Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

MEV burn explained without the roadmap fog.

MEV burn is a proposed Ethereum mechanism that would redirect part of MEV bid value into ETH burn instead of paying the full amount to validators or proposers.

The name gets confusing because it sounds like a live ETH burn switch. It is not. MEV burn belongs to Ethereum’s research and roadmap debate around block building, validator rewards, and who should capture value from transaction ordering. Users usually meet the topic through ETH scarcity claims, staking reward debates, and sandwich-attack frustration. Those problems are connected, but they are not one clean button.

MEV burn is a proposal to burn part of the value created when block builders compete over profitable transaction ordering. MEV means maximal extractable value: extra value that can come from including, excluding, or reordering transactions inside a block.

That value can appear in a DEX arbitrage, a liquidation race, or a sandwich around a large swap. In wallet-level language, MEV often means “someone found a way to profit from the order your transaction landed in.” Charming, in the way a parking ticket is charming.

Break it into three plain pieces before the jargon starts:

So MEV burn does not mean burning a random token, closing a position, or deleting a trading profit after the fact. It means a protocol design where some MEV-derived bid value would be routed into ETH burn.

Status is the guardrail. MEV burn should be described as proposed Ethereum behavior, not as another name for today’s fee burn. Ethereum already burns certain base fees under its current fee market. MEV burn would target a different pool of value: block ordering revenue that can otherwise show up as a validator or proposer windfall. If a builder is willing to pay for the right to have a block proposed, the design tries to split that payment between a burned portion and a proposer reward.

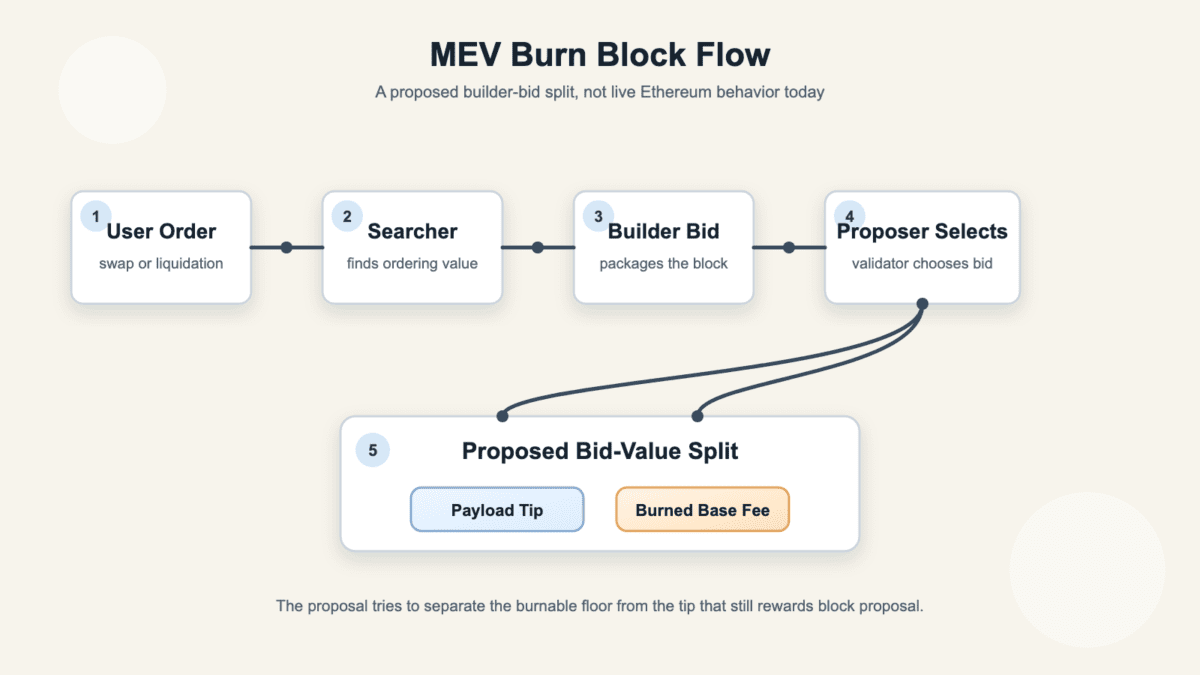

MEV burn fits into Ethereum’s block-production chain where builders bid for a block to be proposed. Before the burn makes sense, the actors need names.

