Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Real yield explained with revenue, APY, and risk checks.

Real yield is crypto yield backed by actual fees, lending interest, or cash flow instead of mainly new token incentives.

The phrase sounds comforting, but it is only the start of the work. A real yield claim still needs a source, a payout route, a net-return check, and an exit plan.

Otherwise, it is just APY wearing a cleaner shirt.

Real yield in crypto means a return funded by economic activity. That activity may be trading fees, borrowing interest, liquidation fees, staking rewards, MEV capture, reserve income, or another traceable cash-flow source.

The opposite is yield funded mainly by newly issued tokens, points, or temporary subsidies. Those rewards can still have value. But until revenue can support the payout, they are closer to marketing spend.

The payout asset can be a clue. Rewards paid in ETH, USDC, BTC, or another liquid asset often look more credible than a freshly printed farm token. But the asset alone does not prove the source. A project can pay stablecoins from a treasury campaign. A protocol can also pay its own token from real fees.

So the useful question is simple: who paid for this return?

If traders paid fees, borrowers paid interest, validators earned rewards, or users paid for a service, the yield may have a real source. If the main source is inflation, referral rewards, points, or a grant budget, the yield may be temporary even when the number looks fantastic.

Crypto usage also differs from traditional finance. In bond markets, real yield often means yield after inflation. In DeFi, real yield usually means revenue-backed or cash-flow-backed yield. Same phrase, different job.

Real yield works best as a source test, not a safety label. It helps you separate earned returns from subsidized returns. It does not make a strategy safe, fixed, liquid, or profitable.

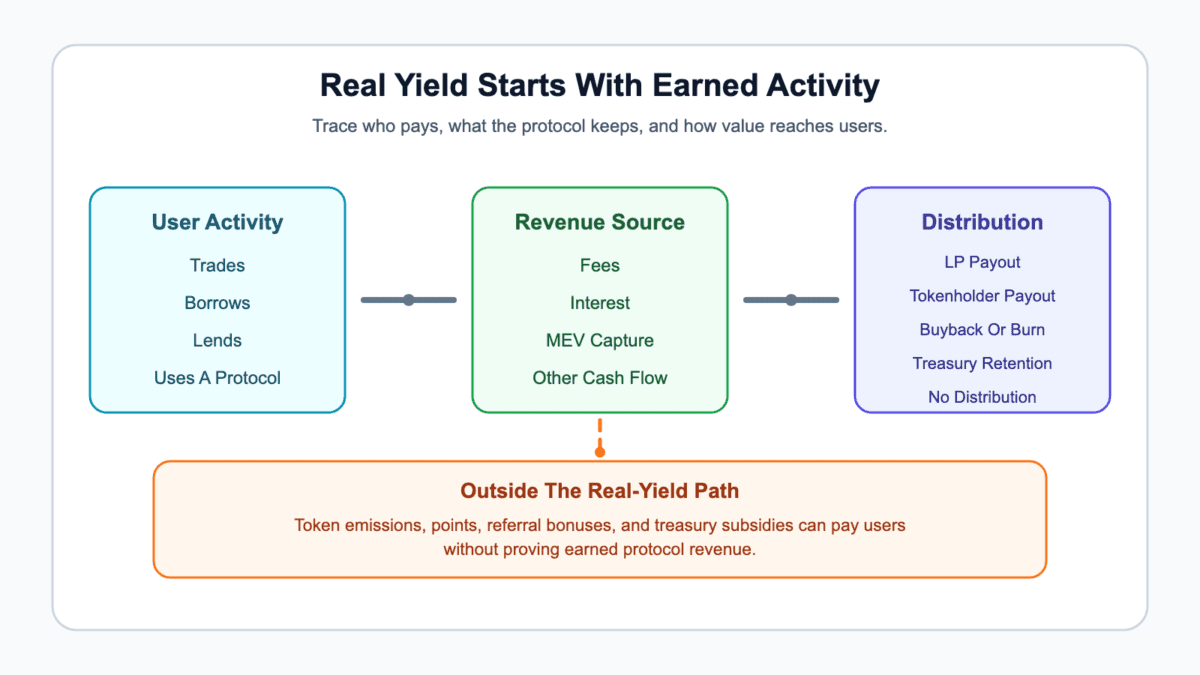

Real yield in DeFi starts with user activity. Someone trades, borrows, lends, mints, redeems, stakes, bridges, or uses an onchain service. The protocol collects a fee, spread, interest payment, reward, or another revenue stream tied to that activity.

