Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Maker-taker rebate basics without the hidden fee trap.

A maker-taker rebate is an exchange fee model where resting orders may earn maker pricing, while immediately matched orders usually pay taker fees.

The fee model changes real trading cost because a cheap fee table can still lead to expensive execution. Order type, order-book price, post-only settings, partial fills, fee tier, spread, slippage, and product type all change the final cost.

Maker and taker are liquidity roles, not buyer and seller labels. You can buy as a maker, sell as a maker, buy as a taker, or sell as a taker, depending on how your order meets the book.

In crypto, a maker-taker rebate means the exchange prices your trade by how your order interacts with the order book. If your order rests and waits, it may qualify for maker pricing. If it matches immediately, it usually gets taker pricing.

The maker side adds liquidity. A maker order gives other traders something to hit later, such as a resting bid to buy BTC or a resting ask to sell ETH. The taker side removes liquidity because it accepts an existing bid or ask right away.

Rebate can mean a few different things. Some venues simply charge a lower maker fee than taker fee. Some charge zero maker fee on certain pairs or tiers. A smaller group uses a negative maker fee, which means a qualifying maker order can receive a credit when it matches.

The exchange is not handing out coupons with candles. Rebate treatment is conditional. It can depend on the pair, region, account tier, 30-day volume, product type, promotion, and whether the order really rested before matching.

Take a simple ETH order-book example. The best bid is $3,000 and the best ask is $3,002. If you place a market buy, you take the ask and usually pay the taker fee. If you place a limit buy at $3,000 and it waits on the bid, you add liquidity and may receive maker pricing when someone sells into it.

The important word is may. Maker pricing only applies when the venue rules and actual fill support it. A button labeled “limit” does not bless the trade. The match engine has the final vote, as usual, and it is not known for being sentimental.

Exchanges use maker-taker rebates to pull more resting orders into the book. A deeper book gives buyers and sellers more orders to trade against, tighter quoted prices, and less panic when size appears.

On an order book, bids are resting buy orders and asks are resting sell orders. The spread is the gap between the highest bid and lowest ask. Market depth is the amount of size available at and around those prices.

| Role | What Happens on the Order Book |

|---|---|

| Maker | Places an order that rests and adds visible liquidity. |

| Taker | Matches against resting liquidity and removes it. |

| Rebate | Rewards the maker side when the venue wants more resting flow. |

The maker-taker model tries to shape behavior. Makers give the market quotes to work with, so exchanges may reward them. Takers demand immediacy, so they usually pay more for the privilege of getting filled now.

But liquidity is not automatically good liquidity. A book can look deep until volatility arrives, then quotes can widen, vanish, or sit too far from the fair price. A maker order resting in a weak book can become exit liquidity for someone leaving a bad trade.

So the rebate only makes sense beside market quality. Tight spreads, real depth, steady fills, and reliable order handling are more useful than a headline maker rate that only works when no one wants your side of the trade.

Maker-taker rebate math looks tiny until you trade often. A few basis points can decide whether a scalping setup survives, but the fee line is only one part of the round trip.

A neutral round trip makes the trade-off clearer. Suppose a trader opens and closes a position on the same pair. The exact fee schedule is not the point here. The useful question is how execution changes the trade path.

| Execution Path | What It Changes |

|---|---|

| Taker entry, taker exit | Pays immediacy twice and needs the price move to beat both fees. |

| Maker entry, taker exit | Reduces one side of the fee drag, but still pays for the fast exit. |

| Maker entry, maker exit | Can lower fee drag most, but both fills depend on waiting. |

| Maker order misses | Saves the fee, but may miss the trade or enter later at a worse price. |

This is why active traders model fees before they trust a backtest. A setup that looks profitable before costs can fall apart after entry fee, exit fee, spread, missed fills, and slippage. The smaller the expected edge, the faster fees eat it.

A maker rebate helps most when it reduces a cost on a fill you wanted anyway. It helps less when you move your price too far away from the market just to qualify. Saving a small fee while missing the actual move is not disciplined trading. It is fee cosplay.

