Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Understand looping before debt compounds.

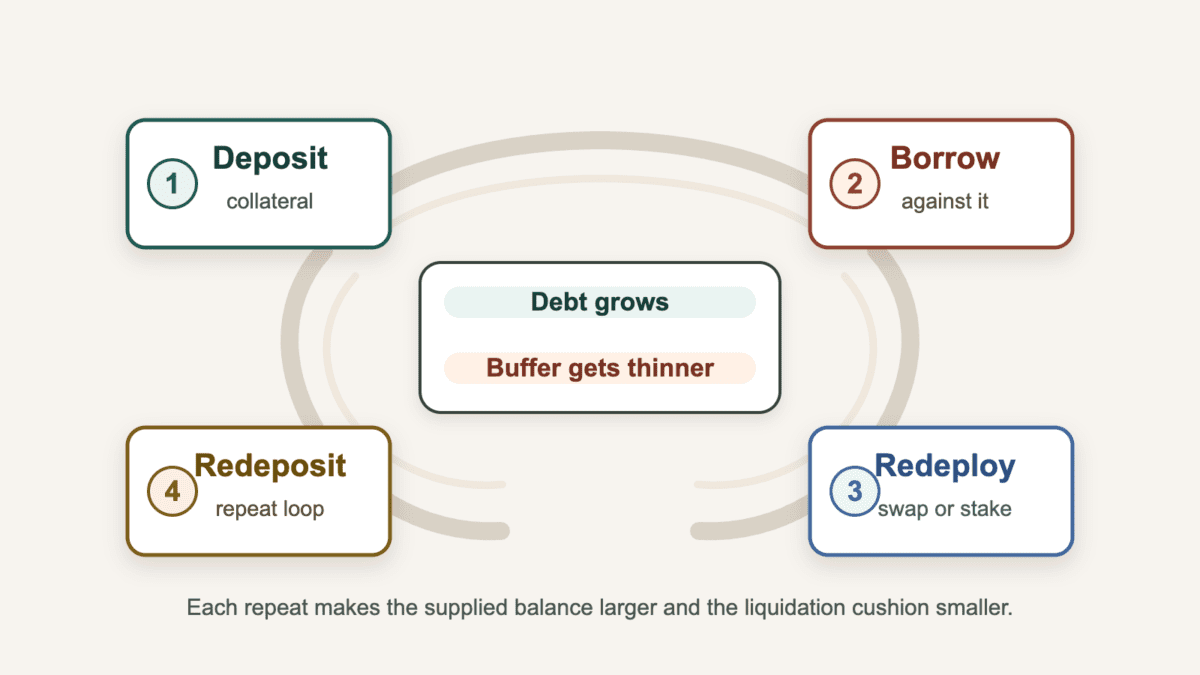

Looping in crypto is a DeFi borrowing strategy where you deposit collateral, borrow against it, redeploy the borrowed asset, and repeat.

The word sounds harmless because it describes a cycle. The risk comes from what the cycle creates: more collateral on the screen, more debt underneath it, and less room for the position to be wrong. Looping shows up around Aave, Morpho, Euler, Pendle, stablecoin yield, liquid staking tokens, restaking wrappers, and points farming. The useful question is not “how high is the APY?” It is “what do I owe, what backs it, and how do I get out?”

Looping in crypto means using a lending market recursively: deposit collateral, borrow against it, turn the borrowed asset into more collateral or exposure, then repeat.

In finance, the cleaner term is recursive lending or recursive borrowing. In DeFi, the loop usually runs through money markets such as Aave, Morpho, Euler, Compound, or similar lending venues.

> The key distinction is debt. Looping reuses borrowed value, so the position becomes larger and less forgiving.

A basic loop starts with one asset. A user supplies collateral, borrows another asset, swaps or redeploys that borrowed asset, and supplies the result again. That new supply supports another borrow, so the cycle can continue until the user stops or the protocol’s limits kick in.

