

|---|---|

| Aave or Morpho lending loop | Health factor, oracle pricing, and liquidation threshold. |

| ETH or LST loop | Peg, liquidity, borrow APR, and collateral correlation. |

| Stablecoin loop | Borrow cost, peg quality, issuer risk, and reward durability. |

| PT or yield-token loop | Maturity, pricing, exit depth, and debt timing. |

| Automated loop | Hidden leverage, assumptions, and unwind path. |

The examples are not recommendations. They help with pattern recognition. If a setup cannot explain what backs the debt, what the debt is, and how the position closes under stress, it is not ready for size.

Recursive leverage can fail through liquidation, negative carry, depegs, oracle stress, thin liquidity, or a crowded unwind. Liquidation is the loud failure. The quieter ones can hurt first.

A 2026 Bank of Canada staff paper on Aave V3 studied borrower behavior, liquidation dynamics, and recursive leverage despite overcollateralization. It also estimated that realized losses, including liquidation penalties and missed price recoveries, can amount to 10-30% of liquidated value. The beginner lesson is simple: collateral requirements do not erase leverage risk.

> A recursive leverage loop can fail while the original thesis still sounds reasonable. The protocol responds to collateral, debt, prices, and rules, not vibes.

Liquidation happens when the account no longer has enough collateral buffer for its debt. A liquidator can repay part of the debt and receive collateral, often with a penalty built into the protocol rules.

Recursive leverage makes this sharper because each loop adds debt. A small collateral move can affect a larger position than the user first deposited. If the collateral asset falls or the debt asset rises, the health factor can drop faster than expected.

Borrow rates can change after the loop opens. If utilization rises, the borrow APR may jump. If rewards fall, a once-positive yield spread can turn into negative carry.

This is common in stablecoin loops. The chart may look calm because the assets remain close to a dollar. The account still bleeds if the borrow cost outruns the supply yield and incentives.

Correlated assets can stop acting correlated. Stablecoins can depeg, LSTs can trade at discounts, and yield tokens can lose depth before maturity.

Oracles add another risk layer. If the protocol price diverges from executable market prices, the dashboard may not match the exit a user can actually get. Thin liquidity can make the situation worse during stress.

Unwind risk is the risk that closing the loop makes losses worse. Closing a loop may require several repayments, withdrawals, swaps, and redeposits in reverse.

When many users exit similar positions at once, the trade can push into weak liquidity. That is where loop users can become someone else’s exit liquidity before they finish closing.

Plan the exit before opening the loop. Waiting until the health factor is blinking is like learning the fire exits after smelling smoke.

Recursive leverage differs from margin trading, yield farming, and plain borrowing because the leverage comes from repeated lending-market actions. It may resemble those strategies on the surface, but the failure points differ.

Margin trading usually gives a trader a direct leverage setting on an exchange or derivatives venue. A DeFi recursive loop uses collateral deposits, loans, oracle prices, liquidation thresholds, and borrow-rate markets.

That changes the job of monitoring. A margin trader may watch entry price, liquidation price, and funding. A recursive leverage user also has to watch collateral quality, borrow utilization, protocol parameters, swap depth, and the path back out.

Here is the plain comparison:

| Concept | What Changes |

|---|---|

| Margin trading | Leverage is set directly through a trading venue or derivatives product. |

| Yield farming | Farming may earn rewards without adding borrow debt. |

| Collateralized borrowing | A single loan stops before the repeat borrowing cycle. |

| Leverage loop | Usually the user-facing name for recursive leverage. |

| Recursive lending | Often the lending-market synonym for the same loop. |

The terms separate cleanly when you track the debt:

Yield farming is often misread here. Farming can involve deposits, incentives, and changing APYs without adding borrow debt. Recursive leverage adds the borrowing leg, so the reward screen is only half the position.

“Recursive leverage” is more common when the focus is protocol risk, research, and how debt stacks inside a lending market. A leverage loop is the user-facing phrase. Recursive leverage is the risk-aware name for the same machine.

Evaluate recursive leverage by checking the debt path before the yield path. If you cannot explain how the loop fails, the position is too large or too complex.

Start with the boring dashboard terms. Find the collateral asset, debt asset, LTV, liquidation threshold, liquidation penalty, borrow APR, supply APY, reward source, oracle, and available liquidity.

Debt and collateral checks show what the position actually depends on. Do not stop at the headline APY or the number of loops.

Ask these before entering:

A low starting LTV can be useful, but it is not a guarantee. Protocol parameters can change, collateral can gap down, and correlated assets can widen when everyone needs the same exit.

Rate checks decide whether the yield story survives normal market changes. Supply APY, borrow APR, rewards, points, fees, slippage, and gas all belong in the same calculation.

The key questions are short:

Adding collateral to defend a failing loop can also make the position worse. That is how a user becomes a bagholder with a debt tab, not a smarter risk manager.

Exit checks show whether the position can close under pressure. Automation can help with transactions and alerts, but it cannot make liquidity appear.

Before copying a recursive leverage setup, identify:

The final test is simple. If the loop only looks good under one friendly rate snapshot, it is not a strategy. It is a screenshot with debt attached.

Recursive leverage is a poor fit for users who cannot monitor positions, explain liquidation, or handle a forced unwind. It is also a poor fit for anyone attracted mainly by headline APY.

Beginners should avoid it until borrowing dashboards feel boring. That means understanding collateral factors, debt assets, liquidation thresholds, borrow rates, repayment, and what a liquidator can do.

The same warning applies to users who cannot react quickly. A loop can look fine on Sunday and turn ugly after a peg move, rate spike, oracle change, or liquidity crunch. If the owner cannot repay, add collateral, or unwind manually, the protocol will not wait for a calmer schedule.

Some users should stay out entirely:

That last point deserves its own warning. Going full port into recursive leverage can hit the same user three ways: collateral falls, debt stays real, and emotions push bad decisions.

There is also a records problem. Recursive leverage can create multiple borrows, swaps, deposits, withdrawals, rewards, and liquidations. Users who cannot track those movements should solve recordkeeping before adding a loop.

Smaller size does not make a bad setup good. It makes mistakes survivable. Recursive leverage is not evil, just unforgiving. If the loop needs perfect rates, perfect peg behavior, and a calm exit to work, keep the wallet away from the shiny loop button.

Recursive leverage in crypto is a DeFi loop where users deposit collateral, borrow against it, redeploy the borrowed asset, and repeat. The goal is usually more exposure, more yield, or both.

Yes, recursive leverage is usually the same core idea as looping, recursive lending, or recursive borrowing. “Looping” is the casual user term, while recursive leverage is more common in protocol-risk and research contexts.

Yes, recursive leverage can get liquidated if collateral no longer covers the debt with enough buffer. The risk can rise quickly because every loop adds more debt to the account.

Recursive leverage can create yield, but it is not truly passive income. Borrow costs, reward changes, fees, slippage, liquidation risk, and monitoring all sit inside the trade.

Stablecoin recursive leverage may reduce price volatility, but it is not automatically safe. Borrow rates, depegs, issuer risk, redemption stress, incentives, and exit liquidity can still break the loop.

No, automated tools cannot remove recursive leverage risk. They can simplify transactions, alerts, or unwinds, but collateral, debt, rates, oracles, liquidity, and liquidation rules still drive the position.