Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

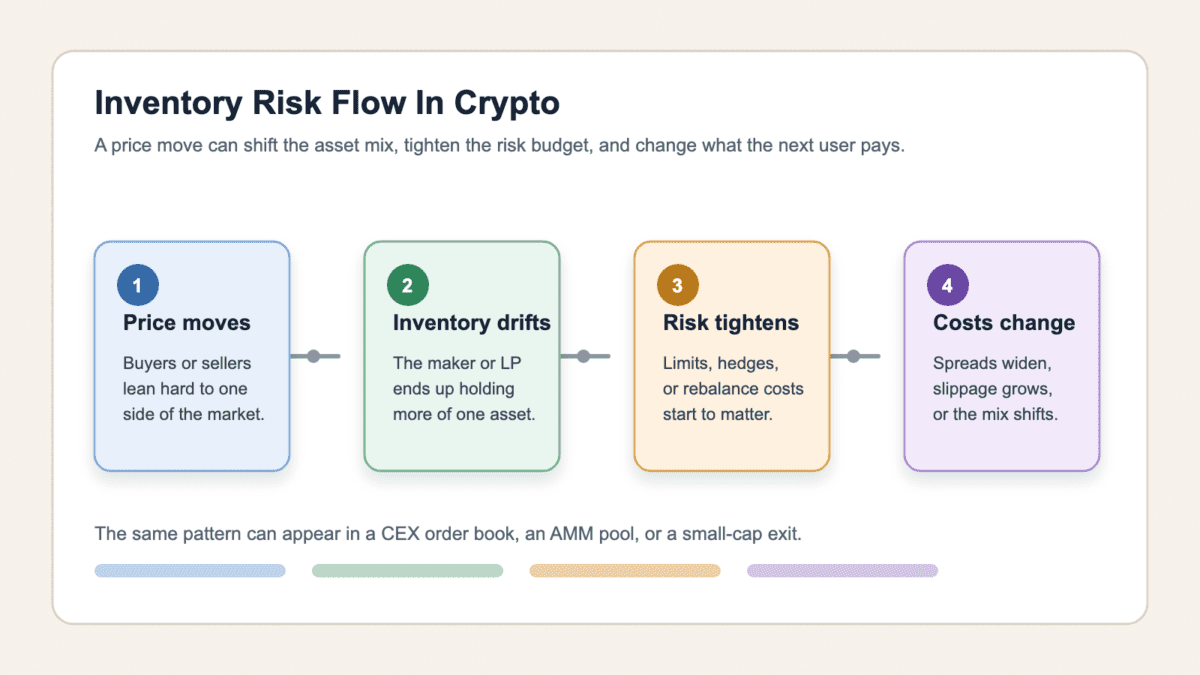

Inventory risk explains why liquidity is never free.

Inventory risk is the chance that a crypto market maker, liquidity provider, or trader gets stuck holding the wrong asset mix after price moves.

That sounds like backstage plumbing, but it reaches normal users fast. It can show up as wider spreads, worse fills, LP losses, out-of-range positions, and fee dashboards that look happier than the actual portfolio.

Inventory risk means the asset you hold while providing liquidity can become the asset you wish you did not hold. In crypto, “inventory” usually means tokens, stablecoins, or derivatives exposure held while quoting markets, supplying a pool, or trying to enter and exit a position.

It is not warehouse inventory risk with a blockchain sticker on it. No one is worried that a pallet of ETH is stuck behind the loading dock. The problem is price movement before the holder can sell, hedge, or rebalance.

Timing is the whole point. A position may look balanced when the quote goes live, the pool is funded, or the trade is opened. Then flow arrives from one side, price moves, and the holder is left with more exposure than planned.

You can see the same idea in three common crypto settings:

The mechanics differ, but the pain rhymes. Someone provides liquidity, takes the other side for a moment, and then price keeps moving. If that person or pool cannot rebalance at a fair cost, the risk becomes real money.

Fee income can mislead. A market maker can earn spreads and still dislike the position it now holds. A DeFi LP can earn swap fees and still underperform a simple hold. A trader can enter cleanly, then discover the exit is where the real market lives.

Inventory risk is the thread tying those examples together. It connects market-maker quote changes, LP impermanent loss, and ugly small-cap exits without pretending they are identical.

Inventory risk hits ordinary traders through the price they can actually get. When a market maker feels safe holding inventory, the bid-ask spread can stay tighter and displayed depth can look deeper. When the risk rises, quotes often get wider, smaller, or disappear from the book.

That is where a backstage risk becomes your fill. A token might show a last traded price of $1.00, but the next meaningful buy could be $1.03 and the next meaningful sell could be $0.97. The screen says “price.” The book says “good luck.”

