Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Learn how market making vaults turn deposits into trading-risk yield.

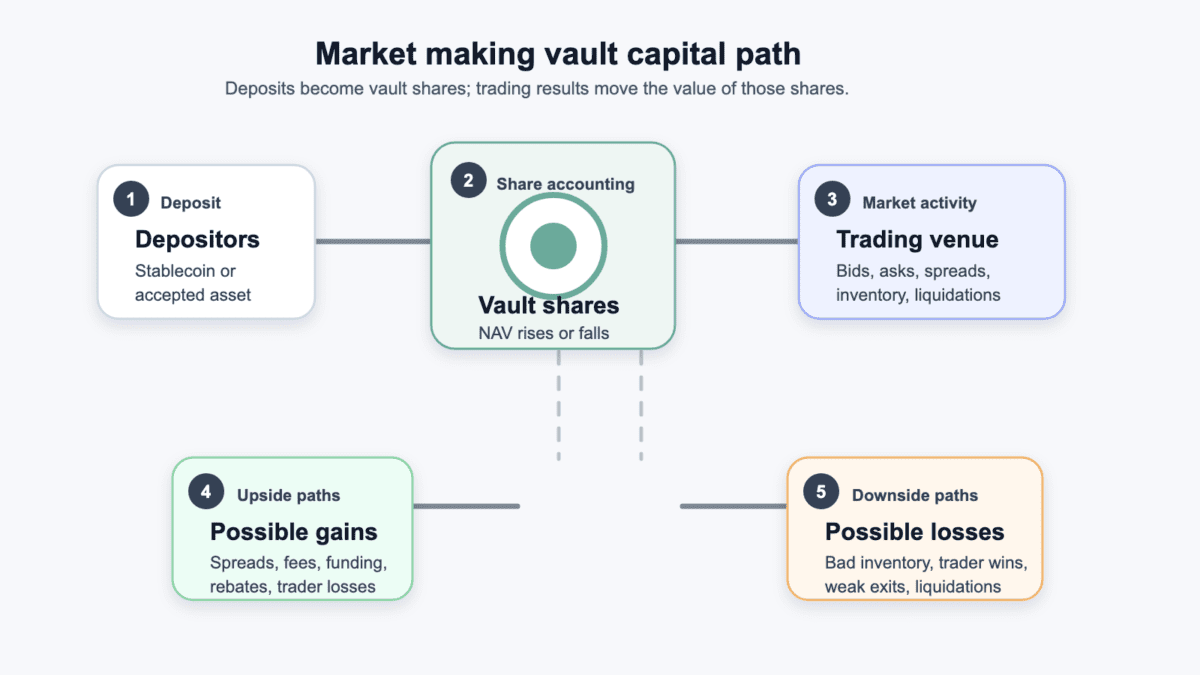

A market making vault is a crypto vault that pools user deposits to provide trading liquidity and share the resulting profit or loss.

The appeal is easy to see. A user can deposit stablecoins or another accepted asset, receive vault shares, and gain exposure to a strategy that normally belongs to market makers, trading desks, or automated liquidity systems.

The risk arrives through the same route. A market making vault is a pooled trading-risk product. Its APY can come from spreads, fees, funding, liquidations, incentives, or traders losing against the vault, and those same paths can cut the other way.

A market making vault in crypto is a pooled vault that uses depositor capital to provide liquidity on a trading venue. The vault may quote bids and asks, hold inventory, earn maker fees, capture spreads, take funding payments, or absorb trader flow.

The key word is pooled. Instead of one professional market maker using its own balance sheet, many depositors provide capital to one vault. The vault then tracks each depositor’s share of the total value. If the vault makes money, each share may become worth more. If the vault loses money, each share may become worth less.

This is why the label can mislead beginners. A vault may accept USDC, but that does not make the position a savings account. The stablecoin is the input. The strategy can still take market risk after the deposit lands.

A simple example helps. A perp DEX may need liquidity so traders can open and close positions. A market making vault can place orders around the market price, earn spread or fees when trades happen, and manage exposure as prices move.

That can be useful for the venue and profitable for depositors in good conditions. But the vault is also closer to a trading desk than a plain lending account. It is doing market work with shared capital, and shared capital also shares the bad days.

A market making vault works by turning a deposit into a claim on a pooled strategy. The user deposits an accepted asset, the vault records ownership, then a protocol, automated system, or manager uses the pooled capital to support trading activity.

