Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A plain-English Pendle guide for PT, YT, maturity, and yield risk.

Pendle is a DeFi protocol that splits a yield-bearing crypto asset into principal and future-yield claims.

With that split, users can buy fixed-style yield, trade future yield, provide liquidity, or hold the PENDLE token as a separate protocol-token bet. Each route carries different risks. A neat APY on a dashboard does not explain the asset, maturity date, liquidity, contracts, or exit path underneath it.

Pendle makes more sense when you stop reading it as a yield billboard. It is a market for future-yield choices. Before the wallet pop-up starts looking friendly, know which side of that market you are taking.

Pendle in crypto is a DeFi yield-trading protocol. It takes assets that already earn some kind of yield and turns that bundled position into tradable pieces.

Those pieces are mainly PT and YT. PT stands for Principal Token, the principal side of the position. YT stands for Yield Token, the future-yield side until a maturity date.

That makes Pendle different from a simple earn account. In a normal yield product, the principal and yield stay bundled together. You deposit an asset, the rate changes, and you accept whatever the position earns.

Pendle lets the market separate those choices. One user may want the fixed-style return from buying PT at a discount. Another may want YT because they think future yield, points, or incentives will be stronger than the market expects. A third may provide liquidity and earn trading fees while taking market-making risk.

Pendle Finance is the broader protocol brand. Pendle is also used casually for the app, the protocol, and the markets inside it. PENDLE, in all caps, is the protocol token. That token can be tied to governance, incentives, and market sentiment, but it is not the same thing as a PT, YT, or fixed-yield position.

That distinction matters before any trade. Using Pendle is about choosing an exposure. Buying PENDLE is a token thesis. Buying PT is a maturity-based yield position. Buying YT is a future-yield trade. Same family, very different meal.

Pendle exists because DeFi yield changes constantly. Lending demand, staking rewards, incentives, stablecoin flows, market stress, and points campaigns can all change what a position earns.

That floating-rate world is normal in DeFi. It is also awkward. If you deposit into a lending market today, tomorrow’s rate can be lower. If rewards end next month, the headline APY can shrink before your spreadsheet has finished pretending to be useful.

Traditional yield farming often accepts that movement and chases the next reward source. Pendle takes a different route. It creates a market where users can trade that uncertainty.

The split is useful because different users want different things:

Those goals should not be squeezed into one APY number. Pendle separates them so the market can price each side.

The result is not magic fixed income. It is a DeFi market for rate expectations. If many users crowd into the same PT market, the implied return can compress. If demand for YT rises because points look attractive, YT can become expensive. Pendle makes those views tradable, but it also makes them easier to misread.