That makes looping different from plain staking, liquid staking, restaking, or Loopring. Staking earns rewards from holding or delegating an asset. Loopring is a separate crypto project and ticker family. A looping strategy is a DeFi lending position with collateral, debt, and a liquidation line.

The important word is position. Looping is not only an action taken once at entry. It leaves an account with an ongoing debt balance, live collateral rules, and a changing buffer. Rates can move after the trade starts. So can collateral prices, peg relationships, and liquidity.

That is why screenshots can mislead. A dashboard may show a bigger supplied balance, a tidy yield estimate, and a calm health factor. Under that, each round has added a new dependency: collateral price, borrow rate, oracle pricing, liquidity, and the user’s ability to unwind before the market gets rude.

A basic looping strategy works by recycling borrowed value back into the position. The account grows on both sides: supplied assets rise, borrowed assets rise, and the safety buffer usually shrinks.

A neutral example shows the mechanics. A user deposits collateral into a DeFi lending market. They borrow against that collateral, then swap or redeploy the borrowed asset. They deposit the new asset again, which lets them borrow again.

The loop has a simple order:

The dashboard usually changes after each round. Collateral value rises because more assets are supplied. Debt rises because more assets are borrowed. Health factor, loan-to-value, or the equivalent risk score moves closer to the liquidation zone.

That is the catch. The position may look more productive, but it is less forgiving.

An automated looping strategy can bundle several steps into one transaction. Tools such as Contango, DeFi Saver, Instadapp, and similar products may automate entry, rebalancing, or flash-loan-assisted loops. Fewer clicks can reduce manual mistakes, but the account still has collateral, debt, borrow costs, and liquidation rules.

Unwinding reverses the same path. The user usually needs to repay debt, withdraw collateral, swap back, and repeat until the loop is closed. If liquidity is thin or gas is high, the exit can be worse than the tidy entry preview.

Traders use looping because it can turn one asset base into larger exposure, a yield-spread trade, a rewards setup, or a way to borrow without selling. Those are different motives, not one universal trade.

The reason for opening the loop decides what can break first. A directional loop cares most about price. A yield loop cares about net spread. A points loop cares about rewards that may arrive late, arrive small, or never arrive.

Common motives include:

Looping can overlap with farming in crypto when rewards or points drive the trade. But farming incentives do not erase debt. Points do not repay a loan, and a future airdrop is not collateral.

That distinction keeps the risk clear. If a loop is really a long ETH position, call it that. If it is a stablecoin carry trade, check the rates. If it is a points farm, accept that the reward side may be uncertain while the borrow side is painfully real.

This is where many users get trapped by a screenshot. A high APY can blend staking yield, lending yield, token emissions, temporary incentives, and points into one number. The position may be profitable only while every assumption stays friendly.

Ask the motive before asking the loop count. “Why am I borrowing?” is the first risk check.

Looping yield comes from what the position earns after debt, execution, and exit costs. The headline APY is only useful after the source of that yield is clear.

Some loops earn from ordinary lending demand. Others use staking yield, liquid staking tokens, incentive campaigns, points, fixed-yield tokens, basis-style carry, or vault distributions. Each source fails in a different way.

Use the yield source as the filter:

| Yield Source | What To Verify |

|---|---|

| Lending spread | Borrow APR, supply APY, utilization, and fees. |

| Staking or LST yield | Validator yield, token liquidity, peg quality, and borrow cost. |

| Incentives or points | Reward rules, vesting, token value, and campaign durability. |

| Fixed-yield or PT carry | Maturity date, market depth, pricing, and debt timing. |

| Vault or strategy yield | Underlying assets, fees, contracts, and unwind path. |

The source also tells you how often to recheck the loop. Lending rates can move hourly. Incentive rules can change with a campaign. Fixed-yield trades have maturity dates, while vault returns depend on the strategy underneath.