The spread can erase the rebate before the order fills. If the best bid and ask are wide, posting passively may only earn maker pricing at a worse effective price. If the market moves away, the fill may never happen.

Round-trip thinking keeps the rebate honest. Ask what the full trade costs to enter and exit, not just whether one side has a shiny maker rate.

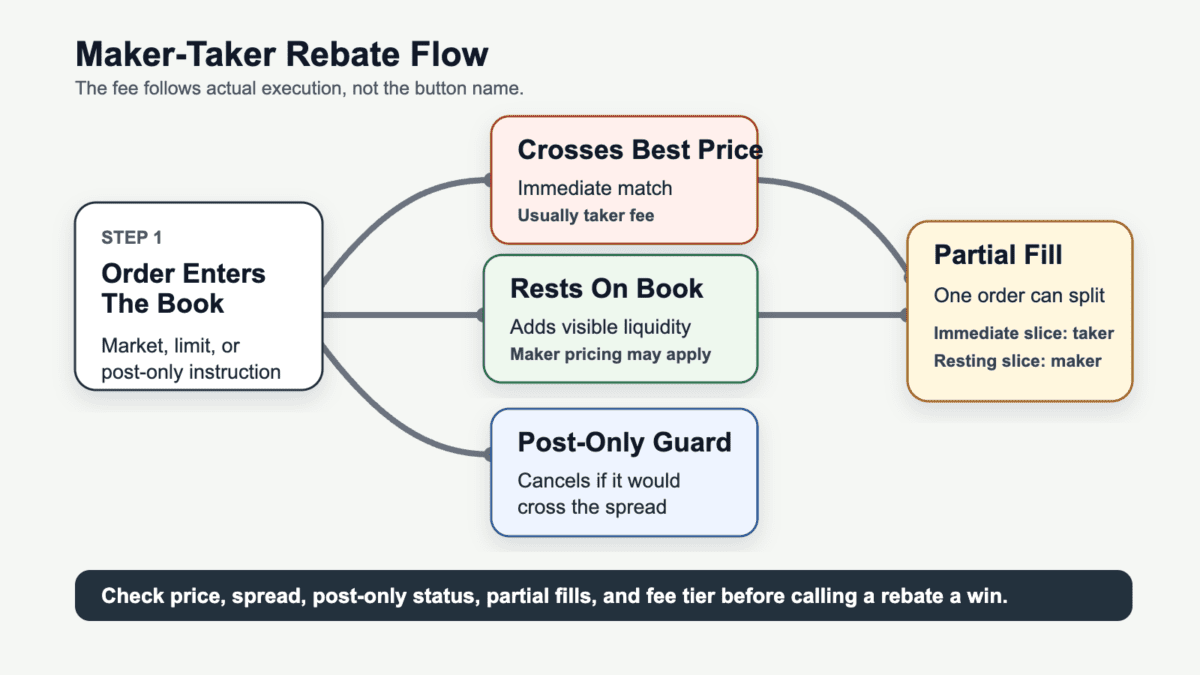

A limit order can miss the maker-taker rebate when it is marketable. That means your limit price crosses the best available bid or ask and matches immediately.

Market orders are usually straightforward. They accept available liquidity now, so they usually pay taker fees. A normal limit order is more flexible. It can rest as a maker order, or it can hit the book as a taker order if the price is aggressive enough.

For example, if the best ask is $3,002 and you place a limit buy at $3,005, your order can match immediately up to your limit. The order used a limit button, but the execution removed liquidity. That is taker behavior.

Use these checks when your goal is maker treatment:

_Flow diagram showing how actual execution, not the order button, controls maker or taker fee treatment._

Post-only is the cleanest guardrail for maker intent. If the order would immediately match, the venue usually cancels or rejects it instead of letting it become taker. That protects the fee outcome, but it also means you might not trade.

Time-in-force settings can also affect behavior. An immediate-or-cancel order is built for speed, not passive quoting. A good-til-canceled limit order can rest longer, but it still needs the price to avoid crossing the book at entry.

