Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Intent-based trading can simplify swaps, but the route still deserves inspection.

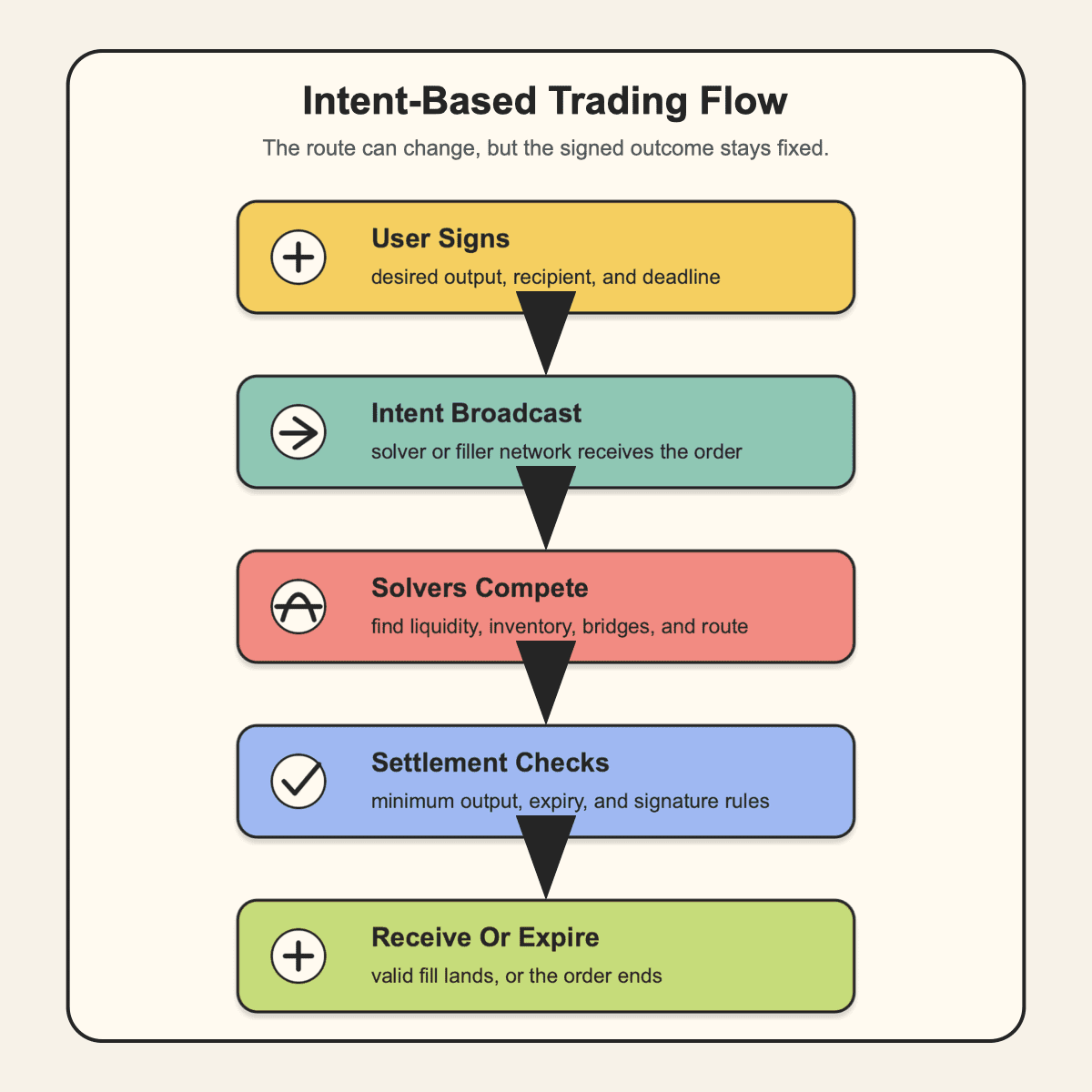

Intent-based trading is a DeFi execution model where you sign the result you want, such as a minimum token output, and solvers or fillers compete to find a route that satisfies those conditions.

That can feel cleaner than clicking through pools, bridges, and gas settings yourself. But the work has not disappeared. It moved to a solver market, a settlement contract, and a quote screen you still need to read carefully.

So before signing, ask what the route really improves. Does intent-based trading improve your final result, reduce failed steps, or hide a different risk behind a smoother button?

Intent-based trading in crypto means you tell a protocol what result you want and let an execution network find a route that can deliver it. You are not manually choosing every pool, bridge, gas payment, or route step.

