Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A practical guide to post-TGE selloff risk, launch dumps, and rebound traps.

A post-TGE selloff is a price drop after a token generation event, when newly tradable tokens meet immediate selling pressure.

That first drop can look dramatic because launch markets are messy. Airdrop claimants, public-sale buyers, market makers, private investors, and hype-driven buyers all meet at once, often before the market knows what the token is worth.

Do not stop at “did it dump?” Many new tokens do. Ask who can sell, who still wants to buy, and whether the chart shows normal price discovery or late buyers becoming the exit door.

A post-TGE selloff in crypto is the first wave of selling after a token generation event. TGE means Token Generation Event, the moment a project creates or distributes its token and prepares it for claims, listings, or trading.

“Selloff” means sellers are hitting bids or swapping into available liquidity faster than buyers are absorbing supply. In plain terms, more people want out at that moment than in.

Break the phrase into three parts:

The phrase usually appears around airdrops, launchpad sales, points programs, and new exchange listings. A token goes live, wallets receive supply, and the first liquid market forms. Then the chart falls because some holders see the launch as payday, not the start of a long relationship.

That does not make every post-TGE selloff a scam. Some drops are normal launch mechanics. Free or discounted tokens often meet thin liquidity, and early price discovery can be brutal before real demand forms.

But the pattern can also expose bad design. If the token launches with a tiny float, a huge fully diluted valuation, vague allocations, and little use beyond speculation, the selloff may reveal that the market was priced for perfection before buyers had any proof.

The clean takeaway is simple. By itself, a post-TGE selloff is a prompt. Inspect supply, incentives, liquidity, and behavior before deciding whether the drop is noise or a real warning.

A post-TGE selloff happens because new sellable supply arrives before stable demand is proven. Launch day compresses months of incentives into one crowded market window.

Airdrop claimants may have no cost basis. Farmers may have spent time, gas, or capital to qualify, then sell quickly to lock in reward value.

Public-sale buyers may sell if the listing price gives them an instant gain. Private investors and teams may not be able to sell immediately, but the market still watches their future release schedule.

Airdrop farming shows the incentive problem clearly. Farmers often optimize for eligibility, not loyalty. Once the claim opens, many rotate to the next opportunity because their job was to earn the allocation, not marry the token. Romantic, it is not.

The seller side usually has several cohorts:

| Seller Cohort | Why They May Sell After TGE |

|---|---|

| Airdrop Claimants | They received tokens and may want to realize value quickly |

| Points Farmers | They may rotate capital to the next farming campaign |

| Public-Sale Buyers | They may sell if the listing price beats their entry |

| Market Makers | They may manage inventory while supporting early liquidity |

| Private-Round Holders | They may not sell at TGE, but later releases can pressure price |

| New Buyers | They may flip fast if the launch candle fails |

Liquidity is the other half. A centralized exchange listing may show an order book, but the book can still be shallow near launch. A DEX pool may allow trading, but a small pool can move sharply when claimants sell. In both cases, the first market can look deeper than it really is.

Low float and high FDV can make the chart even more fragile. A small tradable supply can pump into launch attention, while the implied full-supply valuation already looks stretched. Once sellers arrive, buyers may wait for lower prices instead of catching the first knife.

Community slang often labels fast sellers as “jeets.” The term can be useful shorthand for early exits, but it can also become lazy blame. A seller taking profit after a claim is not automatically malicious. Check whether the launch structure made mass selling predictable.