The key line is simple: execution decides the fee, not the order button. If you need a fill now, you may pay taker. If you need maker pricing, you may need patience, a passive price, and a willingness to miss.

Partial fills can split a maker-taker rebate across one order. One slice may match immediately as taker, while the remaining slice rests and later receives maker pricing.

Imagine you place a limit buy for 10 ETH. The price crosses enough resting asks to fill 3 ETH right away. The remaining 7 ETH sits on the book as a bid. If sellers later hit that bid, the second slice may qualify for maker pricing.

| Order Slice | Likely Fee Treatment |

|---|---|

| Immediate 3 ETH match | Taker fee, because it removed resting liquidity. |

| Remaining 7 ETH resting on book | Maker pricing if it later matches while resting. |

The trade can feel confusing because the interface may show one order, one price limit, and one trade idea. Under the hood, the match engine sees separate execution events. Each slice gets classified by what happened when it filled.

Venue rules differ on how partial fills appear in the order history. Some dashboards show maker and taker lines clearly. Others require you to open fill details, export a trade report, or compare the effective fee after settlement.

Partial fills also affect tax and accounting cleanup because the trade history may show several fills instead of one neat entry. That is normal order-book behavior, but it means your cost model should read fill-level data rather than only the parent order.

So inspect fills after trading. If your strategy assumes maker fees but your fills are half taker, the model is already lying to you. Polite spreadsheet lies are still lies.

A maker-taker rebate is worth chasing when the fee benefit is larger than the execution risk. That usually means the trader already cares about spreads, queue position, fill probability, and round-trip cost.

Long-term investors may not need to optimize every fill. If you buy occasionally and hold, the bigger risk may be using the wrong venue, trading too often, or ignoring withdrawal and custody costs. A small maker discount does not rescue a messy plan.

Frequent traders, scalpers, arbitrage bots, and market makers care more. They repeat trades often, so tiny fees compound. They also face more ways to get hurt, including adverse selection, missed fills, latency, and a crowd of other traders trying to post first.

The rebate is usually more relevant when these conditions line up:

Crowded short-term trades can turn into PVP flow fast. Everyone wants passive fills, lower fees, and a clean exit. That can make queue position and timing more important than the advertised rebate.

Large orders add another wrinkle. Posting passively can reduce fee drag, but it may reveal interest, fill slowly, or leave the trader chasing the market. Splitting size can help execution, but it can also create more fills to track and more chances to pay the wrong side.

The best use of a maker-taker rebate is boring: reduce a cost on trades you already understand. The worst use is changing your whole execution style because a fee table made the word “rebate” look like free edge.

Comparing maker-taker rebate offers across exchanges starts with the total cost, not the lowest maker number. A cheap maker rate is useful only if the venue, pair, product, and execution quality fit the trade.

Start with the actual market you plan to use. Fee schedules can differ by spot pair, stablecoin pair, futures contract, account tier, region, and promotional rule. A headline rate on one page may not apply to the order in front of you.

Use this checklist before you trust an exchange fee table:

A zero-fee or rebate claim can still hide cost. The spread may be wider, the pair may be thin, or the withdrawal path may be expensive. The product may require margin, funding payments, or contract rules that do not apply to ordinary spot trades.

Custody also belongs in the cost check once funds leave the venue. If a trading setup requires frequent transfers, compare withdrawal networks and the wallet process, not only the trading fee. CryptoProcent’s wallets category is useful when storage and transfer workflow become part of the exchange choice.

Do not rank exchanges by one fee side. Compare the maker rate, taker rate, average fill quality, and what happens after the trade settles. A venue with a slightly higher maker fee can still be cheaper if it has better depth, tighter spreads, and fewer transfer headaches.

Maker-taker rebates in spot, futures, and perpetuals can look similar in a fee table, but the surrounding costs are different. Spot trading is the simplest version because the fee applies to buying or selling the asset itself.