Depositor capital usually becomes a vault share, receipt balance, or ownership record. That share is not a fixed claim on the original deposit amount. It is a claim on the vault’s net asset value, often shortened to NAV.

NAV sets the price for deposits and withdrawals. If the vault has more assets after fees, spreads, and profitable trades, each share may be worth more. If open positions lose money, inventory falls, or exits cost more than expected, share value can drop.

Market making means the vault tries to stand ready on both sides of a market. It may place bids to buy and asks to sell. The gap between those prices is the bid-ask spread.

The hard part is inventory. If the vault buys too much of an asset before price falls, it can hold unwanted exposure. If it sells too much before price rises, it can miss upside or need to rebalance at worse prices.

Some market making vaults are protocol-managed. Others are user-managed vaults where a leader, manager, or external strategy operator controls trading logic under platform rules.

The setup changes your checklist. A protocol vault raises questions about code, parameters, governance, and market design. A user-managed vault raises questions about manager skill, incentives, fees, personal stake, and whether the track record is long enough to mean anything.

Withdrawals add one more layer. Some vaults may allow quick exits. Others can use cooldowns, queueing, withdrawal windows, or slippage controls. Read that path before depositing. Panic is a poor time to learn menu design.

Market making vault yield comes from trading activity, not from a fixed savings rate. Different vaults combine different sources, so the displayed APY is only useful after you know what is feeding it.

The main sources can look clean on a dashboard. Each one has a failure path:

| Return Source | What Can Go Wrong |

|---|---|

| Bid-ask spread | The spread can shrink, volume can fade, or the vault can quote poorly. |

| Maker fees or rebates | Fee rules can change, and rebates may not cover losses. |

| Funding payments | Funding can flip direction and become a cost. |

| Liquidation participation | Liquidation events can create profits or expose the vault to bad debt. |

| Trader losses | Traders can also win, leaving the vault with negative P&L. |

| Protocol incentives | Incentives can end, dilute, or depend on token prices. |

This is different from broad yield farming, where yield may come from reward emissions, lending demand, trading fees, or campaign incentives. A market making vault can sit inside the wider yield world, but its core engine is market liquidity and trading P&L.

APY also depends on the measurement window. A short burst of volatility can make annualized returns look huge. A calmer week can make the same strategy look dull. The vault did not become a different species overnight. The market gave it a different weather forecast.

So read the source before reading the number. A smaller, repeatable source can be healthier than a large APY driven by one unusual event.

Market making vault returns are not guaranteed because the vault is exposed to changing markets. Trading volume, volatility, funding, fee rules, liquidity, and strategy quality all shape the final result.

The clearest risk is negative trading P&L. The dYdX MegaVault FAQ warns that automated vault positions can have negative trading P&L, and those losses can outweigh fee sharing or other sources of return.

That lesson applies beyond one named product. If a vault holds a long position and price falls, NAV can fall. If traders win against the vault, NAV can fall. If the vault quotes into a fast move, stale prices, or thin liquidity, NAV can fall.

> A stablecoin deposit can still become a lower-value vault share. The deposit asset may be stable. The strategy is not.

APY can move for less dramatic reasons too. More deposits can dilute the same revenue across more vault shares. Market makers can crowd into the same opportunity. Funding payments can change direction. Protocol incentives can shrink.

Annualized returns also deserve suspicion. A seven-day return multiplied into a yearly number is not a promise from the future. It is arithmetic wearing a blazer.

The useful check is simple. Ask what would make the vault lose money, then look for that condition in its history. If the answer is vague, the APY has not earned much trust.

Market making vaults differ from staking, lending, AMM pools, and copy trading because the return source and loss path are different. These products can all sit under “yield,” but that label hides too much.

This comparison keeps the risk source visible:

| Product Type | How The Risk And Return Actually Work |

|---|---|

| Staking | Rewards come from helping secure or support a network. Loss risk can include slashing, lockups, token price moves, and platform custody. |

| Lending | Returns come from borrower demand and interest. Loss risk can include bad collateral, liquidations, smart contracts, and market stress. |

| AMM pool | Fees come from swaps through a liquidity pool. Loss risk can include impermanent loss, pool imbalance, thin exits, and token price moves. |

| Market making vault | Returns come from liquidity provision, spread capture, fees, funding, incentives, or trading P&L. Loss risk includes bad inventory and traders winning against the vault. |

| Copy trading vault | Returns follow a trader or manager. Loss risk depends on that person’s strategy, discipline, fees, and risk controls. |

The market making vault row is the one users often under-read. Some vault returns can feel like market PVP because depositors may benefit when trader flow loses against the vault. That also means the vault can be the one taking the hit when traders win.