The highest number is not automatically the best loop. A smaller yield with clear debt, deep liquidity, and a wide buffer can be less dangerous than a glossy APY built on points, thin markets, and one very optimistic spreadsheet.

Borrowing cost is the quiet tax. If the borrow APR rises, a positive loop can turn into negative carry. If rewards drop, the same thing happens. If the user has to swap several times to exit, slippage and gas can eat the spread.

So yield size comes second. Yield source comes first.

DeFi looping has several common forms, and each one moves the weak point to a different place. The names can sound similar, but the risk is not the same.

ETH and liquid staking loops are often built around ETH, WETH, stETH, wstETH, weETH, rETH, rsETH, or other ETH-linked wrappers. Stablecoin loops use assets such as USDC, USDT, DAI, USDe, sUSDe, or yield-bearing dollar wrappers. Fixed-yield loops may use Pendle principal tokens or similar markets.

The main variants are easier to compare by failure point:

| Loop Type | Main Thing That Can Break |

|---|---|

| ETH or LST loop | Peg stress, borrow-rate spike, oracle stress, or liquidation. |

| Stablecoin loop | Depeg, rate inversion, issuer risk, or poor exit liquidity. |

| Cross-asset loop | Collateral drop, debt asset move, slippage, or correlation break. |

| Points loop | Rewards disappoint while debt and liquidation risk remain. |

| Automated loop | Wrapper risk, hidden assumptions, or hard-to-read unwind mechanics. |

Aave looping is the most visible example because Aave has deep lending markets and e-mode settings for correlated assets. Morpho and Euler also appear in stablecoin and yield discussions. Pendle appears where users loop fixed-yield or principal tokens. Contango, DeFi Saver, and Instadapp often show up around automation.

Those names are examples, not recommendations. A platform list ages quickly. The useful comparison is always the same: what is collateral, what is debt, what prices both, and what happens if the relationship breaks?

Some loops are directional trades wearing a yield hat. Others are carry trades with liquidation risk. A points loop can be the strangest version: the user takes real debt today for a reward that may be worth less than the gas used to farm it. Crypto does enjoy making patience expensive.

Stablecoin looping can reduce price volatility, but it does not remove liquidation risk. It shifts risk toward pegs, rates, issuers, liquidity, redemption, and protocol assumptions.

The beginner mistake is thinking “stable” means “safe.” A stablecoin can drift, depeg, pause redemptions, face issuer pressure, lose liquidity, or become expensive to borrow during stress. A yield-bearing dollar token adds another layer because the wrapper can carry its own rules and market depth.

> Stablecoin loops can still liquidate. Lower volatility is not a magic shield when the position is borrowed, crowded, and close to its limit.

Picture a simple stablecoin loop. A user supplies one dollar asset, borrows another, swaps, redeposits, and repeats. The dashboard may look calm because both assets are supposed to trade near one dollar. But a small depeg, a borrow-rate spike, or weak liquidity can move the account toward liquidation.

Rate inversion is especially dull and dangerous. The loop may work while supply yield plus rewards beat borrow cost. Then utilization changes, rewards fall, or the borrowed stablecoin gets scarce. The net yield flips negative while the position still looks price-stable.

Exits can also get crowded. If many users run the same stablecoin loop, they may all need to repay, swap, and withdraw at the same time. That can widen spreads and make the unwind more expensive exactly when the buffer is already thin.

Stablecoin looping is not automatically bad. It is just not free yield. The user has to check peg quality, issuer exposure, oracle assumptions, liquidity depth, borrow-rate history, and the exact repayment path.

Looping risks start with liquidation, but they do not end there. The full risk map includes rates, collateral quality, oracle pricing, protocol settings, contracts, gas, taxes, and exit conditions.

Liquidation is the cleanest failure path. If collateral no longer covers debt with enough buffer, liquidators can repay part of the debt and seize collateral under the protocol’s rules. The user may lose assets even if the broader idea still sounds reasonable.

