Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A plain-English guide to locked float, FDV, token unlocks, and liquidity risk.

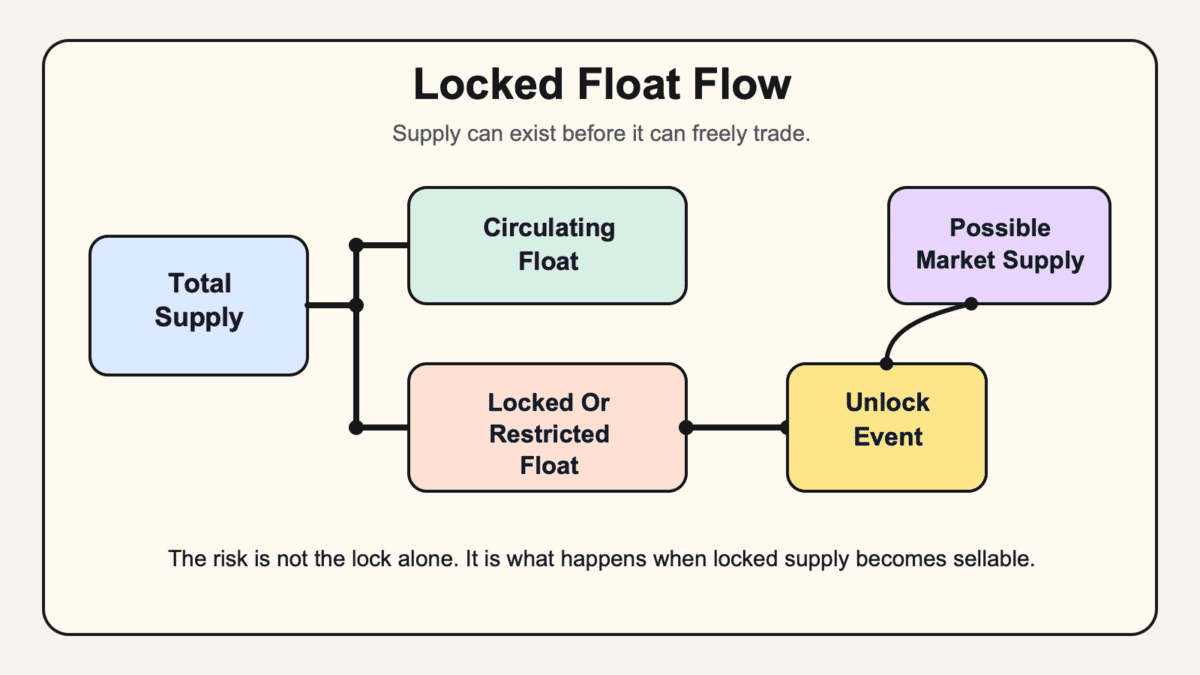

Locked float is the part of a crypto token’s supply that exists but cannot freely trade in the market right now.

The term is practical market language, not a single metric every data site labels the same way. You may see nearby terms such as locked supply, token lockups, restricted supply, free float, circulating supply, low float, and token unlocks.

That vocabulary gap can get expensive. A token may look small by market cap while a much larger supply waits behind vesting schedules, team allocations, treasury wallets, staking restrictions, or private-sale lockups.

Locked float in crypto means token supply that exists but sits outside the freely tradeable market. It may be locked by a smart contract, vesting schedule, legal sale agreement, staking rule, treasury policy, bridge reserve, or internal allocation.

The closest standard market-data idea is circulating supply. CoinMarketCap’s supply methodology treats circulating supply as a public-float-style measure. It generally excludes assets that are locked, insider-held, or not sellable in public markets.

Its token-release-schedule data covered only about 0.00462% of coins, roughly 600 of 13 million. That is a useful reminder: unlock data is still patchy.

Use this table to separate the supply labels before you read a tokenomics chart:

| Term | What It Means For Locked Float |

|---|---|

| Locked float | Existing tokens that cannot freely trade right now. |

| Circulating supply | Tokens counted as public market supply. |

| Total supply | Tokens that exist now, usually after burns. |

| Max supply | The most tokens that can exist under the token design. |

| FDV | Current price multiplied by total or max supply. |

| Locked liquidity | LP assets are locked, not necessarily token supply. |

That turns locked float into a risk lens. It asks how much supply can meet buyers today, and how much may arrive later.

That split also explains why two dashboards can disagree. One may count more supply as circulating, while another may wait for wallet proof, vesting data, or trading venue evidence.