Ethereum users submit transactions. Searchers look for profitable ordering opportunities. Builders assemble candidate blocks, often using searcher bundles or private order flow. A proposer is the selected validator for that slot. Relays currently connect builders and proposers in MEV-Boost style markets. Attesters help the network confirm what was proposed. The basic chain looks like this:

| Actor Or Step | Plain-English Role |

|---|---|

| User transaction | The swap, transfer, liquidation, or app action entering the ordering game. |

| Searcher | Finds profitable ordering opportunities, such as arbitrage or liquidations. |

| Builder | Packages transactions into a block and bids to have it selected. |

| Relay | Helps deliver builder blocks to proposers in today’s out-of-protocol setup. |

| Proposer or validator | Chooses the winning block for the slot. |

| Attesters | Help confirm that the block follows network rules. |

In a simple MEV burn design, the full builder bid does not become proposer income. Part of it can be treated like a payload base fee and burned. The rest can remain as a payload tip for the proposer.

The hard part is not drawing the boxes. It is making the protocol observe and enforce the split without creating easy workarounds. If builders and proposers can hide value, delay bids, or route payments around the burn, the clean chart becomes more wish than mechanism.

MEV burn differs from EIP-1559 burn because it targets ordering-value bids, while EIP-1559 burns part of normal transaction fee pricing. Both involve ETH burn. They do not burn the same thing.

EIP-1559 changed Ethereum’s fee market by introducing a base fee that moves with demand and is burned. Users still can pay priority fees when they want faster inclusion. MEV burn would live in the block-production auction layer, where builders compete to have blocks accepted by proposers.

Keep the buckets separate:

| Burn Mechanic | What It Burns |

|---|---|

| EIP-1559 Burn | The transaction base fee from Ethereum’s live fee market. |

| MEV Burn | A proposed part of MEV-related builder bid value. |

| Priority Fee | A tip to encourage inclusion, not the main burn target. |

| Payload Tip | The proposed proposer reward left after a MEV burn split. |

| Payload Base Fee | The proposed floor-like MEV amount that could be burned. |

This distinction prevents a common mistake. A user might see “burn” and assume MEV burn already works like the fee burn on Ethereum dashboards. It does not. EIP-1559 is live fee-market behavior. MEV burn is a proposed way to redirect a different revenue stream.

The investor read changes too. EIP-1559 burn rises or falls with transaction fee dynamics. MEV burn would depend on builder competition, extractable ordering value, protocol design, and whether the final mechanism can actually capture that value.

Ethereum researchers want MEV burn because MEV can create lumpy validator rewards, centralizing pressure, and messy incentives around block ordering. Burning part of MEV bid value could make that value accrue more broadly to ETH holders instead of one lucky proposer.

The idea is not only “burn more ETH.” That is the headline version, and headlines are where nuance goes to lose a shoe. The stronger case is about where ordering value goes, how validator rewards behave, and whether specialized MEV markets push small operators toward larger pools.

Three motivations usually drive the proposal:

Each point has a caveat. Reward smoothing does not mean validators earn nothing from block proposal. Value capture does not mean ETH price must rise. Cleaner incentives do not remove every MEV strategy from every app.

Solo stakers are part of the appeal. If MEV rewards depend heavily on specialized infrastructure, smaller validators may feel pushed toward operators that can optimize the whole MEV stack. A design that reduces extreme windfalls can make staking rewards less dependent on who gets lucky in a valuable slot.

That is why the proposal keeps resurfacing. It tries to turn a private ordering race into a more protocol-level value path. Whether it can do that cleanly is still the live debate.

MEV burn is not live on Ethereum as a normal feature users can rely on today. The current answer is that MEV burn is a research and roadmap idea tied to PBS, ePBS, and related block-production designs. The ethereum.org PBS roadmap describes proposer-builder separation as advanced research with important design questions still unresolved, and notes that there is no finalized specification yet.