In spot markets, you usually compare maker fee, taker fee, spread, depth, and withdrawal cost. There is no funding rate on the position. There is also no liquidation price unless the venue wraps the trade in margin.

Futures and perpetuals add more moving parts. Fees may be charged on notional value, which means the fee is based on contract exposure rather than only the cash you posted as margin. A rebate can reduce the trading-fee line while funding, liquidation risk, and margin rules still dominate the outcome.

For a current official example, Gemini’s ActiveTrader fee schedule lists a -0.01% maker fee for qualifying derivatives volume tiers and notes that those maker orders receive a rebate when matched.

That example shows why product type cannot be ignored. A negative maker fee may be real, but it can sit inside a margin product with funding payments, margin interest, liquidation fees, or contract-specific settlement rules. The rebate is one line, not the whole invoice.

Perpetual traders should keep funding separate from maker and taker fees. Funding is a periodic payment between longs and shorts. Trading fees are charged when orders execute. Mixing them together makes the strategy look cleaner than it is.

Spot users can still learn from derivatives fee tables, but they should not copy the conclusion. The same phrase, maker rebate, can produce a very different result once notional exposure and margin risk enter the room.

Maker-taker rebate mistakes usually come from trusting labels too much. A market order, limit order, post-only toggle, zero-fee claim, or VIP tier can all mean less than the actual fill.

The first mistake is buying or selling with market orders by habit. Market orders can be useful when speed is worth the cost, but they usually remove liquidity and pay taker fees. If the spread is wide, the execution price may hurt more than the visible fee.

The second mistake is assuming every limit order earns maker pricing. A marketable limit can cross the book immediately. If you wanted maker treatment, the price and post-only setting need to support that goal.

Watch for these common traps:

Small balances deserve extra caution. A tiny rebate can be meaningless when the trade leaves dust balances, creates awkward leftovers, or costs more to move than it saves.

The fix is to check the order after it fills. Look at whether the fill was maker or taker, what fee was charged, whether the spread changed the effective price, and whether your model counted the same cost. If not, fix the model before scaling.

A maker-taker rebate should make a good execution plan slightly better. It should not be the reason the trade exists.

A maker-taker rebate in crypto is a fee setup where orders that add resting liquidity may receive lower maker pricing or a rebate, while orders that remove liquidity usually pay taker fees. It is a market-structure incentive, not a guaranteed trading profit.

A maker-taker rebate can be a lower fee, but not always. Some venues charge a reduced maker fee, some charge zero, and some use negative maker fees that credit qualifying maker fills.

Yes. A limit order can miss the maker-taker rebate if it is priced aggressively enough to match immediately. The order may be a limit order by input, but taker by execution.

Yes. One order can split maker-taker rebate fees when part of it fills immediately and the rest sits on the book. The immediate slice can be taker, while the resting slice can later receive maker pricing.

Sometimes. Normal traders may get lower maker fees or zero maker fees on certain venues, pairs, or tiers. The strongest rebates often require higher volume, specific products, or account conditions.

No. Chasing a maker-taker rebate is only worth it when the fee benefit beats spread, slippage, missed-fill risk, funding, withdrawal cost, and time. A smaller fee can still produce a worse trade.

Start by checking the trade you are actually about to place. Fee pages are useful, but the order preview, book, and fill report tell you what happened to your money.

Start small when you test a venue or product. The first goal is not to win the rebate leaderboard. It is to confirm that your order settings, fill reports, and fee tier behave the way your strategy expects.

Use a small workflow before you scale size:

If the rebate is smaller than the execution risk, skip the optimization. A missed fill, wide spread, or bad exit can cost more than the maker fee ever saved.

Then keep records. Track expected fee, actual fee, maker or taker status, spread at entry, and whether the order filled as planned. Do the same for exits, because a cheap maker entry can still lead to an expensive taker exit.

That small habit will tell you whether the maker-taker rebate is helping your strategy or just giving the fee table something pretty to say. If the logs keep showing taker fills, missed entries, or worse prices, change the execution plan before adding size.