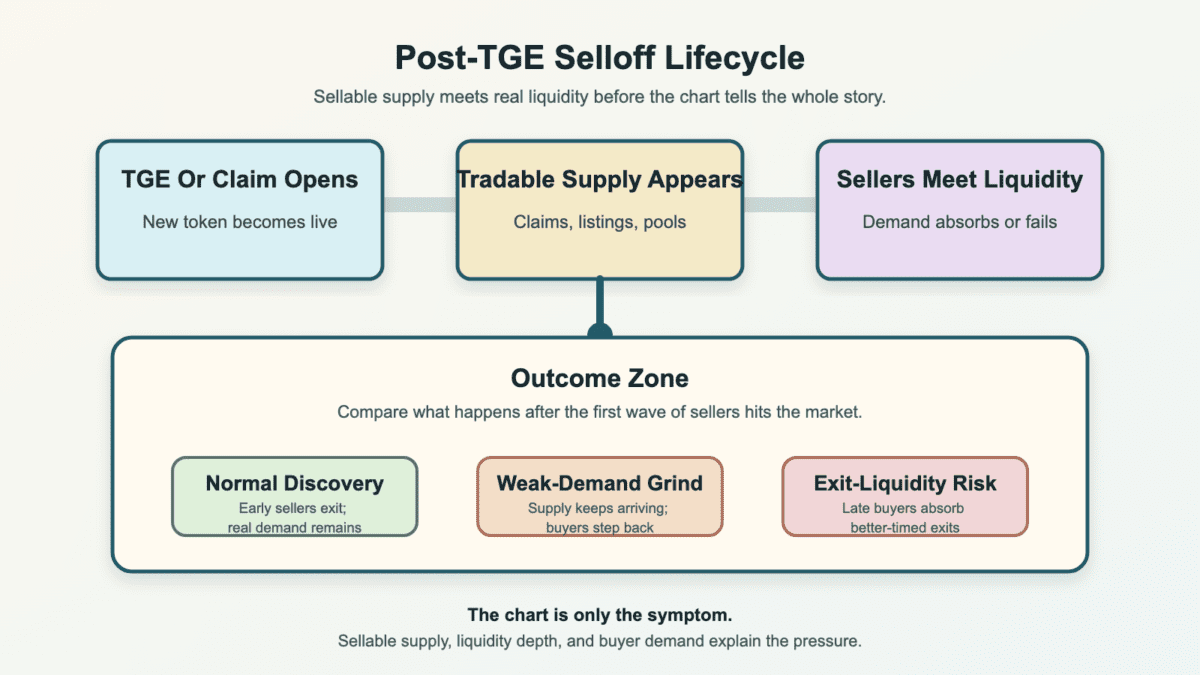

The lifecycle is simple. Tokens become tradable, seller cohorts meet available liquidity, and the market sorts the outcome. The result can be normal price discovery, a slow weak-demand grind, or a setup where late buyers absorb better-timed exits.

A post-TGE selloff on the chart often starts with a sharp listing move, then fades as claimable supply reaches the market. The chart can look like a launch spike followed by lower highs, failed rebounds, and heavy turnover.

The first candle is often the least useful candle. It may reflect tiny liquidity, market-maker setup, listing excitement, or thin early fills. That price can become a headline before it becomes a real market.

Common chart features include:

A crowded launch can also become a top signal when hype prices the token before the market has tested real demand. If everyone arrives for the first candle, the next buyer may already be scarce.

Still, price action has limits. A falling chart cannot tell you whether insiders are dumping, farmers are rotating, or buyers are simply waiting. You need tokenomics, holder data, liquidity depth, and communication history to understand the cause.

Fake rebounds deserve special caution. A token can bounce because early selling paused, not because demand changed. If the bounce comes on thin volume while more claims or releases are pending, it may only reset the next wave of sellers.

The chart tells you pressure exists. It does not tell you whether the pressure is finished.

A post-TGE selloff is normal price discovery when the market is simply finding a fairer price after launch supply becomes tradable. Early markets are noisy, and the first quoted price may be more theater than truth.

Free or discounted allocations create obvious selling pressure. Some claimants need cash. Some farmers want to recycle capital. Some buyers planned to flip from the start. If the token still has active users, clear supply data, and enough liquidity, the selloff may be ugly without being fatal.

Timing can hurt too. A strong project can list into a weak market, a crowded unlock week, or a risk-off tape. In that case, selling pressure may reflect broader conditions as much as project quality.

Healthy post-TGE price discovery usually has a few practical signs:

Normal does not mean safe. It only means the drop has a reasonable mechanical explanation. A token can fall for normal reasons and still fail to recover if demand never grows beyond the launch crowd.

Recovery depends on new demand meeting a cleaner supply picture. If short-term sellers leave and actual users arrive, the token can stabilize. If only the narrative remains, the chart may keep asking for fresh believers until it runs out.

So do not call every launch dump a rug. Also do not call every dump “healthy price discovery” because that sounds calmer. The useful middle ground is to match the drop with the supply calendar and buyer demand.

A post-TGE selloff starts looking like exit liquidity when public buyers are mainly absorbing supply from better-positioned sellers. The risk is strongest when the launch story hides who can sell, when they can sell, and why demand should continue.

Exit liquidity risk does not require a dramatic rug. It can happen when late buyers chase a token after insiders, farmers, or early buyers already have the better exit path. The market still functions, but the timing is tilted.

The warning signs usually arrive in clusters. One red flag can be noise. Several together deserve attention.

