Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Understand the hidden risks behind overcollateralized stablecoins.

An overcollateralized stablecoin is a stablecoin backed by more collateral value than the coins issued, usually to absorb crypto price swings.

That extra backing can help a stablecoin stay near its target price. But it does not make the token risk-free, and it does not guarantee that every holder can exit near $1 during a panic. The real work is finding where the risk moves: collateral quality, oracle prices, liquidation speed, governance settings, liquidity depth, and the borrower’s margin for error.

An overcollateralized stablecoin is a crypto-backed stablecoin design where the backing value exceeds the stablecoins in circulation. If a user deposits $150 of ETH and mints $100 of stablecoins, the stablecoin is backed by more value than the debt created.

You may also see the spelling variant “over collateralized stablecoin.” The meaning is the same. The design exists because crypto collateral can fall quickly, so the system needs a buffer before the backing value drops below the stablecoin debt.

That buffer is useful, but it is not magic. It helps absorb price moves, gives liquidators room to sell collateral, and can support confidence in the peg. It cannot make thin markets deep, slow crashes orderly, or bad governance harmless.

The term often appears in DeFi dashboards, stablecoin lists, lending markets, and yield vault risk notes. When a pool says a stablecoin is overcollateralized, it is pointing to the backing model, not handing you a safety certificate.

For a holder, the important question is simple:

For a borrower, the question changes. You need to know how close your collateral is to liquidation, how the oracle prices it, and what happens if the market gaps before liquidators clear the debt.

So the term is a starting point. It tells you the stablecoin has a collateral buffer. It does not tell you whether the collateral is good, liquid, unencumbered, or enough under stress.

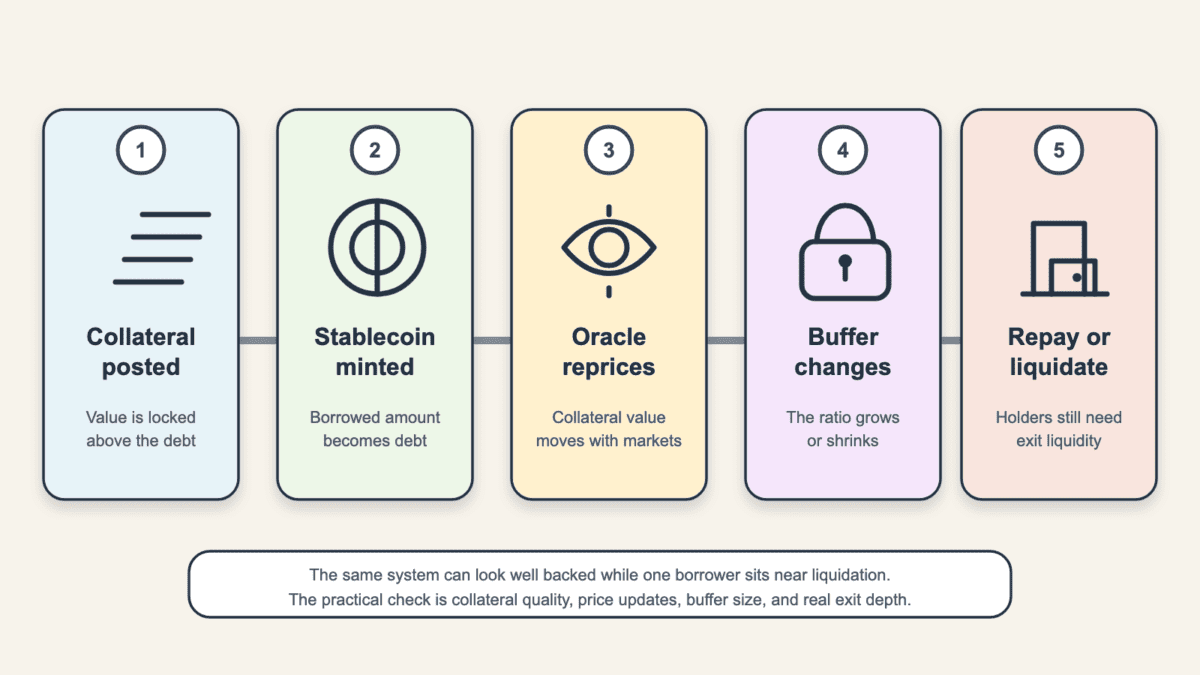

An overcollateralized stablecoin usually starts with a user depositing collateral, then minting or borrowing stablecoins against it. The protocol tracks the collateral value, the debt value, and the ratio between the two.

