Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Understand impermanent loss before chasing LP yield.

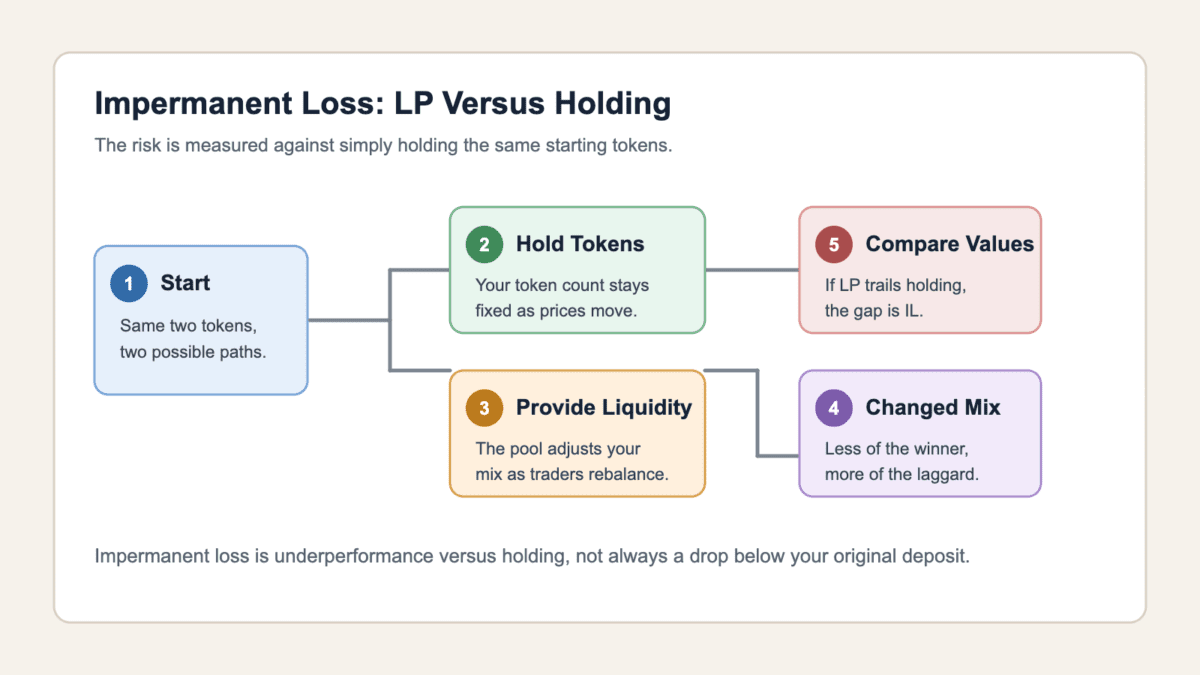

Impermanent loss is the gap between a liquidity pool position and simply holding the same starting crypto assets.

The word “impermanent” does too much work. The loss can shrink if token prices return to the old ratio, but it becomes real when you withdraw while the pool’s token mix is still changed.

That is why high LP APY needs a second look. A pool can pay fees and rewards while your position still trails a boring hold-only wallet. Not glamorous. Often useful.

Impermanent loss in crypto means your liquidity pool position is worth less than the same tokens would be worth if you had simply held them. The comparison is against holding, not only against your original deposit value.

That distinction fixes the biggest beginner mistake. If you deposit ETH and a stablecoin into a pool, then ETH rallies, your LP position may still rise in dollar value. You may feel richer. The impermanent loss is the missing upside versus holding the original ETH and stablecoin outside the pool.

The core comparison is simple:

The term is awkward because the loss is only “impermanent” while the relative prices can still return to the deposit ratio. If they do, the gap can close. If you withdraw while the ratio is still different, the underperformance is locked into the assets you receive.

So impermanent loss is not the pool stealing tokens. It is the tradeoff you accept for acting as liquidity. You earn fees by letting traders use your assets, but the pool may leave you with less of the token that outperformed and more of the token that lagged.

Impermanent loss is one possible reason an LP result looks worse than expected. It is not the only one. A bad pool result can also come from token price drops, weak volume, fees, slippage, reward-token dumps, depegs, or outright failure.

Start by diagnosing the loss before blaming the formula. A user who receives fewer dollars after withdrawal may have suffered regular market loss, impermanent loss, or both. A user who is up in dollars may still have impermanent loss if holding would have paid more.

Use this quick split before you touch a calculator:

| What Happened | How To Recognize It |

|---|---|

| Impermanent loss | Your LP value trails the hold-only value for the same starting tokens. |

| Regular token price loss | One or both assets fell, and holding them would also be down. |

| Fee drag | Trading, withdrawal, gas, or platform costs reduced the final result. |

| Slippage | Entry or exit execution moved against you because liquidity was thin. |

| Reward-token dump | Incentives looked rich, then the reward token fell hard. |

| Depeg risk | A stablecoin or wrapped asset stopped tracking its expected value. |

| Exploit or rug loss | Contract control, liquidity removal, or project failure damaged the pool. |

The rug row is separate on purpose. A hard rug is not impermanent loss with a nastier haircut. It is a failure or malicious exit pattern where liquidity, contract controls, or team behavior breaks trust quickly.

The practical check is the hold-only comparison. Rebuild what your wallet would have held if you had never provided liquidity. Then compare that value with your LP withdrawal value, after costs and rewards. That gives you the cleanest view of whether impermanent loss was the main drag.

Impermanent loss happens because an automated market maker changes your token mix as prices move. In a basic 50/50 pool, the pool must keep the two assets balanced by value under its pricing formula.