Then the protocol decides where that value goes. It may pay liquidity providers, stakers, tokenholders, validators, vault depositors, a treasury, or nobody outside the protocol. Some designs use revenue for buybacks or burns instead.

That is why revenue language can get confusing fast. Total fees are usually what users pay. Supply-side fees are the part paid to liquidity providers or depositors. Protocol revenue is what the protocol keeps after supplier payouts. Token-holder revenue is what returns to tokenholders through payouts, burns, buybacks, or staking-style distributions.

A useful starting point is DefiLlama’s fees dashboard, because it separates user fees, revenue, supply-side fees, and token-holder revenue instead of collapsing everything into one APY box. When accessed on June 21, 2026, its live dataset tracked 2,299 protocols and about $1.66 billion in total fees over the previous 30 days.

The route matters more than the label. A DEX may generate high trading fees, but most of those fees may go to liquidity providers. A lending market may show steady interest, but borrower demand can fade. A governance token may claim value capture while the fee switch stays off or waits on a DAO vote.

The cleanest DeFi yield story has a visible trail. You can name who pays, why they pay, which contract or treasury receives funds, which asset pays users, and which rule moves the value.

If that trail breaks, pause. A protocol can still be legitimate, but the “real yield” claim has not proved much yet.

Real yield and token emissions can both pay users, but they prove different things. Real yield points to earned activity. Token emissions point to newly distributed supply, usually meant to attract users, liquidity, or attention.

That does not make emissions worthless. Early protocols often use liquidity mining to bootstrap markets. A new lending pool may need deposits before borrowers arrive. A new exchange may need makers before takers show up. Incentives can start that loop.

The problem starts when emissions become the main return. If a yield depends on constant token issuance, APY can fall when rewards slow, token price drops, or users leave after the campaign ends. That is why yield farming needs a source check before a rate comparison.

Use this split before comparing two APYs:

| Yield Source | What To Check |

|---|---|

| Trading fees | Is volume real, repeatable, and paid by users? |

| Lending interest | Is borrow demand strong without unsafe collateral stress? |

| Token emissions | Who gets diluted, and when do rewards slow? |

| Points | Who controls conversion, and is there any promised value? |

| Treasury subsidy | How long can the budget support the payout? |

| Referral or campaign rewards | Does the return survive when the campaign ends? |

The table is not a ranking. It is a way to stop comparing every APY as if it came from the same engine.

Farm rewards can be useful while a protocol grows. They can also hide weak demand. If revenue later replaces emissions, the program may mature. If emissions only attract mercenary deposits, the yield can vanish once the subsidy gets dull.

Real yield is not morally superior by default. It is just easier to inspect. You can ask who paid, how often they pay, and whether the payout survives when the marketing budget gets cut.

Real yield in practice comes from several different sources, and each source can shrink in a different way. That is why lists of “real yield coins” can mislead. The token name matters less than the mechanism behind the return.

DEX trading fees are the classic example. Users swap tokens, pay fees, and some of those fees may flow to liquidity providers or a protocol treasury. But impermanent loss, gas, or weak exits can still wipe out gross fees.

Perpetual exchanges can generate real yield through trading fees, funding-related mechanics, liquidation fees, or vault activity. GMX, Hyperliquid-style vaults, and similar designs often appear in real yield discussions because volume can be tied to fee streams. The first check is whether the vault or tokenholder actually receives that flow.