In a normal wallet swap, you often approve a token and send a transaction against a specific route. In an intent-based swap, you may sign a message that says something like this:

> Swap 1 ETH for at least 2,000 USDC, send it to my wallet, and expire the order if nobody can fill it before the deadline.

That one line carries the trade’s important guardrails. It names the input token, output token, minimum received, recipient, deadline, and sometimes the chain. Solvers, fillers, or market makers then try to make the trade happen without breaking those rules.

The word “intent” is easy to overcomplicate. Your wallet is not signing a wish. It is signing conditions. The route can get clever, but settlement should still respect the result you agreed to.

If the quote screen only shows an expected output, look for the actual floor. Minimum received is the number that protects you when solvers, liquidity, or price movement make the first quote stale.

The model is most useful when routing gets messy. That includes fragmented liquidity, cross-chain moves, gas abstraction, and trades where MEV or price impact can punish a visible transaction. The final result still depends on solver competition, liquidity, fees, and settlement design.

Intent-based trading works by separating your signed desired outcome from the execution path. You sign the condition, then solvers or fillers search for a valid way to settle it.

That signature is usually not the same as sending a raw swap transaction straight into a public mempool. A 2026 Chainlink explainer describes the same three-part split: users specify outcomes, solvers compete offchain, and settlement happens onchain if the conditions are met.

The lifecycle usually follows this shape:

No-fill behavior is part of the design. If the market moves, liquidity dries up, or no solver can profitably satisfy the order, the trade may not execute. That can be annoying, but it is better than receiving a bad fill because the route was forced through anyway.

The wallet prompt is still the pressure point. If the token, recipient, deadline, or signature scope is wrong, solver competition cannot repair the instruction you already signed. The route may be invisible, but your conditions should not be.

Intent-based trading differs from normal DEX trading because the user signs an outcome while an execution market finds the route. A normal AMM swap asks the user to accept a route into a pool or set of pools in that moment.

DEX aggregators sit in the middle. They compare routes before you sign, but many still build a transaction for a specific path. Intent-based DEXs go further by letting solvers or fillers compete to execute the signed order.

Here is the clean comparison:

| Trading Model | What Changes For The User |

|---|---|

| Direct AMM Swap | You trade against one pool, usually with clear pool price impact and direct gas payment. |

| DEX Aggregator | The app compares routes across liquidity sources before building the transaction. |

| Intent-Based DEX | You sign the desired result, then solvers or fillers compete to settle a valid route. |

| Cross-Chain Route | The route may add bridge, destination-chain, liquidity, and refund assumptions. |

| Centralized Exchange | The venue handles execution inside an account, but you take custody and platform risk. |

The difference is not just branding. It changes who controls routing, who pays gas up front, where liquidity can come from, and what failure looks like.

A direct AMM swap can be the cleanest option for a small, liquid pair. A DEX aggregator can improve routing when liquidity is split across venues. Intent-based trading can help when solvers can compete across more sources than your wallet interface can display clearly.

But more abstraction also means more questions. Who can fill the order? How many solvers compete? Does the app show the route? Who captures any surplus when the route beats your minimum? A smoother screen helps only when those checks are visible.

Solvers and fillers are the parties that try to execute an intent-based trade under your signed terms. They may be market makers, routing operators, professional searchers, or protocol-approved participants.

Different systems use different names. “Solver” is common in batch auction and CoW-style language. “Filler” appears in UniswapX-style order flow. Relayers may broadcast or coordinate execution, while professional market makers may provide inventory or RFQ-style liquidity.

Their incentive is straightforward enough:

That last point is easy to miss. A solver is not a charity desk with a logo. If your minimum output is too high, the route is unsupported, or the market moves too far, nobody may fill it.

Solver competition helps when it is real. More independent solvers can push quotes toward better execution because weak routes lose. A small or permissioned solver set can still work, but it may concentrate pricing power, route visibility, and censorship risk.

The best interfaces make solver behavior understandable without exposing every internal calculation. You want to know the quote, minimum received, fill time, fee logic, and failure path. You do not need a PhD in auction design before breakfast, but you do need enough detail to know who is doing the work.

Intent-based trading can help when the execution problem is larger than a simple same-chain swap. It is most useful when route choice, MEV exposure, liquidity fragmentation, or gas handling can change the final amount you receive.

The model shines when solvers can compare more paths than a basic interface would show. That can include onchain pools, private liquidity, RFQ quotes, bridge routes, and inventory held by market makers.

The benefit grows when the trade has several ways to fail. A cross-chain stablecoin move may need a bridge, destination liquidity, gas handling, and a swap. One solver-filled intent can coordinate those pieces while you focus on the final amount.