The basic flow is clearer as a sequence:

| Step | What The User Should Understand |

|---|---|

| Deposit collateral | The backing asset may be volatile, like ETH, BTC, or a liquid staking token. |

| Mint or borrow stablecoins | The stablecoins become debt against the collateral position. |

| Monitor the ratio | The position must stay above the required collateral level. |

| Update prices | An oracle feeds collateral prices into the protocol. |

| Trigger liquidation | If the ratio falls too far, collateral can be sold to repay debt. |

| Handle the result | The borrower may keep leftover collateral, or the system may face bad debt. |

The stablecoin’s peg depends on those moving parts working together. A high collateral ratio gives the system room, but the room can disappear when collateral sells off fast.

Diagram of the main overcollateralized stablecoin mechanics from collateral posting to liquidation, repayment, or holder exit.

Collateral ratio is the current relationship between collateral value and stablecoin debt. If a vault holds $180 of collateral against $100 of stablecoin debt, the collateral ratio is 180%.

Liquidation ratio is the line the position must not cross. If the required liquidation ratio is 150%, the same vault has a $30 cushion before the protocol can start selling collateral.

Those numbers sound similar, but they answer different questions:

This distinction catches many new DeFi users. A protocol can look strongly overcollateralized across all users while one individual vault is sitting inches from liquidation.

Say a user deposits $200 of ETH and borrows $100 of an overcollateralized stablecoin. The position starts at a 200% collateral ratio, which looks comfortable.

If ETH falls and the collateral is now worth $145, the ratio falls to 145%. If the protocol’s liquidation ratio is 150%, that position can be liquidated even though the stablecoin system may still be healthy overall.

In Maker-style systems, liquidation can involve auctioning collateral to repay debt, as in Maker Protocol Liquidation 2.0.

Liquidation is not a punishment in the moral sense. It is the enforcement mechanism that tries to keep the stablecoin backed before losses spread to everyone else.

But liquidation needs working markets. The oracle must update accurately, liquidators must show up, collateral must sell, and the sale must cover the debt plus penalties or fees. When any of those fail, excess collateral can shrink faster than the system reacts.

Extra collateral helps an overcollateralized stablecoin because it gives the system a buffer before stablecoin debt exceeds backing value. That buffer can support confidence, liquidation incentives, and arbitrage around the target price.

Think of it as a shock absorber. The protocol expects the collateral to move, so it asks for more collateral than the stablecoins created. If the collateral drops a little, the debt can still remain covered.

The buffer can support the peg in several ways:

That last point is easy to miss. Overcollateralization can make a stablecoin more resilient, but it also makes the design less capital-efficient. Locking $150 to create $100 does not scale as quickly as issuing $100 against $100 of cash-like reserves.

That tradeoff is the point. The design pays for resilience with trapped capital, borrowing costs, and liquidation complexity.

A strong overcollateralized stablecoin also needs collateral that can be sold without wrecking the market. ETH is easier to liquidate than a thin governance token. A liquid staking token may be useful, but it adds smart contract, redemption, and market-depth questions.

So extra collateral helps most when the collateral is transparent, liquid, and priced correctly. When the backing is fragile, bridged, correlated, or hard to sell, the headline ratio can flatter the real risk.

An overcollateralized stablecoin can still break when the buffer fails to cover the real-world path from collateral to repayment to user exit. The ratio helps, but it is only one part of the risk map.

The danger is comfort. “Overcollateralized” sounds like more safety than a user needs to think about. In practice, the design can fail through collateral crashes, stale prices, liquidator absence, weak liquidity, governance changes, bridges, or smart contract bugs.