Read locked float as a set of questions, not one magic number. Who controls the supply, when can it move, and can the market absorb it?

Locked float changes market cap and FDV because those metrics count different supply views. Market cap usually focuses on circulating supply, while FDV estimates the valuation if the full token supply were priced at today’s market price.

That gap can make a token look cheap and expensive at the same time. A token with a modest market cap may carry a much larger FDV if most supply is locked, vested, reserved, or not yet counted as public float.

Use a simple illustrative example:

Nothing in that example predicts the next candle. It only shows the valuation gap. The market price is being set by a small tradable slice, while future supply still needs real demand and depth.

The gap only becomes useful when you connect it to timing. The same market cap can carry very different risk if the missing supply belongs to early investors, a team allocation, a treasury wallet, or rewards that unlock soon.

That is where late-buyer risk enters. If early holders, private investors, or treasury wallets later sell into public demand, new buyers can become exit liquidity for supply that was not visible in the current float.

Start with the gap. Compare FDV with the current float, then ask when the missing supply can move, who receives it, and whether buyers have enough reason to absorb it.

Locked float can help a token pump hard because fewer freely tradeable tokens can make demand hit a thin market. If a listing, a meme, a strong catalyst, or a public narrative arrives fast, price can move before deeper supply appears.

That scarcity can be real for a while. Thin order books, shallow DEX pools, and CEX listing attention can all push a low-float token higher than a deeper market would allow.

On a thin book, a few aggressive buys can walk through weak sell orders. On a small DEX pool, the same demand can move the pool price sharply because there is not much inventory to absorb it.

But the same setup can turn quickly. Future unlocks, weak liquidity, concentrated holders, and low-cost insider allocations can add supply after the easy upside is gone.

Watch for these pressure points:

> A low float can make price action look cleaner than the token structure underneath it.

The trap is timing. A user who buys after the pump may hold through the part where new supply reaches the market and demand thins.

That is how a late buyer can become a bagholder even when the original setup was not a clear scam. The trade can simply move from scarcity to supply overhang.

That is why locked float should sit beside liquidity checks. Scarcity can explain the first move, but depth decides whether later selling lands softly or turns into a long red staircase.

Token unlocks change locked float by moving tokens from a restricted bucket into a bucket that may become transferable, sellable, stakeable, claimable, or usable by the recipient. The price effect depends on what unlocks, who receives it, and how deep the market is.

A cliff unlock releases a set amount at once. Linear vesting releases supply gradually. Staking emissions, airdrop claims, treasury releases, and market-maker inventory can also change available supply.

Recipient type shapes the story. A team allocation may have different incentives from a community reward, a private investor allocation, a foundation treasury release, or market-maker inventory used for liquidity operations.

Before reacting to an unlock headline, check the event in order:

An unlock does not force an immediate dump. Recipients may hold, hedge, stake, use tokens operationally, or sell slowly.

Still, the market has to price the possibility of new supply. A known, small, slow release can be absorbed. A large cliff into weak demand is much harder for the market to digest.

Locked float and locked liquidity describe different risks. Locked float is about token supply availability. Locked liquidity is about liquidity pool assets or LP tokens being locked so the liquidity provider cannot withdraw them easily until the lock ends.

That difference is not cosmetic. People can often still trade against a pool while liquidity is locked. The lock may reduce one type of LP-pull risk, but it does not prove the token supply is fair, the holders are distributed, or future unlocks are harmless.

Use this table before treating a lock badge as a safety stamp:

| Signal | What It Does And Does Not Prove |

|---|---|

| Locked float | Shows some supply cannot trade now, but may unlock later. |

| Vesting lock | Delays recipient access, but does not remove sell pressure forever. |

| Staking lock | Restricts movement while staked, but rules can vary by protocol. |

| Locked liquidity | Limits LP withdrawal, but trading can still happen. |

| Burned liquidity | Can reduce LP-pull risk, but contract and holder risks remain. |

| Concentrated holders | Shows control risk even if liquidity looks locked. |

The mistake is reading locked liquidity as proof that a token cannot be dumped. It is only one market-structure signal.

If a project can remove liquidity suddenly, that belongs closer to hard rug risk. If liquidity is locked but insiders hold a large future allocation, the risk is more about supply pressure and holder concentration.

So check both. Supply locks and liquidity locks answer different questions, and neither replaces wallet, contract, volume, or unlock checks.