These are the clearest use cases:

None of that guarantees a better price. It only means the solver market has a real job to do. If the route is easy, deep, and already cheap, the benefit may be small.

Use intent-based trading when it reduces a specific execution problem. Do not use it because the interface sounds futuristic. Crypto already has enough shiny buttons with tiny landmines underneath.

Intent-based trading may not help when the trade is small, liquid, urgent, or unsupported by enough solvers. A plain AMM, aggregator, CEX, or no trade at all may be cleaner.

For a small same-chain swap between deep assets, the extra routing layer may add little. The direct route is already obvious, gas is manageable, and the output difference may be too small to justify more moving parts.

Urgency can also weaken the model. If you need out now, a no-fill or delayed fill may hurt more than a slightly worse direct route.

Be more cautious in these cases:

Thin liquidity is where slick routing can become expensive. If your trade size overwhelms available buyers, you may become someone else’s exit liquidity with a nicer user interface.

Intent-based trading also does not guarantee the best price. It can improve competition for execution, but the result still depends on who sees the order, what liquidity exists, and how the system handles surplus. A route that hides too much can be worse than a simple swap you can inspect.

Intent-based trading fees can appear as gas, protocol fees, solver spread, bridge costs, priority fees, or a worse final quote. Gasless trading only means you may not pay native gas directly.

Someone still pays for execution. A solver may front gas and recover it through spread. A protocol may subsidize costs for a while. A bridge route may charge a fee. The quote may simply arrive with those costs already baked in.

Use this table to separate the cost lines:

| Cost Line | What To Check |

|---|---|

| User-Paid Gas | Whether your wallet pays network gas directly for approval or settlement. |

| Solver-Paid Gas | Whether the solver pays gas and recovers it through the route economics. |

| Embedded Spread | The gap between market value and the output you receive. |

| Protocol Fee | Any explicit interface, protocol, or partner fee. |

| Bridge Fee | Cross-chain routes may pay liquidity, message, or bridge costs. |

| Priority Fee | Fast settlement can require higher transaction priority. |

| Failed Transaction Cost | Some actions may still cost gas if an approval or route step fails. |

| Output Surplus | If execution beats your minimum, rules decide who keeps the extra. |

The final amount received is the real bill. A route with no visible gas line can still cost more than a direct swap if the spread is worse.

This is why “gasless” deserves a raised eyebrow, not panic. It can be useful UX, especially across chains or for wallets without native gas. Just compare the final output against another route before assuming free execution has arrived.

Intent-based trading can reduce some MEV exposure by changing how an order reaches execution. It may avoid a normal public-mempool swap path, use private routing, or settle through auctions that make sandwiching harder.

That helps, but a private or auctioned route can still leak value in other ways. MEV is a market-design problem, not one switch the app can flip off. Order flow can still be valuable, and whoever sees or controls that flow may have an edge.

The safety questions are specific:

This is where PVP trading becomes useful shorthand. In adversarial markets, other actors may profit from your timing, slippage, route visibility, or urgency. Intent-based trading can reduce some angles, but it can also move the contest into solver networks and private order flow.

Smart contract risk stays on the table too. Settlement contracts, approvals, routing contracts, and wallet signatures all matter. If a route is opaque, the minimum received and signature scope become even more important.

The best version of intent-based trading gives you fewer public execution leaks and stronger output guarantees. The weak version gives you a prettier path into the same old trade traps.

Intent-based trading across chains lets you state a destination result while solvers handle bridge, swap, liquidity, gas, and settlement steps. It can turn a multi-tab bridge journey into one signed outcome.

For example, you may have USDC on Arbitrum and want USDC on Base. A cross-chain intent may let you sign the desired destination amount and chain, while solvers figure out the bridge or liquidity route.

That convenience changes the failure path:

| Cross-Chain Question | Why It Changes The Risk |

|---|---|

| Destination Token | The received token may be native, bridged, wrapped, or issuer-specific. |

| Destination Chain | The app must support the chain, wallet, gas, and settlement path. |

| Bridge Or Liquidity Route | The solver may use a bridge, inventory, pools, or several steps. |

| Chain Finality | A source-chain reorg or delay can affect settlement timing. |

| Refund Path | The route should explain what happens if no valid fill arrives. |

| Route Support | Unsupported assets or chains can lead to no-fill behavior. |

Cross-chain intents can reduce manual work. They can also make it harder to see which bridge, pool, or inventory source carried the risk.

That means you should not read “intent-based” as “safer than a bridge” by default. It may be safer for some routes because fewer manual steps reduce user error. It may be riskier if the destination token, refund path, or route operator is unclear.