The main risk buckets are worth checking before any APY:

Correlated-collateral loops need special caution. In a May 2026 Aave V3 Core snapshot, Galaxy Research found e-mode loans had a debt-weighted health factor near 1.05. That is a thin margin when many positions rely on ETH-linked collateral, WETH-heavy debt, and assets staying closely correlated.

Crowded exits add a market-structure problem. If everyone rushes to unwind the same loop, slippage can worsen and late exits can become exit liquidity for faster users. The exit route matters as much as the entry route.

Protocol failure belongs on the same checklist. A loop that stacks new vaults, bridges, wrappers, and unaudited markets can turn one weak component into a bigger loss. In extreme cases, a malicious or failed protocol can behave like a hard rug, and borrowed exposure makes the damage travel faster.

The boring risks are often the expensive ones. Gas spikes can block a small unwind. Slippage can turn a profitable loop into a loss. A parameter vote can lower borrowing power. An alert that never fires can make a monitored strategy into a sleeping liquidation.

Looping differs from staking, farming, and margin trading because it creates exposure through repeated lending-market debt. Similar-looking yield does not mean similar mechanics.

Staking starts with an asset and earns rewards for network participation or protocol design. Yield farming may involve supplying assets to earn fees, rewards, or incentives. Margin trading uses a trading venue or derivatives product to create direct borrowed exposure. Looping uses collateral deposits and borrowing rounds.

The debt leg is the key difference:

| Compared With | What Changes |

|---|---|

| Staking | Staking earns rewards without automatically adding borrow debt. |

| Liquid staking | The token stays usable, but looping adds lending-market debt. |

| Yield farming | Rewards may overlap, but looping reuses borrowed collateral. |

| Simple lending | One deposit earns yield without recursive borrowing. |

| Margin or perps | Leverage comes from a trading venue, not repeated collateral loans. |

Restaking and liquid restaking can sit inside a loop, but they are not loops by themselves. A user might deposit an LRT, borrow ETH or a stablecoin, buy more exposure, and redeposit. The restaking wrapper is the asset. The loop is the borrowing cycle around it.

Margin and perps can be more direct. The trader usually sees position size, liquidation price, funding, and margin in one interface. A DeFi loop can feel softer because it lives inside a lending dashboard. The softness is cosmetic. Debt is still debt, even when the button says supply.

Farming sits somewhere in the middle. A loop can farm rewards, but the rewards are only one side of the trade. If the rewards end, vest slowly, or trade poorly, the debt remains.

Evaluate a looping strategy by tracing the debt path before the yield path. If you cannot explain the downside without mentioning APY, the setup is not ready.

Start with the dashboard terms. Find the collateral asset, borrowed asset, LTV, liquidation threshold, health factor, borrow APR, supply APY, rewards dependency, oracle source, and liquidation penalty. Then check how those values change after the final loop, not just the first deposit.

Use this checklist before signing anything:

Wallet and approval hygiene are part of the position. A good wallet setup cannot stop a valid liquidation, but it can reduce signing mistakes, approval sprawl, and wallet-level damage if a protocol or front end is compromised.

The unwind test should come before the entry. Write the exit path in order: repay debt, withdraw collateral, swap if needed, repay again, and repeat until closed. If the loop depends on one button that you cannot reproduce manually, size it like a tool can fail.

Finally, compare the loop to the boring alternative. If simple lending, plain staking, or holding cash-like assets gives most of the return without recursive debt, the extra yield has to earn its keep. Often, it does not.

Looping is probably a bad idea when you cannot monitor the position, explain liquidation, or close the loop under stress. It is also a poor fit when the main attraction is a screenshot APY.

Beginners should be cautious because loops punish vague understanding. Collateral, debt, liquidation threshold, health factor, oracle pricing, and borrow APR are not decoration. They decide whether the account survives a bad day.

The red flags are blunt:

Going full port into a loop is especially fragile. The same market move can hit collateral value, debt cost, liquidity, and emotional control at once. That is not conviction. That is a liquidation test with branding.