Split the risk this way:

| Risk | What To Check |

|---|---|

| Collateral crash | How volatile and liquid the backing assets are. |

| Oracle failure | How prices update during fast markets. |

| Liquidation backlog | Whether liquidators can clear unsafe positions quickly. |

| Thin secondary markets | Whether holders can exit near the target price. |

| Governance change | Who can change collateral, fees, or risk settings. |

| Bridge exposure | Whether backing assets depend on wrapped or bridged claims. |

| Smart contract failure | Whether a bug can freeze funds or create bad debt. |

The table is not a scare list. It is the checklist behind the word “overcollateralized.”

Collateral quality risk starts with what backs the stablecoin. ETH, BTC wrappers, liquid staking tokens, real-world assets, and other stablecoins do not carry the same risk.

The best collateral is liquid, transparent, and easy to price. The weakest collateral can be volatile, concentrated, bridged, frozen, or tied to the same protocol that issues the stablecoin.

Stablecoin-on-stablecoin collateral can look calm until one peg slips. If a protocol backs its stablecoin with another stablecoin, the volatility may be lower, but the depeg risk becomes connected.

Oracle and liquidation risk covers whether the protocol reacts in time. If the price feed is stale, manipulated, delayed, or too slow for the market, unsafe positions can sit open longer than they should.

Liquidators then need incentives to act. They buy collateral, repay debt, and keep the system solvent. If gas fees spike, collateral is hard to sell, or the discount is too small, liquidation may not clear fast enough.

This is why a borrower should track the liquidation price, not just the stablecoin peg. The peg can look fine while a vault is already close to the edge.

Liquidity risk is the holder’s version of the problem. A stablecoin can be backed on paper and still be hard to sell near $1 when everyone wants out.

Good exit liquidity means there are real routes out: deep pools, redemptions, swap modules, exchange support, and enough buyers when stress hits. Thin liquidity turns a small depeg into a very annoying lesson.

This is how a holder can become a bagholder in the plainest crypto sense. The collateral dashboard may still look respectable, but the exit door can be narrow.

Governance risk comes from human-controlled parameters. Collateral types, stability fees, liquidation penalties, debt ceilings, and emergency actions can all change.

Bridge risk appears when collateral exists on another chain or depends on wrapped assets. A bridge failure can damage the backing even if the stablecoin contract works as designed.

Smart contract risk is the base layer under all of this. If the vault, oracle, liquidation, or swap module has a bug, the collateral ratio may become less useful than it looked on the dashboard.

The takeaway is blunt: overcollateralization is a risk control. It is not a promise that the peg, collateral, market, and exit route will behave at the same time.

An overcollateralized stablecoin differs from fiat-backed and algorithmic stablecoins by how it creates confidence in the peg. The backing model changes what users must trust.

Exogenous collateral means the backing has value outside the stablecoin system. ETH, BTC, Treasury bills, or cash-like reserves are exogenous. Endogenous collateral means the backing is tied to the same system, often through a related token.

That distinction helps explain why the word “algorithmic” still makes many crypto users tense. Terra UST made reflexive stablecoin design a permanent warning label for many people.

| Stablecoin Type | Main Failure Mode |

|---|---|

| Fiat-backed stablecoin | Issuer, reserve, banking, freeze, redemption, or regulatory access risk. |

| Crypto-backed overcollateralized stablecoin | Collateral crash, oracle failure, liquidation failure, governance risk, or thin liquidity. |

| Endogenous algorithmic stablecoin | Reflexive collapse if confidence in the related token breaks. |

| Hybrid stablecoin | Mixed risks from reserves, crypto collateral, algorithms, governance, and liquidity. |

No model wins every tradeoff. Each one moves trust to a different place.

Fiat-backed stablecoins usually rely on an issuer holding reserves such as cash, bank deposits, short-term government debt, or similar assets. USDC and USDT are the common reference points.