The clean habit is to inspect the received asset, destination chain, minimum output, expiry, and refund rule. A smooth cross-chain wrapper is still a wrapper around real settlement risk.

An intent-based trading quote should be checked like a signed instruction, not like a casual price preview. The exact fields decide whether settlement is valid.

Start with the wallet. Use the official app URL, confirm the wallet prompt belongs to the route you opened, and read the approval or signature scope. CryptoProcent’s wallets section is useful background for wallet types, signing flow, and custody before you trust a swap prompt.

The danger is not only a bad price. A sloppy signature can approve the wrong spender, send funds to the wrong recipient, or leave you waiting for a route that never fills.

Run this checklist before you sign:

Then compare one alternative route. It does not need to be perfect. It just gives you a sanity check against a quote that looks too confident.

If the trade is large, split it or test with smaller size first. If the route is cross-chain, verify the destination token before moving real funds. If the wallet prompt looks broader than the trade requires, stop. The best quote is not worth a bad signature.

Intent-based trading comes with a small vocabulary pile. Learn the terms once, and the quote screen gets less theatrical.

An intent is the signed desired outcome. It can include token, amount, recipient, chain, minimum received, deadline, and other limits.

A solver is an actor that tries to find a valid route for that intent. A filler is a similar role in order-flow systems where someone fills the signed order.

A relayer helps broadcast or coordinate execution. It may not provide liquidity itself. An RFQ, or request for quote, asks market makers to quote a trade directly.

A batch auction groups orders before settlement. It can help match compatible trades and reduce some ordering games. A Dutch auction changes price over time to encourage fillers to compete.

A settlement contract checks whether the final execution satisfies the signed conditions. Minimum received is the floor output you accept. Expiry is the deadline after which the order should no longer fill.

These terms are useful because they separate the user promise from the execution machinery. When a protocol uses different labels, map each label back to the same questions: who routes, who fills, who pays, who checks, and what happens if nobody can execute.

No. Intent-based trading can improve execution when solver competition and liquidity are strong, but it does not guarantee the best price for every trade.

The final result depends on route support, solver access, market movement, fees, spread, and your minimum received setting. Compare the quote against another route before assuming the solver market beat everything else.

No. A DEX aggregator usually compares routes before building a swap transaction, while intent-based trading lets solvers or fillers compete to satisfy a signed outcome.

The two models can overlap. Some aggregators use intent-style execution for certain routes, and some intent-based DEXs compare liquidity sources like aggregators. The difference is who controls execution after you sign.

Sometimes. Intent-based trading can feel gasless when the solver pays settlement gas or the app abstracts gas from the user.

That does not make execution free. The cost may appear in spread, a protocol fee, route economics, bridge fees, or the final output. Gasless is a UX feature, not a law of physics.

Yes. An intent-based trade can fail, expire, or receive no fill if no solver can satisfy the signed terms.

It can also fail because of unsupported chains, weak liquidity, settlement issues, stale quotes, or wallet approval problems. A no-fill is often better than a bad fill, but you still need to know the expiry and refund path.

Not automatically. Intent-based trading can reduce some manual bridge steps, but cross-chain routes still carry destination-chain, liquidity, finality, token-form, and refund-path risk.

It may be cleaner for a supported stablecoin move with a clear quote. It may be worse if the app hides which route fills the destination side or what happens when settlement stalls.

Common examples include CoW Swap, UniswapX, and 1inch Fusion, with cross-chain intent products also appearing across routing and chain-abstraction tools.

Use examples as starting points, not permanent rankings. Supported chains, solver sets, fees, and order types change. Check current product documentation and the exact wallet prompt before using real size.

Start with intent-based trading as a quote-checking tool, not a belief system. The model is useful when it solves a visible execution problem, and risky when it asks you to trust hidden routing without enough detail.

Use a small same-chain swap first. Compare the final output against a direct AMM or aggregator route. Then inspect the minimum received, expiry, approval, token contract, and route details.

If the first quote fails or expires, that is useful information. It may show weak solver demand, thin liquidity, or an expiry window that is too tight for the market.

Bad fills teach faster than branding.

For larger trades, avoid going all in through one unfamiliar route. A full-port trade needs extra care because one bad fill, failed route, or wide spread can hit the whole position.

Cross-chain trades deserve a separate test. Confirm the destination token contract, destination wallet, gas situation, and refund path before you let convenience hide the route.

The clean starting checklist is short:

Intent-based trading is promising because it moves routing into a competitive execution layer. It is still your signature. Read the conditions before the solver market handles your funds.