An AMM pool is not identical either. AMMs use pool reserves and pricing curves. Market making vaults often deal with order books, perp markets, inventory, funding, and automated position management.

So do not compare only the APY. Compare the job each product is doing. A staking position, lending deposit, AMM LP token, and market making vault can all pay yield, but different risks fund those yields.

The main risks of using a market making vault are strategy losses, trader-flow losses, manager risk, protocol risk, withdrawal friction, and infrastructure failure. “DeFi risk” is too vague to help.

Strategy risk shows up when the vault’s trading logic fails for the market it faces. The vault may quote too tight, hold bad inventory, rebalance too late, or depend on conditions that disappear.

A strategy can look strong during one market regime and weak in another. High volume can feed spread capture. Sharp one-way moves can punish inventory. Low volume can leave the vault earning little while still carrying operational risk.

Some market making vaults effectively sit across from trader flow. When traders lose, the vault may gain. When traders win hard, the vault may lose.

This does not mean every vault is hostile to users. It means the economics can be adversarial in spots. If a vault is the liquidity source, it can also be the balance sheet absorbing the other side.

User-managed vaults add manager risk. A manager may overtrade, chase short-term performance, hide weak periods behind selective charts, or take fees that leave depositors with less upside.

Look for manager stake, fee split, public history, drawdowns, strategy description, and controls. A hot leaderboard can be survivorship bias with a nice jacket.

Smart contracts, oracle inputs, governance parameters, and market listings can all affect vault outcomes. A bad price feed, thin new market, broken liquidation path, or rushed listing can hurt a strategy that depends on clean market data.

Bridge risk can also hit deposits or withdrawals that cross chains. A vault does not only depend on its trading logic. It depends on every layer funds must pass through.

Withdrawal risk appears when a user can technically exit, but the exit is delayed, costly, or available at a worse value. Cooldowns, queues, slippage, bridge congestion, and market stress can all change the final result.

That is where exit liquidity becomes more than a meme. A vault share is only useful if the exit route can return value when you need it.

The risk map is not a reason to panic. It is a reason to size the position like a trading strategy, not like spare cash.

Evaluate a market making vault by tracing the money, the strategy, and the exit before you sign. You should know what enters the vault, who or what controls it, how NAV is measured, and how withdrawals work.

Start with the official product page, live app terms, and strategy description. Then compare that with the vault’s actual history. A pretty APY screen is not a due diligence packet.

Use this checklist before any meaningful deposit:

| Check | Why It Matters |

|---|---|

| Deposit asset and network | Confirms what leaves your wallet and which chain or bridge path you use. |

| Vault share or NAV method | Shows how ownership, gains, losses, deposits, and withdrawals are priced. |

| Strategy description | Explains whether yield comes from spreads, funding, fees, incentives, or trader P&L. |

| Manager or automation | Separates protocol-run logic from user-managed strategy risk. |

| Drawdown history | Shows how the vault behaved when markets moved against it. |

| Fee split | Reveals how much upside stays with depositors after manager or protocol fees. |

| Lockup or cooldown | Tells you whether you can exit quickly or must wait. |

| Withdrawal route | Exposes slippage, queues, bridges, or unsupported asset paths. |

| Audit and permissions | Helps you understand contract, upgrade, and wallet-approval risk. |

| Return concentration | Shows whether performance came from one lucky event or a repeatable source. |

Do not let the table do all the work. The strongest check is whether you can explain the vault in two plain sentences: where the return comes from, and what would make the position lose money.

Wallet hygiene belongs here too. Before signing, confirm the official URL, network, token approval, spending limit, and revocation path. CryptoProcent’s crypto wallets section is useful background if approvals and custody still feel fuzzy.

Then test the exit. A tiny deposit and withdrawal can reveal fees, delays, UX friction, and balance tracking problems while the mistake is still small.