The visible effects are usually simple:

Take a small-cap token with thin depth. A $500 test buy may fill close to the quote, so the market feels liquid. A $10,000 exit can be a different beast if there are few real bids below you. That is where exit liquidity stops being a meme and becomes the question: who is actually taking the other side?

Inventory risk does not mean every bad fill is sinister. It means liquidity providers price the chance that they get stuck with exposure. If the token is volatile, depth is thin, or order flow is one-way, they demand more protection. You pay for that protection through worse execution.

Market maker inventory risk starts with a simple job: quote bids and asks so others can trade. The market maker earns the spread when flows are balanced, but flows rarely behave politely. Buyers may keep lifting offers, sellers may keep hitting bids, and the market maker can end up holding too much of one asset.

A Bank for International Settlements market-making paper frames this job around earning spreads while managing inventory, funding, and price risk. Crypto adds speed, fragmented venues, weekend trading, and token-specific shocks. The math can get formal, but the business problem is plain: do not become the unwilling bag for a moving market.

Market makers use several controls when inventory gets lopsided:

Quote skew means the market maker changes prices to lean away from a position it does not want. If it already owns too much of a token, it may quote a lower bid and a more attractive ask. That nudges sellers away and buyers toward taking inventory off its hands.

Spread widening is the blunt version. When volatility jumps, the market maker may widen both sides because any fill can become stale fast. Fast markets punish stale quotes. Crypto, being crypto, likes to test that before breakfast.

None of this makes market makers public utilities. They provide liquidity when the spread, fees, or issuer agreement pays them enough for the risk. When conditions turn hostile, they can reduce size, hedge harder, or pull back. The trader sees the result as a thinner book and a worse fill.

Inventory risk in DeFi liquidity pools appears when an AMM changes the LP’s token mix as traders swap against the pool. You are not manually quoting bids and asks, but the pool is still taking the other side of trades. That means your inventory can drift.

In an ETH/USDC pool, a rising ETH price can leave the LP with less ETH than a simple holder. In a falling token/USDC pool, the LP can end up with more of the weaker token. Fees may soften that hit, but they are not magic dust. Net return is what counts.

The table below maps the same idea across common crypto roles. It keeps the wording broad because the exact risk depends on venue design, token quality, and position size.

| Context | How Inventory Risk Shows Up |

|---|---|

| CEX market maker | Uneven fills create too much long or short exposure, so quotes change. |

| DEX liquidity provider | Swaps push the pool position toward one asset, which can lag holding. |

| Active trader | A position looks liquid on entry but becomes expensive to exit. |

| Token project | Paid liquidity may thin out when volatility makes inventory too costly. |

This is also where inventory risk and impermanent loss overlap in user experience. Impermanent loss describes LP underperformance versus holding after pool prices move. Inventory risk is the broader idea that the asset mix itself can become unfavorable before you can rebalance.

Inventory risk is broader than impermanent loss. Impermanent loss is a DeFi LP result. Inventory risk can also affect market makers, active traders, OTC desks, and anyone else temporarily holding exposure while liquidity is being provided.

The common LP complaint is still fair: “I earned fees, so why did I lose versus holding?” The answer is that fees are only one line. You also need the token mix, price move, range status, gas, rebalancing cost, tax friction, and opportunity cost.

Concentrated liquidity makes this sharper. A tight range may collect more fees while price stays inside it. But if price runs through the range, the position can move heavily into one side and stop earning new fees. Wide ranges can be less exciting, but sometimes boring is just risk management wearing sensible shoes.

Inventory risk gets worse when price moves faster than liquidity can adjust. The danger is not just volatility. It is volatility plus weak exits, slow rebalancing, fragmented venues, and one-sided flow.

Small-cap and meme-coin markets show this clearly. During a rush, buyers can push price through thin offers. During the turn, sellers discover that the bid side was more decorative than durable. Life in the trenches teaches this lesson quickly, usually with expensive tuition.

Watch for conditions that make inventory harder to manage:

This is also how a trader becomes a bagholder risk case study. You buy what looks like momentum, the other side disappears, and the inventory you planned to flip becomes the inventory you now have to explain to yourself.

Inventory risk is not proof of a hard rug, spoofing, or market manipulation. Those are separate claims. But liquidity disappearing during stress can create the same user feeling: the door is still there, but the exit price has moved down the street.

Traders and LPs can reduce inventory risk by sizing positions around real exit conditions, not just entry excitement. You cannot erase the risk, but you can stop pretending the quoted price is the whole market.

For spot traders, the first control is boring and effective: check the spread, depth, and recent volume before sending size. If a market order would walk the book, use smaller orders, limit orders, or no trade. The best fill is sometimes the one you did not chase.