This is also why “abandoned” is too blunt. MEV burn is not a finished upgrade waiting quietly behind a button. It is one design inside a wider debate about PBS, ePBS, execution tickets, inclusion lists, auction design, censorship resistance, validator incentives, and private order flow.

That middle status is easy to miss. If a wallet, dashboard, or social post talks as if MEV burn is already reducing ETH supply in every block, it is skipping the dependency chain. The burn idea needs a protocol structure where builder bids, proposer rewards, and any payload base fee can be defined and enforced cleanly.

So the practical answer has four parts:

Roadmap debates move slowly because the stakes are not small. Ethereum needs block production to stay efficient, censorship-resistant, and verifiable. A simple burn story is attractive, but the final design must survive builders, validators, searchers, and users who all have real money on the table.

That leaves users with a boring but useful rule: talk about MEV burn as a possible roadmap mechanism, not a current Ethereum setting. If the mechanism moves forward, the details to watch will be the final split, the enforcement model, and how much value can avoid the burn through private arrangements.

MEV burn could matter for ETH investors because it may redirect some block-ordering value toward all ETH holders through burn. That is the scarcity story. It is useful, but easy to overcook.

Crypto Twitter can turn any burn mechanic into instant “ultrasound money” shorthand. That shorthand belongs in the same drawer as Crypto Twitter shorthand: useful for reading sentiment, flimsy as a full model. For ETH holders, the possible impact has three lanes:

But none of that gives a launch date, daily burn number, or price target. The final formula, timing, and actual value captured are not settled. MEV volume also changes with market structure, app design, liquidity, volatility, and private routing.

The validator effect needs care too. Burning MEV can reduce certain proposer payments, but it may also make rewards less uneven. For a solo staker, lower variance can help if it narrows the gap between occasional windfalls and ordinary slots.

> MEV burn is not a guaranteed ETH scarcity machine. It is a proposed value-routing change with open design questions.

The useful investor takeaway is simple. MEV burn could improve ETH value accrual and staking fairness, but it is not a number-go-up coupon with protocol branding.

MEV burn does not automatically protect traders from bad execution. It changes who may capture or burn some ordering value at the protocol level. It does not make every swap safe.

If you trade through thin liquidity, use sloppy slippage settings, or route a large order through a visible public path, you can still become the meal. MEV burn may redirect part of the value chain, but a sandwich attack still begins with an order that can be anticipated and exploited.

That is where trader language helps. Some DeFi markets feel like PVP trading because one user’s poor execution can become another user’s profit. In the worst cases, late or careless buyers can also run into exit liquidity risk when liquidity is thin and everyone wants out.

Keep watching these risks even if MEV burn eventually ships:

MEV burn can change the protocol-level destination of some value. It does not replace trade sizing, route checks, slippage discipline, or skepticism toward any tool promising invisible protection.

The trader takeaway is less exciting and more useful. If your trade can be sandwiched today, a future burn proposal does not make today’s settings safer.

MEV burn sits beside several Ethereum roadmap terms, and the overlap can make the topic feel harder than it is. The key is to separate today’s market structure from proposed protocol changes.

MEV-Boost is part of today’s out-of-protocol builder and relay market. PBS means proposer-builder separation, where block building and block proposal become distinct roles. ePBS means enshrined PBS, where more of that separation moves into protocol rules. MEV burn is a proposed way to redirect some bid value inside that structure. Use this map before the acronyms pile up:

| Term | How It Relates To MEV Burn |

|---|---|

| MEV-Boost | Today’s out-of-protocol builder and relay setup used by many validators. |

| PBS | Separates block builders from block proposers. |

| ePBS | Moves that separation deeper into Ethereum protocol rules. |

| MEV Burn | Redirects part of builder bid value into ETH burn. |

| Execution Tickets | A related auction model for rights to build future execution payloads. |

| Inclusion Lists | A censorship-resistance tool that can force certain known transactions into blocks. |

Execution tickets matter because they show the roadmap is not a single-file queue. Some designs try to auction future execution rights. Others focus on PBS, inclusion, or bid rules. MEV burn can appear inside this wider auction-design debate, not always as a standalone upgrade.