Watch for these patterns:

The community joke that TGE means “Team’s Gonna Exit” is not the literal definition. It is a criticism. People use it when a launch feels designed for insiders to monetize attention while public holders carry the downside.

Different failure patterns need different names:

| Pattern | What It May Mean |

|---|---|

| Normal Claim Selling | Recipients take profit, but supply details and liquidity remain clear |

| Weak-Demand Grind | Sellers keep arriving while new buyers wait or leave |

| Soft-Rug Drift | Updates fade, insiders benefit, and holders keep hoping |

| Hard-Rug Collapse | Liquidity, sellability, or project control breaks suddenly |

| Exit-Liquidity Setup | Public demand absorbs supply from better-positioned sellers |

A gradual soft rug can look like a slow version of post-TGE disappointment. Delivery fades, communication becomes vague, and holders are kept around by hints rather than evidence.

A hard rug is more severe. It involves direct abusive behavior, such as removed liquidity, blocked selling, malicious contract changes, or a sudden project disappearance. A normal post-TGE selloff should not be mislabeled as that without stronger proof.

Behavior beats vibes here. If wallets tied to insiders keep exiting while public messaging asks for patience, risk has changed. If the team explains supply, shows progress, and liquidity remains functional, the drop may be painful but less suspicious.

To check post-TGE selloff risk before buying, inspect the supply schedule, live liquidity, holder behavior, and the reason buyers should keep showing up after the claim rush. Do that before the chart tempts you into “cheap” mode.

Start with tokenomics. Find circulating supply, total supply, FDV, initial float, allocation buckets, and the first major release date. A token can look small by market cap while pricing a much larger future supply.

Then compare supply with actual market depth. A token may trade on a CEX, a DEX, or both, but venue access is not the same as durable liquidity. Thin books and shallow pools can turn a modest sell wave into a cliff.

Use this checklist before chasing a rebound:

Rebound checks help too. A lower price is not enough. You want signs that selling pressure is slowing, liquidity is holding, and buyers have a reason beyond “surely it cannot go lower.” Crypto enjoys humiliating that sentence.

Bottom-signal checks can help here. They push you to look for confirmation, such as calmer sell volume, stronger bids, clearer news, or improving holder behavior, rather than treating a red chart as a discount label.

Also separate trading risk from investment risk. A short bounce trade may depend on liquidity and timing. A longer hold needs supply clarity, product demand, and a reason future buyers will still care after the first reward cycle ends.

If you cannot answer who may sell next, do not pretend the dip is simple. You may still choose to trade it, but at least know which door the next seller is walking through.

If you are caught in a post-TGE selloff, slow down and classify the problem before acting. Panic trades often turn one bad entry into two bad decisions.

Start with your original thesis. If you bought because the token had product traction, check whether that evidence still exists. If you bought because the chart was green and everyone sounded euphoric, be honest. That was momentum, not a thesis.

Then check the position itself. A small speculative position and an oversized position need different handling. The token may be risky, but the larger problem may be that the size is now driving your thinking.

Use this five-step triage:

Avoid turning the loss into an identity. The path toward bagholder risk usually starts when someone replaces new evidence with hope. Holding can be rational, but only if the reason is still alive and the position size is survivable.

Tax context, opportunity cost, and security risk can also matter. A token that is down but liquid is different from a token with blocked selling, unclear contracts, or suspicious wallet movement. Safety comes before revenge trading.

Do not force a sell, hold, or buy-more answer from one candle. Use the checklist to make the decision less emotional. Name the risk, update the thesis, size the exposure, and stop letting the launch candle write the whole plan.

Post-TGE selloff examples are useful when they show patterns, not when they become stale price recaps. The names change every cycle, but the mechanics repeat with eerie commitment.

Lighter is a clean recent example of airdrop-related outflows after launch. CoinDesk reported that about $250 million was withdrawn from the platform within 24 hours of its LIT airdrop. Expert comments pointed to farmers and early participants rotating after TGE.

Solstice and Plasma-style examples show another pattern: a visible launch-day drop can mix claim selling, high expectations, low liquidity, and broader market conditions. The headline price move is obvious. The cause needs more work.