Before entering a trade or LP position, run these checks:

For LPs, inventory risk management means comparing the LP position with holding the assets outright. Check expected fees against impermanent loss, gas, range movement, and rebalancing frequency. A pool can show attractive fee APR while still losing the comparison against holding ETH, BTC, or stablecoins.

Range choice changes the workload. Tight ranges can make sense for active LPs who monitor positions and accept rebalancing work. Wider ranges may fit those who want less management. Full-range positions still carry price exposure, but they do not demand the same constant attention.

Hedges can help, but they add their own teeth. Perpetual futures, borrowing, or options can offset part of the exposure. But perps add funding costs, liquidation risk, basis risk, and changing delta as the LP position shifts. If your hedge needs constant babysitting, your “passive yield” has found a second job.

Small-cap traders should also think about PVP flow before assuming someone else will absorb the exit. If everyone is trading the same chart for the same quick move, inventory risk can become zero-sum very fast.

Common inventory risk mistakes come from reading one metric and ignoring the position behind it. Fees, APR, volume, and tight spreads can all look useful. They become dangerous when users mistake them for proof that risk is under control.

The usual shortcut is to look at the number that feels easiest. LP fees look clean on a dashboard. A tight spread looks like healthy liquidity. A hedge label sounds careful. None of those tells you what asset you may hold after the market moves.

The table below separates the popular shortcut from the reality that usually decides the outcome.

| Mistake | Reality |

|---|---|

| LP fees are profit | Fees matter only after price movement, gas, rebalancing, and hold-versus-LP performance. |

| Delta-neutral means no risk | The hedge can drift, funding can bleed, and liquidation can still happen. |

| Tight ranges are always better | They can earn more fees, but they demand more monitoring and can go out of range. |

| Wider spreads mean manipulation | Spreads can widen because inventory risk, volatility, and hedging costs rose. |

| Market makers always absorb the other side | They manage their own risk and can reduce size when flow gets hostile. |

The most common trap is treating LP yield like a savings account. It is not. You are taking price, inventory, routing, execution, and management risk in exchange for fees.

That does not make LPing wrong. It means the comparison is against holding, staking, lending, or doing nothing. If the LP position needs constant rebalancing, pays less after gas, or leaves you with more of the weaker token, the headline yield has not done its job.

Another trap is blaming every ugly fill on a villain. Crypto has plenty of villains, no need to invent extras. Wider spreads and thin depth can come from normal risk controls during a fast move. Claims about manipulation need proof beyond a painful chart.

Start with the asset mix, not the headline return. Inventory risk is about what you may be left holding when price moves and liquidity changes. That makes it a practical pre-trade check, not a textbook term to memorize.

The routine is deliberately simple because the risk usually shows up in simple places. Check what you can exit, what you may end up holding, and what the position costs to manage when conditions stop being friendly.

Before trading or LPing, use this short routine:

Then ask one plain question: if the market moves against this position, what asset am I likely to hold more of? If the answer makes you uncomfortable, size down, widen the range, wait for better depth, or skip the setup.

For traders, this means matching order size to real depth instead of the last traded price. For LPs, it means checking the token mix, range status, fee history, and rebalancing cost before calling the yield attractive. For hedged positions, it means asking whether funding, liquidation risk, and basis risk are worth the extra work.

Inventory risk is not a reason to avoid every trade or LP position. It is a reason to price liquidity honestly. Someone holds the other side for a moment. Make sure you know when that someone is you.

No. Inventory risk is broader. Impermanent loss is one DeFi LP outcome where a pool position underperforms simple holding after prices move. Inventory risk also applies to market makers, traders, and desks that hold exposure while providing liquidity or executing trades.

Market makers widen spreads when inventory risk rises because each fill can leave them with unwanted exposure. A wider spread gives them more room to cover volatility, hedging costs, and the chance that price moves before they can rebalance.

Yes, liquidity providers can hedge inventory risk with perpetual futures, but it is not beginner-safe. A perp hedge can add funding costs, liquidation risk, basis risk, and exposure that changes as the LP position rebalances.

No. Inventory risk can explain wider spreads, smaller quotes, and thinner books during volatility. It does not prove manipulation by itself. Manipulation claims need stronger evidence than a bad fill or a chart that moved too fast.

Look at spread, order-book depth, recent volume, holder concentration, AMM pool size, and route price impact. Inventory risk is higher when a small order moves price, volume is one-sided, and exits depend on new buyers arriving.

Inventory risk is not automatically bad for normal crypto traders. It is a cost signal. If spreads are tight, depth is real, and size is reasonable, the risk may be manageable. If liquidity is thin, it can turn a simple trade into an expensive exit.