Looping can make sense for advanced users who understand lending markets, accept the debt, and have a written exit. It does not make sense as a shortcut into high yield. If the loop only works when rates stay friendly, pegs stay perfect, gas stays cheap, and rewards stay generous, the trade is already asking for too much politeness.

Related looping concepts help decode the dashboard before the position gets dangerous. They are not trivia. They are the vocabulary that shows where the risk is hiding.

Start with the lending terms. Recursive lending means borrowing against collateral, redeploying the borrowed asset, and repeating the process. Health factor is the risk score that shows how close the account is to liquidation. Liquidation threshold is the point where collateral no longer supports debt under protocol rules.

Then check the asset labels. E-mode can allow higher borrowing limits for correlated assets, but it also relies on that correlation holding. LSTs, LRTs, PTs, oracles, and flash loans each add their own assumptions. A high health factor gives more room. A weak oracle can misprice collateral. A thin PT market can make the exit expensive.

For next steps, two related concepts matter most:

The terms also stop false comparisons. Looping is not automatically staking because an LST is involved. It is not automatically safe because e-mode exists. It is not automatically simple because a flash loan makes entry fast.

When a strategy uses too many terms you cannot define, that is a signal. The right next move may be more reading, a smaller size, or no loop at all.

No. Looping is a DeFi borrowing strategy, while Loopring is a separate crypto project and token family. The similar spelling creates confusion, but the concepts are unrelated.

Here, looping means recursive lending: deposit collateral, borrow, redeploy, redeposit, and repeat.

No. Crypto looping can use staking tokens, but the loop itself is the borrowing cycle. Staking earns rewards from an asset or validator setup without automatically adding a debt leg.

If you deposit wstETH, borrow ETH, buy more wstETH, and repeat, the staking token is only one part. The loop is the debt structure around it.

Yes. Stablecoin looping can be liquidated if peg, rate, liquidity, oracle, or collateral assumptions break. Lower volatility does not remove debt risk.

A small depeg or borrow-rate spike can matter more after several loops because the position has less room than a simple one-deposit loan.

Users loop when the expected return beats the borrow cost after fees, gas, and slippage. That return may come from staking yield, incentives, points, lending spread, or basis-style carry.

The risk is that the spread changes. Borrowing costs can rise, rewards can fall, and points may not become valuable tokens.

No. More looping can increase exposure, but it also increases debt and tightens the liquidation buffer. Past a point, the extra round may add more fragility than return.

Check net return after borrowing costs, fees, slippage, and exit risk. More loops can simply make a bad assumption fail faster.

Usually no. Looping is better suited to users who already understand collateral, debt, liquidation, oracles, rates, wallet approvals, and manual unwinds.

A beginner who wants yield should first understand plain lending, staking, and wallet safety. Recursive debt can wait. It is not going anywhere, unfortunately.

Start with looping by learning the risk terms before looking at platforms. A loop is only worth evaluating once the debt asset, collateral asset, health factor, yield source, and unwind route are all clear.

The first action is not opening a position. It is writing the loop in plain English. If the explanation begins with APY and skips the debt, the strategy needs more work.

Use these next actions:

Do this before comparing platforms. Venue choice matters, but it comes after the structure is clear. Aave, Morpho, Euler, Pendle, and automated tools can all show different interfaces for the same basic question: what collateral backs what debt?

Also decide what would make you leave. A loop needs a stop condition, not just an entry plan. That can be a minimum health factor, a maximum borrow APR, a peg move, an oracle concern, a rewards change, or a simple rule that says the position is too large.

Then compare the loop against simpler options. Plain lending, staking, or holding the asset may offer less yield, but they also remove several failure paths. That comparison keeps the yield honest.

The best loop is not the one with the loudest APY. It is the one where you know exactly what can break, how fast it can break, and what you will do before the dashboard starts blinking red.