Lending markets such as Aave-style protocols can generate yield from borrower interest. That source is easier to understand than points, but it is not fixed. Borrow demand changes, collateral quality changes, and liquidations can turn a calm pool into a stress test.

Several sources show up across DeFi:

| Source | What Can Make It Shrink |

|---|---|

| DEX fees | Lower volume, thinner liquidity, or LP losses. |

| Perp fees | Lower trading activity or trader losses hitting vaults. |

| Lending interest | Weak borrow demand or collateral stress. |

| MEV capture | Lower opportunity, validator changes, or routing changes. |

| Staking rewards | Lower network rewards, slashing, or validator costs. |

| RWA cash flow | Custody, reporting, redemption, or issuer risk. |

Real-world assets add another layer. Treasury bill income, private credit, invoices, or tokenized funds can produce offchain cash flow that reaches onchain users. That can count as real yield when the legal claim, custody path, reporting, and redemption rules are clear.

But an RWA label is not a magic wand. It can also mean TradFi risk with crypto wrappers, delayed redemptions, and opaque custody. The same rule applies: find the payer, find the route, then find the exit.

To check whether real yield is real, trace the return before funds move. Start with the source. Then compare the payout against what the protocol actually earns.

First, identify the paying activity. A yield claim should connect to fees, interest, staking rewards, reserve income, liquidation fees, MEV, or another explainable flow. If the answer is only “community incentives” or “protocol rewards,” keep digging.

Then compare revenue to distributions. A protocol that earns $1 and pays $5 is using another funding source for the difference. That extra source may be emissions, a treasury budget, venture incentives, or a short campaign.

Use this checklist before trusting the label:

The farm rewards label needs special care because it can cover fees, incentives, points, emissions, or a mix of all four. Do not let one familiar word do too much work.

TVL is useful, but it can grow for the wrong reason. Deposits may rise because incentives are high, not because the protocol has durable demand. When the rewards slow, TVL can leave faster than a group chat after an ugly supply release.

Net return is the final check. A real fee source can still lose money after gas, price impact, impermanent loss, withdrawal fees, token price drops, taxes, and bridge costs. Real yield explains where the money comes from. It does not promise what stays in your wallet.

Real yield risks start with the activity that funds the return. If a perp exchange has less volume, fees fall. If a lending market has fewer borrowers, interest falls. If a DEX pool gets less flow, LP fees fall.

APY often changes after conditions have already moved. A dashboard can show yesterday’s annualized rate while today’s exit is crowded, expensive, or delayed. That lag is where users get caught.

The biggest risk is mistaking “real” for safe. Real yield can still sit behind smart contracts, governance votes, vault strategies, bridges, custody routes, oracle feeds, liquidation engines, and withdrawal queues. Each layer can fail in its own way.

Exit risk is the one users often notice too late. A strategy can earn real fees for months, then become painful when too many deposits try to leave through the same narrow door. That is where exit liquidity turns from slang into portfolio math.

Watch these weak spots before chasing the headline rate:

There is also a slower failure path. A protocol may start with clear revenue, then lean harder on vague incentives, changing promises, and new reward layers as growth slows. That pattern can look like soft rug risk when the story degrades without one dramatic rug-pull moment.

The boring warning is also the useful one: if the strategy cannot explain what breaks first, it is not ready for serious money. The APY box is the advertisement. The risk path is the bill.

Real yield examples help only when they show a mechanism. They lose value when they turn into a ranked list of tokens with fast-changing APYs.

Fee-sharing perp designs are one bucket. Users trade, the protocol collects fees, and some value may flow to liquidity providers, vault depositors, stakers, tokenholders, a buyback program, or the treasury. The first question is who absorbs trader losses and volatility.

Lending markets are another bucket. Borrowers pay interest, and depositors may receive a supply rate. The first question is whether borrow demand is organic or temporarily boosted by incentives.

DEX fee routing can be real yield for LPs when trading fees outweigh losses and costs. It can also become poor net yield when pool composition moves against the LP. High volume is helpful, but it does not cancel impermanent loss.