Compare examples by pattern, not by token name:

| Pattern | What to Compare Before Reacting |

|---|---|

| Farmer Exit | Was the user base mainly reward hunters or real repeat users? |

| Claim-Window Pressure | Are claims still opening in waves or mostly complete? |

| High-FDV Repricing | Was the launch valuation already too rich for demand? |

| Weak Price, Real Usage | Are users still active after rewards become liquid? |

| Better Launch Design | Did the project limit free-bag dumping or align incentives? |

Blast, Berachain, MegaETH, Katana, Rujira, and similar community examples all get discussed through this lens. Some debates focus on whether fully tradable airdrops create instant sell pressure. Others focus on whether reward design can reduce free-bag exits.

The lesson is not that one model always wins. It is that launch design decides who gets liquid first, who waits, and who absorbs the first wave of selling. That is the post-TGE selloff story in miniature.

Related post-TGE selloff terms are useful only when they sharpen the diagnosis. Start with the selling cohort. Jeets are quick sellers or early exiters, often blamed when a launch candle fades. The word is common in crypto chat, but it is not proof of bad faith. It tells you to ask whether the project made fast selling predictable through free claims, weak lockups, or reward-farmer incentives.

Then separate normal market pressure from abuse. A hard rug means sellability, liquidity, contract control, or project access breaks in a much more direct way. That is different from a token falling because claimants took profit. Calling every post-TGE selloff a rug can hide the real issue: poor launch design, weak demand, or upcoming supply.

Other nearby labels still matter, but use them after the mechanics are clear. Bagholder risk describes the holder outcome. Soft-rug drift describes slow abandonment. Top-signal and bottom-signal language describes chart context, not project intent. Airdrop farming explains why wallets may leave quickly after rewards become liquid.

That order keeps the diagnosis honest because the same red candle can come from very different causes. Fast sellers with clear supply data point to one problem. Opaque wallet movement, vague allocation updates, and broken market access point to another. Start with supply, liquidity, and incentives, then choose the label. Otherwise every red candle becomes courtroom drama.

After a post-TGE selloff, start by finding the next source of sellable supply. The chart is already telling you pressure exists, so the useful work is figuring out whether more pressure is waiting.

Run the checks in a calm order:

The checks should change the next action. If the next seller cohort is known and liquidity is thin, a bounce can fail even when the price looks washed out. If claim activity is mostly finished and product use still exists, the selloff is easier to classify as price discovery.

Then decide what kind of decision you are making. A dip trade needs timing, depth, and a clear invalidation point. A longer hold needs a stronger thesis and enough patience to survive future releases.

Avoid sizing a bounce trade before the first sell waves are understood. New-token charts can punish certainty fast, especially when the first visible price was built on thin liquidity and heavy launch attention.

If the token has clear supply data, working markets, active users, and slowing sell pressure, the selloff may be part of price discovery. If supply is vague, insiders are moving, communication is weak, and every rebound gets sold, caution belongs in the room.

The goal is not to predict the perfect low. It is to stop reacting to the first red chart and start asking whether the next wave of supply has already been priced in. That is where a post-TGE selloff becomes readable instead of just loud.

A post-TGE selloff means a token falls after its token generation event, usually because newly claimable or tradable supply hits the market before steady demand forms.

It often happens around airdrops, launchpad sales, exchange listings, and points-program tokens. The phrase does not prove fraud by itself. It tells you to inspect seller incentives, liquidity, and the supply schedule.

No, a post-TGE selloff is not always a bad sign. Some selloffs are normal price discovery after free or discounted tokens become liquid.

It becomes more concerning when allocations are vague, liquidity is thin, team communication fades, or wallet movement suggests better-positioned sellers are leaving while public buyers absorb the pressure.

Airdrop farmers can cause post-TGE selling pressure because many joined the campaign to earn rewards, not to hold the token long term.

Once the claim opens, they may sell to lock in value and move capital to the next campaign. That behavior can be rational, but it still creates immediate supply for the market to absorb.

A post-TGE selloff is not the same as a rug pull. A selloff can happen in a working market when claimants, farmers, or early buyers sell.

A rug pull involves stronger abuse signals, such as removed liquidity, blocked selling, malicious contract changes, hidden insider exits, or a project disappearing. Do not blur the terms without evidence.

Yes, a token can recover after a post-TGE selloff if selling pressure slows and real demand appears. Recovery needs more than a lower price.

Look for completed claim waves, stable liquidity, transparent supply updates, active users, and fewer forced sellers. If future releases are large and demand stays weak, the selloff can continue instead.

Before buying after a post-TGE selloff, check the claim status, circulating supply, FDV, liquidity depth, holder concentration, next release date, and project activity.

Then ask who may sell next and why new buyers would absorb that supply. If the answer is only “because it already dumped,” the trade is still leaning on hope.