A market making vault can fit as a small, high-risk yield allocation for users who already understand DeFi, stablecoins, withdrawals, and trading P&L. It belongs in the “monitor carefully” bucket, not the emergency-funds bucket.

The fit starts with capital you can afford to keep busy or lose. A stablecoin deposit may make the position feel calmer than a token trade, but the vault can still move with trader flow, inventory, fees, and withdrawal rules. If those mechanics still feel foggy, study first or run a tiny test. Do not make it a meaningful allocation.

Good-fit cases have a few shared traits:

Bad-fit cases are easier to spot. Avoid market making vaults when the strategy is vague, the manager is unknown, the exit path is unclear, the vault depends on a bridge you would not use directly, or the money is needed soon.

Also check correlation before calling several deposits diversified. Three vaults tied to the same venue, collateral asset, manager style, or perp market can weaken together during the same stress event. Diversification should change the risk source, not just the dashboard tab.

The product can be legitimate without being suitable. That distinction saves people from two lazy conclusions: “all yield is a scam” and “all stablecoin APY is safe.” Both are too neat for crypto, which rarely wastes a chance to be messy.

These market making vault terms help decode vault pages without turning the page into a glossary dump. Focus on ownership, market structure, and loss language. If a vault page uses these words but never explains them, slow down before the APY starts doing stage magic.

HLP is Hyperliquid’s well-known liquidity vault example. dYdX MegaVault is another protocol example. Vault shares track a depositor’s claim on the pooled position. NAV is the vault’s net asset value, which can rise or fall with strategy results.

The bid-ask spread is the gap between buy and sell quotes. Funding rate is a perp-market payment that can help or hurt depending on direction. Liquidations can create fees or losses. Perpetual futures markets explain why funding, mark prices, and liquidation rules show up so often in vault risk.

Inventory risk is the danger of holding the wrong exposure after quoting markets. Drawdown means a drop from a prior high in vault value. Market maker means the strategy or actor placing liquidity.

Exit liquidity describes whether a position can be sold or withdrawn at a useful value, especially during stress. Wallet approvals and custody language describe who can move funds, what permissions you signed, and how cleanly you can revoke access if the product stops making sense.

Once those terms are clear, a market making vault page becomes less mysterious. You can read it as a route: deposit, share, strategy, P&L, fees, and exit. That route is what you are buying, not the prettiest number on the front page.

A market making vault in crypto is a pooled vault that uses depositor capital to provide trading liquidity and share the resulting profit or loss with depositors. It may quote bids and asks, manage inventory, earn fees, or take automated positions.

Yes, you can lose money in a market making vault. Losses can come from negative trading P&L, bad inventory, trader wins, liquidations, oracle issues, smart-contract problems, bridge failures, stablecoin risk, or poor withdrawal conditions.

No, a market making vault is not the same as staking. Staking supports a network or validator process, while a market making vault uses pooled capital for liquidity or trading strategies.

Market making vault APY can change because trading volume, volatility, funding rates, fee rules, incentives, strategy performance, and vault size all change. Short measurement windows can also make returns look stronger than they really are.

Some market making vaults may allow quick withdrawals, but others use cooldowns, queues, withdrawal windows, or slippage controls. Check the live app terms before depositing because exit rules can vary by protocol.

A market making vault can be run by protocol automation, a designated operator, or a user-managed strategy leader. The operator controls strategy settings, fees, permissions, and risk limits, so depositor outcomes can change with that role.

Start with the loss path, not the APY. If you cannot explain how a market making vault loses money, you are not ready to size it.

The first review should be boring on purpose. Read the strategy, then say it back without protocol slogans. A market making vault should have a clear return source, a clear accounting method, and a clear exit path. If those pieces only appear after five clicks and a Discord search, that friction is part of the risk.

Use this sequence before depositing:

The tiny test is not a ritual. It checks whether the app, wallet, network, fees, and withdrawal route behave the way the documentation suggests. It also gives you a chance to spot surprise cooldowns, unclear balances, or confusing share pricing before the number is large enough to ruin your week.

Keep the first position small enough that a bad lesson stays educational. A market making vault can be useful when the mechanics are clear and the risk is sized honestly.

After that, keep reviewing the position when conditions change. A vault that looked sensible during steady volume can look different after a funding flip, liquidation event, manager change, bridge issue, or quiet market. If the only clear detail is a large APY, let someone else beta-test the spreadsheet.