MEV-Boost confusion is especially common. MEV-Boost helps validators access builder bids today, so it belongs in the current-market bucket. MEV burn belongs in the proposed-protocol-rule bucket. If the two get blended, a user can mistake active relay infrastructure for an upgrade that already burns ETH.

So when someone says “MEV burn is coming with ePBS,” ask what they mean. Dependency, research direction, final spec, and launch date are four different claims.

MEV burn still has open questions because MEV is slippery. Some value can be seen in builder bids. Some value can move through side deals, private order flow, timing games, or strategies the protocol cannot cleanly observe.

That does not make the proposal pointless. It means the final mechanism must handle incentives, not just ideals. If the design creates a burn floor that smart actors can route around, the burn captures less value than the simple story suggests.

The main open questions are practical:

Censorship resistance also needs careful handling. MEV burn may reduce some proposer incentives, but censorship risks need inclusion lists, builder checks, and other protocol tools. Burning bid value does not make block builders morally pure. It changes one part of the payoff.

The best case is a design that captures meaningful MEV value, smooths validator rewards, and reduces harmful incentives without making block production fragile. The worst case is a complex rule that looks clean on paper while value leaks through side doors.

Precise status language keeps the promise from outrunning the mechanism. MEV burn touches ETH economics, staking, and user execution, but the hardest parts are not solved by a tidy acronym.

You can reduce MEV risk today by improving trade execution habits. MEV burn is a roadmap idea, while your next swap uses the tools and liquidity available now.

Start with the parts you control. Slippage settings, order size, route choice, liquidity depth, and wallet or RPC defaults can change your outcome more than any future proposal you cannot use yet.

Use this checklist before sending a meaningful DeFi trade:

Wallets and RPC choices belong here because they shape how your transaction reaches the market. If a wallet advertises protected routing, look for clear details, not magic words. CryptoProcent’s wallet tools category can help you compare wallet-style features, but the protection claim still needs scrutiny inside the app you use.

Also remember that private routing can trade one risk for another. You may reduce public mempool visibility, but you might trust a relay, builder, wallet partner, or app path more than you realize. Hidden does not always mean safer.

The useful move is simple: act as if MEV burn will not save your current trade. That keeps you focused on the settings, routes, and liquidity conditions that decide your execution today.

No. MEV burn is best described as a proposed Ethereum roadmap and research idea, not a live feature users can see in every block. Ethereum already has fee burn through its current fee market, but that is separate from a proposed MEV bid burn.

The difference is important. If a wallet, dashboard, or post implies that MEV burn is already changing every Ethereum block, ask for the exact mechanism. Without a finalized design and live protocol support, that claim is ahead of the chain.

MEV burn has not disappeared from Ethereum research discussion, but it is not a finalized upgrade with a launch date. It sits inside a wider design space that includes PBS, ePBS, execution tickets, inclusion lists, and other ways to handle block building and MEV incentives.

So “abandoned” is too strong, while “imminent” is also too strong. The clean status is unresolved research and roadmap debate.

MEV burn would burn part of MEV-related builder bid value. EIP-1559 burns the transaction base fee from Ethereum’s live fee market.

Both can affect ETH supply, but they target different value sources. EIP-1559 is already part of Ethereum. MEV burn would need a design that can separate, price, and enforce part of builder bid value as burn instead of proposer income.

MEV burn could reduce ETH supply relative to a design where the same value goes fully to proposers. That does not guarantee ETH becomes deflationary.

Deflation depends on total issuance, fee burn, usage, staking dynamics, and the final MEV burn design. The exact burn formula and launch timing are not settled, so precise daily burn claims should be treated as speculation.

No. MEV burn does not automatically stop sandwich attacks. It may change where some ordering value goes, but a visible swap with loose slippage can still be exploited if the market path allows it.

Traders still need conservative slippage, sensible order sizing, route checks, and care around thin pools. Protocol-level value routing is not the same as wallet-level execution protection.

MEV burn usually depends on PBS or ePBS because the protocol needs a clearer separation between block builders and block proposers. That separation makes it easier to reason about builder bids, proposer tips, and any payload base fee that could be burned.

Without that structure, MEV value can be harder to observe and enforce at the protocol level. That is why MEV burn keeps appearing beside PBS and ePBS rather than as a simple fee switch users can toggle today.