Liquid staking, restaking, vaults, and RWAs each need their own first check:

| Example Type | First Question To Ask |

|---|---|

| Liquid staking | What earns the reward, and what slashing or liquidity risk exists? |

| Restaking | Is the extra reward paid by real service demand or incentives? |

| Vaults | What strategy earns the yield, and who controls changes? |

| RWAs | What legal claim, custodian, and redemption path support the cash flow? |

| Fee switches | Is the switch active, and who receives the value? |

Use protocol names as examples, not endorsements. GMX can illustrate perp fees. Aave can illustrate lending interest. Curve can illustrate fee routing. Lido can illustrate staking rewards. Pendle can illustrate yield markets. Morpho can illustrate lending vaults. None of that makes a current APY attractive by itself.

Group examples by source. If two products both say real yield but one depends on trading fees and another depends on offchain Treasury income, they are not the same risk.

Real yield research fits most crypto users because it improves APY reading. Even if you never deposit into a vault, the concept helps you spot the difference between earned returns, token inflation, points, and campaign rewards.

Putting money into real-yield strategies is different. That brings wallet setup, contract approvals, transaction fees, tax records, withdrawal rules, and custody choices. A clean yield source can still be a bad fit if the route is too complex for the amount at risk.

For small accounts, fees and tax cleanup can matter as much as the headline rate.

Beginners should separate learning from acting. Learning real yield means reading the source and asking better questions. Acting on real yield means signing transactions, accepting smart contract risk, and tracking exits.

Wallet hygiene belongs in that second category. If a strategy requires approvals, bridges, or vault shares, the user needs a careful wallet setup before yield research turns into live exposure.

Real yield can fit users who want to compare DeFi products more carefully, understand protocol revenue, or avoid obvious incentive traps. It fits less well when a user cannot explain the route, cannot afford a lockup, or only wants the highest displayed APY.

The best use is defensive before it is profitable. Real yield helps you reject weak claims faster. That alone can save more than a slightly better rate on a strategy you did not understand.

Start real yield research with the funding source, not the APY. A rate is only useful after you know who pays it and why that payer keeps showing up.

Keep the research small at first. One protocol, one yield source, one exit route. If the path already feels foggy at that size, adding more dashboards will not make the risk clearer.

Use a short process before any deposit, stake, or vault move:

Then write down the first failure point. For a lending pool, it may be borrower demand. For a DEX LP position, it may be impermanent loss. For a perp vault, it may be trader PnL and withdrawal queues. For an RWA product, it may be custody or redemption.

Also write down the boring numbers. Expected net return, gas, entry cost, withdrawal cost, tax record needs, and the time you may be locked in all belong beside the advertised APY. If those costs make the return look ordinary, the strategy may still be fine. It just stopped being magical.

Sizing comes after understanding. If the yield path makes sense only after three dashboards, two Discord threads, and a heroic amount of optimism, reduce the size or skip it.

Real yield should make a strategy easier to explain, not harder. If nobody can say who pays the return, the yield has not earned your money.

Real yield in crypto is yield funded by actual economic activity such as fees, lending interest, staking rewards, or cash flow. It is different from rewards funded mainly by new token emissions, points, or temporary subsidies.

Real yield is not the same as yield farming because yield farming describes an activity, while real yield describes the source of the return. A farm can include real yield, emissions, points, or a mix of incentives.

You calculate real yield by comparing earned revenue with the amount distributed to users, then subtracting costs and risks that affect net return. The source should be visible before the APY gets attention.

Real yield is not always safer than token emissions because fee-backed yield can still fall, contracts can fail, and exits can become crowded. It is easier to inspect, but it is not guaranteed.

Staking can be real yield when rewards come from network activity, validator rewards, or another real economic source. It becomes less clear when extra APY comes mainly from incentive tokens or promotional boosts.

Real yield does not guarantee profit. A strategy can earn real fees while the user loses money to price drops, impermanent loss, gas, taxes, slippage, lockups, or a bad exit.