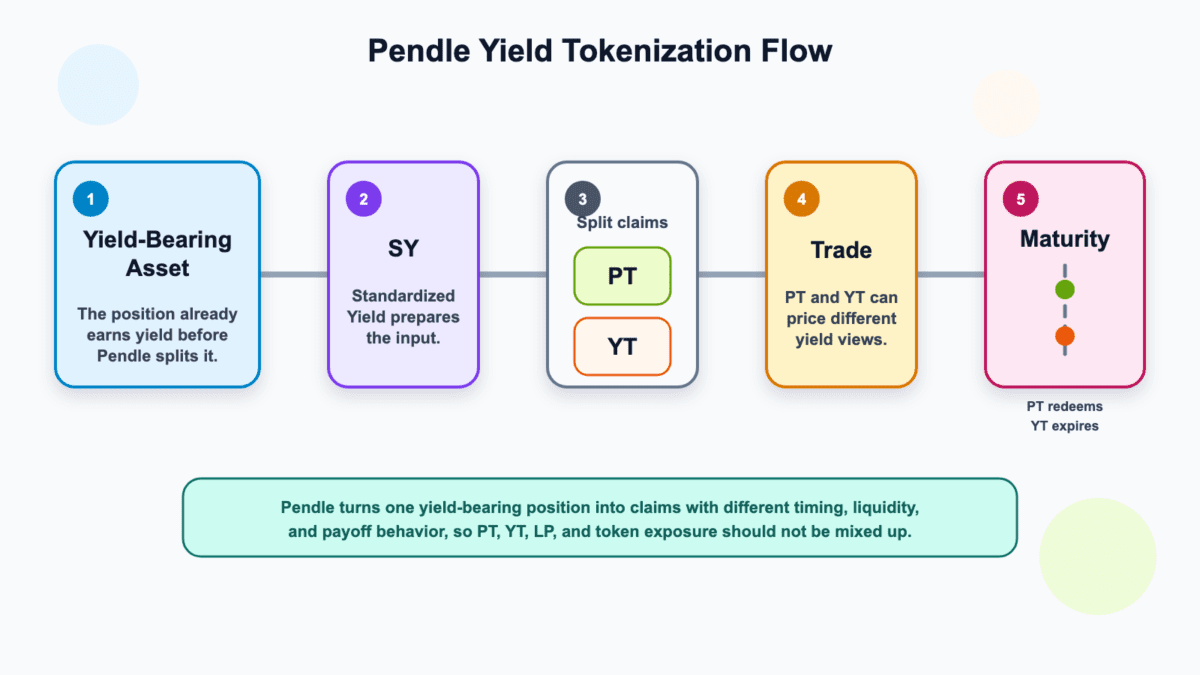

Pendle works by wrapping a yield-bearing asset into a standard format, splitting it into principal and yield claims, then letting those claims trade until maturity. That core path is yield tokenization: an asset is wrapped as SY, split into PT and YT, then traded through Pendle markets.

The lifecycle starts with something that can earn yield. That might be a liquid staking token, a yield-bearing stablecoin, a lending position, a restaking asset, or another supported asset type.

Pendle then makes that position easier for its own market to handle. After that, users are no longer looking at one bundled yield position. They are looking at claims with different behavior, different buyers, and different failure paths.

Standardized Yield, or SY, is the wrapper step that makes different yield-bearing assets usable inside Pendle markets. It turns varied assets into a common format before the split happens.

The wrapper is useful because yield-bearing assets do not all behave the same way. A liquid staking token, a stablecoin receipt, and a vault share can have different accounting, rewards, and redemption paths. SY is the protocol’s way of preparing those inputs for PT and YT.

Users do not need to obsess over SY first. They do need to know that SY does not remove the risk of the underlying asset. If the starting asset has depeg, redemption, oracle, contract, or liquidity risk, Pendle inherits that risk rather than politely deleting it.

A Principal Token, or PT, is the claim to the principal side of the position at maturity. It is the side most users mean when they talk about fixed yield on Pendle.

PT often trades at a discount to its expected redemption value. If the position works as expected and the holder waits until maturity, that discount can become the fixed-style return. The math can be clearer than a floating APY, but the path still depends on the asset and redemption route.

PT is usually the cleaner starting point for cautious users because the question is fairly direct: what does it redeem into, when, and what can break before then?

A Yield Token, or YT, is the claim to future yield before maturity. It is not the quieter fixed-yield side.

YT can attract users who think future yield, rewards, points, or incentives will beat the market’s current expectation. That can make YT powerful when the view is right. It can also make YT painful when yield disappoints, points get repriced, or time decay starts doing its quiet little job.

So YT belongs in the active-trade drawer. It can be useful, but it asks for a stronger view than “the APY looked nice.”

Maturity is the date that anchors a Pendle market. It controls when PT can be redeemed under the market’s terms and when YT stops representing future yield for that market.

Before maturity, PT and YT can trade at market prices. That means users can exit early if there is enough liquidity, but the price may not match the neat implied return shown at entry. After maturity, the position changes from trading logic to redemption or expiry logic.

Maturity is where Pendle becomes less like a spot token and more like a dated yield position. If your time horizon is shorter than the maturity, you are relying on the secondary market. That is a different risk from holding to redemption.

Pendle PT, YT, LP positions, and the PENDLE token are separate exposures. Confusing them is one of the easiest ways to buy the wrong exposure.

The app may place them near each other, and social posts may talk about them in the same breath. But the return path changes sharply depending on the position.

Use this split before treating every Pendle-related ticker as the same bet.

| Position | What The User Is Really Exposed To |

|---|---|

| PT | A principal claim with fixed-style return potential if held to maturity and redeemed as expected. |

| YT | Future yield, points, incentives, rate movement, and time decay before maturity. |

| LP Position | Trading fees, pool balance changes, PT/YT market movement, and liquidity-provider risk. |

| PENDLE Token | Protocol-token exposure, governance and incentive narratives, market sentiment, and token-specific risk. |

The table is not a ranking. It is a map of what you are actually buying.

PT is usually the closest thing to a fixed-yield position. YT is more speculative. LP positions can earn fees but carry market-making exposure. PENDLE is a token investment, not a claim on one specific PT maturity.

LP exposure often gets missed because it sounds passive. It is not only “deposit and earn.” The liquidity provider is helping the market trade PT and YT, so pool balance, pricing, volume, fees, and market movement all matter.