The user trust assumption is simpler to understand: does the issuer hold enough reserves, manage them properly, and redeem when needed? But simplicity does not remove issuer power, freeze risk, banking exposure, or regulatory access issues.

Fiat-backed stablecoins can be easier for beginners because the backing story sounds familiar. The tradeoff is that you trust the issuer and its reserve chain, not a vault liquidation system.

Crypto-backed overcollateralized stablecoins use on-chain collateral and rules for minting, repayment, and liquidation. DAI, LUSD, crvUSD, and GHO are common examples users may see in DeFi.

The benefit is transparency when collateral and debt are visible on-chain. The cost is more moving parts. You must understand vaults, oracles, liquidations, governance settings, and the actual liquidity around the stablecoin.

These stablecoins can reduce dependence on a bank issuer, but they add protocol and market risk. It is a trade, not a free upgrade.

Endogenous algorithmic stablecoins depend heavily on a related token or internal incentive loop to defend the peg. When confidence falls, the backing and the stablecoin can weaken together.

Hybrid designs mix pieces from several models. They may include reserves, crypto collateral, algorithmic controls, governance rules, and incentive programs. The label alone does not tell you enough.

For users, check whether the collateral has real value outside the stablecoin itself. If the backing depends mainly on belief in the same system, the risk is more reflexive.

Borrowers use an overcollateralized stablecoin when they want liquidity without selling the crypto they deposited. That can make sense when they want to keep exposure, manage timing, or use capital elsewhere.

The simple objection is fair: why lock $150 to borrow $100? Because the borrower may want the $100 now while still owning the asset they deposited.

That choice only works when the loan size leaves room. A small borrow against a large collateral stack can handle normal volatility. A high borrow makes every price wick feel like an emergency notification.

The debt also changes the portfolio. The borrower now has two jobs: use the stablecoins well and keep the collateral position alive. If the borrowed funds go into another trade, liquidity pool, or yield strategy, losses can stack on both sides.

Common reasons include:

That last point is not tax advice. It is just one reason borrowing exists.

A borrower accepts two costs. First, the position can be liquidated if collateral falls too far. Second, the loan may carry a stability fee, interest cost, or other protocol charge.

Consider a cleaner example. A user deposits $10,000 of ETH and borrows $4,000 of stablecoins. They still have ETH exposure, but their liquidation price becomes the key number. If ETH drops enough, the protocol can sell collateral to protect the stablecoin debt.

Good borrowers work backward from a bad day, not from the amount they wish to spend. They decide how much collateral they are willing to lose, how quickly they can repay, and whether they can add collateral if the oracle moves against them.

That is the deal. The borrower keeps exposure and gets liquidity, but buys that flexibility with liquidation risk.

Examples of overcollateralized stablecoins show that the label covers several designs. Some are vault-based, some are lending-market based, and some mix collateral with governance or stabilization tools.

Do not read the list as a ranking. The point is to see what each example teaches about the design.

| Example | What It Illustrates |

|---|---|

| DAI | Vault-based stablecoin issuance, mixed collateral, and governance-controlled risk settings. |

| USDS | The Sky-era continuation of the DAI family, with current governance and collateral tradeoffs. |

| LUSD | A crypto-backed design focused on ETH collateral and liquidation mechanics. |

| crvUSD | A DeFi-native stablecoin tied to lending and automated liquidation design. |

| USDD | A hybrid label where users should inspect reserves, collateral, governance, and liquidity. |

| Djed | A design often discussed in the overcollateralized versus algorithmic label debate. |

| GHO | A lending-protocol stablecoin tied to Aave-style borrowing and risk controls. |

The pattern is more useful than the names. Every example forces the same questions: what backs it, how liquid is the backing, who controls parameters, and how does the stablecoin return to target when stressed?

DAI and USDS are useful because they show the messy middle. A stablecoin can be called decentralized while still using collateral, governance, and modules that create different trust assumptions.

As of June 21, 2026, DefiLlama’s stablecoin dataset showed Sky Dollar (USDS) at about $8.17 billion in circulating supply.