You check locked float before buying by comparing what can trade now with what can become tradeable later. The goal is to avoid a tiny public float while a much larger supply sits nearby.

Start with the tokenomics page, then verify what you can with independent market data and on-chain tools. Labels vary, so compare several supply views instead of trusting one dashboard number.

Use this workflow before entering a low-float token:

For meme-token environments, the workflow gets faster and rougher. People often check LP locks, deployer wallets, holder concentration, taxes, mint controls, and liquidity depth before entering the trenches.

That speed does not make the checks optional. It just means the market punishes lazy reading faster.

Also separate “available to transfer” from “likely to sell.” A treasury release can fund operations. A private investor release may create profit-taking risk. Airdrop claims can create scattered small sellers.

Signals work best as a cluster, not as one datapoint. A tiny float plus high FDV, vague vesting, concentrated wallets, and shallow liquidity deserves more caution than any single item alone.

Locked float is neither good nor bad by itself. It is a structure that can support orderly distribution, create early scarcity, or hide future sell pressure depending on the design.

Some projects lock supply so teams, investors, treasuries, or reward programs cannot sell everything at launch. That can reduce instant dumping and align longer-term incentives when the rules are clear.

The problem appears when the public market prices a small float as if the rest of the supply will never arrive. That is the low-float, high-FDV anxiety traders complain about.

A cleaner setup usually explains the restriction before anyone has to hunt for it. The supply schedule is public, recipient buckets are named, and future releases are easy to compare with volume.

A weaker setup asks the market to trust vague scarcity. It may talk about locked supply while avoiding the harder details: who owns the locked tokens, when they unlock, and whether early holders already sit on large paper gains.

Use a few practical signals:

A low locked float token is not automatically a scam. A fully circulating token is not automatically clean.

Ask four plain questions instead: where is the rest of the supply, when can it move, who controls it, and how could the market absorb it?

Start with locked float by building one small checklist before you buy or hold a low-float token. Keep it short enough that you will actually use it when the chart is yelling.

Do these checks before you size a position:

Then write one sentence that would make you change your plan. It could be a cliff unlock, a wallet movement, a liquidity drop, a contract change, or a failed demand catalyst.

Keep that sentence visible before you buy. It turns a vague worry into a rule you can check later, which is useful when a group chat starts chanting that supply details are “already priced in.”

That sentence helps because locked-float risk usually shows up as a sequence. First the token looks scarce. Then supply becomes available. Then the market reveals whether demand was real or just a crowded line waiting for the same exit door.

If you cannot find the supply schedule, do not fill the blank with hope. Mark the unknown, reduce size, or skip the trade. There will be another shiny chart. Crypto has never suffered from a shortage of those.

For an existing position, repeat the same check before large unlock dates. You do not need to predict every seller. You only need to know whether your reason for holding still survives the next supply change.

Locked float in crypto is token supply that exists but cannot freely trade right now. It may sit in vesting contracts, team allocations, private-sale lockups, treasury wallets, staking restrictions, or other restricted buckets.

The key check is whether that supply can become sellable later. If it can, compare the release schedule with FDV, current float, volume, and liquidity.

Locked float and locked supply are closely related, but they are not always used the same way. Locked supply usually means tokens that are restricted or unavailable for transfer. Locked float focuses on how much supply is outside the freely tradeable market.

For most trader checks, ask the same thing: which tokens cannot trade now, and when could they enter the market?

Locked float is not the same as locked liquidity. Locked float is about token supply. Locked liquidity is about LP assets or LP tokens being restricted so liquidity cannot be pulled easily.

A liquidity lock can reduce one risk, but it does not prove clean tokenomics. You still need to check holder concentration, supply locks, contract controls, and future unlocks.

Locked float describes supply availability, while FDV describes valuation. Locked float asks which tokens can trade now. FDV estimates what the project would be worth if all relevant supply were counted at the current price.

The two work best together. A small float and large FDV gap can warn that the current market price is being set by a thin slice of supply.

A locked float token unlock does not always reduce price. The effect depends on unlock size, recipient behavior, market depth, demand, and whether traders already expected the event.

A small linear release into strong demand may pass quietly. A large cliff unlock into weak liquidity can create heavier sell-pressure risk.

A low locked float crypto token is not automatically a scam. It can be a normal launch structure, especially when vesting, recipients, and supply schedules are clear.

It becomes riskier when low float pairs with high FDV, vague lockups, concentrated wallets, weak liquidity, aggressive promotion, or missing unlock data.