The PENDLE token sits even farther from the maturity math. A user can be right that Pendle markets are useful and still be wrong about the token entry, supply pressure, or broader market timing.

This is why “I am bullish on Pendle” is incomplete. Bullish on what? The protocol? The PENDLE token? Stablecoin PT demand? Future yield from YT? Those answers can point to different trades with different downside.

Fixed yield on Pendle usually means a PT buyer can know the entry price, the maturity date, and the expected redemption value. If the holder waits and the position settles as expected, the return math can be fixed-style.

That is not the same as guaranteed yield. The “fixed” part describes the pricing path, not the safety of every layer below it. The underlying asset can still lose value. A stablecoin can depeg. A contract can fail. A market can be hard to exit before maturity.

Here is the simple version. Imagine a PT that should redeem for 1 unit of an underlying asset at maturity. If a user buys it for 0.94 units, the expected gross return is the gap between the price paid and the redemption amount.

The actual result still depends on several checks:

Implied APY is the market’s translation of that discount and time remaining. It can move before you enter because PT prices move. It can compress when capital crowds into the same market. It can also look high because the market is charging you to carry real risk.

So read fixed yield on Pendle as “fixed if the terms work and you hold the right thing to maturity.” It is a useful structure. It is not bubble wrap.

Pendle risk starts with the underlying asset, then adds protocol, market, maturity, and wallet risk on top. The headline APY is only one part of the position.

Stablecoin PT markets show the problem clearly. A fixed-style stablecoin return can look tidy, but the user still needs to care about depeg risk, issuer or protocol risk, chain liquidity, maturity timing, slippage, and what happens if they need to exit early.

Early exits are a separate risk. Selling PT or YT before maturity depends on exit liquidity, not just the number shown on the market page. Someone has to buy the position at a price that still makes your trade work.

Use this checklist before any Pendle position becomes real money.

| Check | Why To Check It |

|---|---|

| Underlying asset | Pendle cannot make a weak asset safe just by splitting it into PT and YT. |

| Maturity date | PT and YT behavior changes as the market approaches expiry. |

| Redemption asset | The position may redeem into a token with its own liquidity, peg, or wrapper risk. |

| Implied APY | The displayed return comes from market pricing, not a permanent offer. |

| Early-exit depth | Thin markets can erase the expected return through slippage. |

| Rewards and points | Extra upside may be speculative, delayed, or repriced by the market. |

| Chain and bridge route | Moving assets across networks can add fees, delays, and contract risk. |

| Wallet approval | A bad signature can be worse than a bad APY. |

The checklist is meant to slow the click, not scare you away. Pendle can be useful when the position is clear. It gets dangerous when a user cannot explain what backs the yield, what date controls the trade, or how they would exit if the market turns.

Social walkthroughs deserve extra caution. A thread can make a strategy look clean while skipping referral incentives, thin liquidity, bridge steps, and reward assumptions. Copying the route without copying the risk work is how a smart-looking strategy becomes expensive tuition.

Traders watch Pendle because it creates market prices for future yield. Instead of only accepting a floating APY, users can express a view on rates, incentives, points, and demand for fixed-style yield.

Pendle has enough scale for that signal to carry weight. Pendle listed roughly $1.01 billion in total value locked on June 21, 2026, but the useful view is still market by market. Check the maturity, asset, and exit depth instead of assuming every pool is equally liquid.

That makes Pendle useful beyond one yield dashboard. PT markets can show what users are willing to accept for fixed-style exposure. YT markets can show how aggressively traders value future yield or points. Liquidity demand can show which assets the market wants to price.

Token investors watch a different layer. PENDLE may benefit from attention around protocol usage, market growth, incentives, or governance. But a PENDLE position is still a token bet. It does not automatically earn the yield shown on a PT market.

This is where narrative risk enters. A trader may see Pendle as a conviction play on tokenized yield or DeFi rate markets. That thesis can be reasonable, but it should not be mixed up with a specific PT maturity or a YT points trade.

The useful split is simple. Protocol use can make Pendle more relevant. Token performance depends on token supply, demand, incentives, governance value, market mood, and broader crypto liquidity. Those forces can overlap, but they do not move in lockstep.

So traders care because Pendle turns yield expectations into prices. Investors care because those markets may support a broader token story. The mistake is pretending those are the same trade with different fonts.

Pendle Boros adds a more advanced rate-trading branch to the Pendle product family. Instead of focusing on PT and YT markets for DeFi yield-bearing assets, Boros is tied to funding-rate exposure.