LUSD shows why some users like narrower collateral models. A smaller collateral set can be easier to understand, though it may also concentrate risk.

crvUSD and GHO show how DeFi-native stablecoins can connect issuance to lending markets. That can make the mechanics elegant, but it also means borrowers, liquidity pools, and protocol parameters all matter.

USDD and Djed show why labels need inspection. A project may describe itself as overcollateralized, algorithmic, reserve-backed, or hybrid. The label is the cover. The collateral and exit route are the book.

Evaluate an overcollateralized stablecoin by separating your role first. A holder, borrower, and yield farmer are exposed to different parts of the same design.

Start with the stablecoin’s backing and exit route. Then move to your own position risk. If you jump straight to yield, you are reading the dessert menu before checking the kitchen.

Holder checks focus on whether the stablecoin can stay near target and whether you can leave when needed. The peg chart is only the first screen.

Use these checks before holding meaningful size:

Custody is part of the stablecoin experience. If you hold an on-chain stablecoin yourself, wallet setup, approvals, seed security, and contract interactions become practical risks.

Borrower checks focus on liquidation. The stablecoin may be sound while your vault is fragile.

Before borrowing, check the mechanics that affect your position:

Then stress the position. Ask what happens if collateral drops 20%, if network fees spike, or if liquidity thins when everyone tries to adjust at once.

Yield-farming checks start with one question: who is paying the yield? The answer should be visible enough to explain without hand-waving.

Stablecoin yield can come from borrower interest, reserve income, trading fees, token incentives, or looped borrowing. Each source carries a different risk.

Before using an overcollateralized stablecoin in yield farming, check these points:

High yield should not trigger automatic excitement. It should trigger better questions. Stablecoin yield can be useful, but “stable” describes the target price, not the full risk stack.

Start with the collateral, not the label. An overcollateralized stablecoin is only as strong as the backing, pricing, liquidation, governance, and liquidity around it.

If you are evaluating one for the first time, use a short order of operations:

Then choose your role. Holding a stablecoin, minting it, borrowing against collateral, and farming it are different activities. Each one has a different failure point.

Those checks should happen before any APY, brand name, or decentralization pitch gets a vote. If the stablecoin cannot explain collateral and exits clearly, a small test position is the ceiling, not the warm-up.

For small experiments, use a crypto wallet and chain you understand, avoid complex loops, and keep enough room above liquidation if you borrow. Boring risk management is still undefeated.

For larger amounts, do not stop at the peg chart. Look at collateral quality, pool depth, oracle design, governance controls, bridge exposure, and the actual source of any yield.

The final check is boring but useful: decide how you will get out before you get in. If that exit route depends on one thin pool, one bridge, or one governance promise, the stablecoin deserves a smaller role than the headline collateral ratio suggests.

An overcollateralized stablecoin is a stablecoin backed by more collateral value than the stablecoins issued. The extra collateral acts as a buffer against volatile backing assets, but it does not remove liquidation, liquidity, governance, or smart contract risk.

Yes, DAI is commonly understood as an overcollateralized stablecoin design because users can create it through collateralized vaults. Its current risk profile also depends on collateral mix, governance decisions, liquidity, and the broader Sky Protocol transition.

Yes, an overcollateralized stablecoin can lose its peg if collateral falls too fast, liquidations fail, liquidity dries up, governance changes weaken trust, or holders cannot exit near the target price. Extra collateral helps, but it does not guarantee a $1 trade.

An overcollateralized stablecoin is not automatically safer than USDT or USDC. It has different risks. Fiat-backed stablecoins rely more on issuers, reserves, and redemption access, while overcollateralized stablecoins rely more on collateral quality, oracles, liquidations, governance, and market liquidity.

Overcollateralized stablecoins need liquidations because collateral can fall below the required safety buffer. Liquidation sells enough collateral to repay debt, protect the stablecoin backing, and stop one weak vault from pushing losses into the wider system.

Overcollateralized stablecoins can be useful in yield farming, but the yield source decides the risk. Borrower interest, trading fees, token incentives, and looped lending all behave differently when liquidity falls or the stablecoin depegs.