Funding rates are periodic payments in perpetual futures markets. They can change with positioning, market demand, and borrowed exposure. Traders watch them because they can reveal pressure between long and short exposure.

Boros aims to make that kind of rate exposure tradable in a Pendle-style format. In plain English, it gives advanced users another way to express a view on future funding rates, hedge rate exposure, or trade rate expectations.

That does not make Boros the right starting point for a beginner. A user should understand PT, YT, maturity, implied yield, liquidity, and wallet signing before moving into funding-rate products.

The main difference is the input. Core Pendle markets usually start with yield-bearing crypto assets. Boros starts with rate exposure from perpetual markets, where positioning and funding can change fast. That makes the product more sensitive to trader behavior.

Keep Boros in the advanced drawer:

Boros is worth knowing because it shows Pendle moving beyond basic yield tokenization. It should not hijack the core lesson: first understand what claim you are buying, what date controls it, and what market lets you exit.

Pendle is beginner-friendly only for users who already understand basic DeFi risks. It is explainable, but it is not the cleanest first app for someone still learning wallets, approvals, bridges, and yield sources.

A careful beginner can still learn from Pendle without signing anything. Open a market, identify the underlying asset, compare PT and YT, read the maturity date, and watch how implied APY changes. That teaches more than blindly chasing the highest number.

Before using Pendle, a user should be able to answer a few plain questions:

The wallet route is not a footnote. Users comparing crypto wallets should care about transaction previews, hardware-wallet support, approval visibility, network support, and spam protection before using DeFi positions with real value.

Pendle is less suitable when the user cannot explain where the yield comes from. It is also a poor fit when the whole plan is “I saw a big APY and a confident thread.” That is not a strategy. That is a vibes-based onboarding process with gas fees.

Start with observation. Read markets, compare maturities, trace the asset, and learn the interface with no transaction pending. If the position still makes sense after that, size it like a DeFi experiment, not a savings account.

Pendle is a crypto protocol for trading future yield. It separates an interest-earning asset into a principal side and a future-yield side, so users can choose which exposure they want.

The important caveat is that the split changes the risk. PT, YT, LP positions, and PENDLE token exposure do not behave the same way.

No, Pendle fixed yield is not guaranteed. PT can create fixed-style return math if bought at a discount and held to maturity, but the position still depends on the asset, contracts, liquidity, and redemption path.

“Fixed” describes the structure of the return under the market terms. It does not mean risk-free.

PT on Pendle is the principal side, while YT is the future-yield side. PT is usually used for fixed-style yield exposure, and YT is usually used for future yield, points, or rate speculation.

The difference becomes sharper near maturity. PT moves toward redemption logic. YT loses the time left to capture future yield.

When a Pendle market reaches maturity, PT can usually be redeemed under the market’s terms, while YT stops representing future yield for that maturity. The exact route depends on the market and supported asset.

Before maturity, users may trade PT or YT if the market has enough liquidity. After maturity, the focus shifts to redemption, expiry, or rolling into another market.

No, buying PENDLE is not the same as earning yield on Pendle. PENDLE is the protocol token, while PT, YT, and LP positions are market exposures inside the protocol.

A token thesis can be connected to Pendle usage, but it is not the same as holding a dated PT or trading future yield with YT.

Pendle Boros is an advanced product focused on funding-rate exposure. It is meant for users who want to trade or hedge views on rates in perpetual futures markets.

Boros should come after the core Pendle mechanics. If PT, YT, maturity, and implied APY still feel fuzzy, Boros is too early.

Start with Pendle by reading the market before using the market. The goal is to understand the claim, the date, and the exit path before a wallet signature turns curiosity into exposure.

Spend the first pass comparing markets, not choosing a winner. Look at one stablecoin market, one ETH-related market, and one market with a shorter maturity. The differences will show how pricing, depth, and time left can change the same basic PT/YT logic.

Do not compare markets only by the largest APY. Compare the extra return with the extra work. A small premium over a simpler route may not justify a new chain, a new approval, and a maturity date you might forget.

Run these checks first:

If one check is unclear, stop there. Pendle rewards patience more than speed because the trade depends on several moving parts, not just one attractive number.

Write the position in one sentence before signing: I am buying this claim, backed by this asset, maturing on this date, and I plan to exit this way. If that sentence breaks, the position probably breaks too.

Then ask one blunt question: what would make this position lose money even if the interface number looked good? If the answer is vague, the trade is not ready.

Pendle is most useful when it turns yield into a deliberate choice. It is least useful when it turns a confusing APY into a fast click. Let the former win.