Imagine a pool with ETH and USDC. When ETH rises on outside markets, the pool does not magically update itself. Traders and arbitrageurs buy the underpriced ETH from the pool until the pool price lines up with the broader market.

That trading changes the pool balances. The pool now has less ETH and more USDC. As a liquidity provider, your share of the pool reflects that new mix.

Here is the user-facing result:

This is not a glitch. It is how many AMM pools quote prices and supply liquidity without an order book. LPs provide the inventory. Traders use it. Arbitrage keeps the pool price aligned with outside markets.

The subtle part is that arbitrage also explains why LPs can underperform. The market pays arbitrageurs to rebalance the pool. LPs earn fees for supplying depth, but they also absorb the structural effect of that rebalancing. A calm interface can hide a very active market-making job.

An impermanent loss example works best when the LP still makes money. That shows the real issue: the pool position can rise while still losing to the hold-only alternative.

Suppose you start with 1 ETH worth 1,000 USDC and another 1,000 USDC. You could hold those assets, or you could provide them to a 50/50 ETH/USDC pool. Now suppose ETH doubles to 2,000 USDC before fees.

The simplified comparison looks like this:

| Hold-Only Outcome | LP Outcome |

|---|---|

| You still hold 1 ETH and 1,000 USDC. | The pool gives you less ETH and more USDC. |

| At 2,000 USDC per ETH, the wallet is worth 3,000 USDC. | The LP position is worth about 2,828 USDC before fees. |

| You captured all of ETH’s upside on the original 1 ETH. | You earned pool exposure, but sold some ETH through rebalancing. |

| No LP fees or rewards are included. | Fees and rewards may reduce or offset the gap. |

A common 50/50 Chainlink example puts that 2x price-move gap near 5.7 percent versus holding, before fees. In that same worked example, the hold-only result beats the LP withdrawal by 171.6 USDC. The LP is still up from the original 2,000 USDC deposit. It is just behind the 3,000 USDC hold-only outcome.

That is the part high-yield dashboards can blur. A green position is not proof that LPing beat holding. You need both numbers: the LP value and the hold-only value. Without that comparison, you are only checking whether the pool made money, not whether the pool was the better use of the assets.

You calculate impermanent loss by comparing the value of the LP position with the value of simply holding the deposited tokens. For a basic 50/50 pool, the common formula uses the relative price change between the two assets.

The usual formula is:

IL = 2 * sqrt(price ratio) / (1 + price ratio) - 1

The price ratio is the new relative price divided by the starting relative price. If one token doubles against the other, the ratio is 2. If it falls by half, the ratio is 0.5. In a symmetric 50/50 pool, both directions create the same percentage underperformance versus holding.

Use that ratio for the pair, not only for one token’s dollar chart. In ETH/USDC, the move often feels obvious because USDC is the reference point. In two volatile assets, both tokens can move at once, so the relative move between them drives the estimate.

Rounded examples help more than staring at the formula:

| Price Ratio Change | Approx Impermanent Loss |

|---|---|

| 1.25x | 0.6% |

| 1.5x | 2.0% |

| 2x | 5.7% |

| 3x | 13.4% |

| 5x | 25.5% |

Those numbers are before trading fees, rewards, gas, taxes, and pool-specific design. They are also for a basic 50/50 constant-product pool.

Keep the estimate separate from the trade result. A calculator can show 5.7 percent impermanent loss while the LP is still profitable after fees. It can also show a small percentage while both tokens are down in dollar terms. The formula answers the hold-only comparison. It does not tell you whether the whole position was smart.

The formula gets less tidy when the pool is not a simple 50/50 design. Weighted pools, stable-swap pools, concentrated-liquidity ranges, dynamic fees, automated vaults, and single-sided products can all change the math. Use the formula as a starting point, not a full profit and loss statement.

An impermanent loss calculator usually isolates price divergence. That is useful, but it is not the same as real LP profit.

Many calculators ask for starting prices, ending prices, and token weights. Some add APY fields. Fewer capture all the messy details that decide what actually lands in your wallet after you exit.

That makes them good for one question and weak for the bigger one. They can estimate the pool’s structural drag, but they cannot know your exact entry timing, gas bill, reward-claim behavior, records burden, or whether you will exit a range after a fast move.

Check what the calculator excludes before trusting the result:

That missing context is why “legit APR” is harder than a dashboard number. A pool may show strong rewards while the reward token falls, gas eats small accounts, or the LP range moves out of position.

For smaller accounts, those omissions can dominate the theoretical number. A high gas bill, one bad exit trade, or a reward token that fades quickly can outweigh a neat calculator estimate.

Run scenarios instead. Check a mild move, a sharp rally, a selloff, and a sideways case. Then add realistic fees, rewards, and costs. If the pool only looks good under one perfect path, the APY is doing a little theater.

Impermanent loss becomes permanent when you withdraw while the token-price ratio is still different from when you deposited. At that point, the changed token mix leaves the pool and becomes your actual wallet balance.

Waiting can help only if the relative prices move back toward the starting ratio. It does not help because time passed. It helps because the price relationship changed in your favor.

Two users can see the same impermanent loss estimate and make different calls. One may wait because they still want both assets and expect the pair to move back together. Another may exit because the pool has become a worse position than holding, even if that realizes the underperformance.

Your main choices usually look like this:

Concentrated liquidity makes this more active. Moving a range, resetting a vault, or changing exposure can turn a paper gap into a realized trade path. The screen may still call it an LP position, but the economics have shifted.

Rebalancing deserves care because it can disguise the exit. Moving from one range to another is still a new exposure choice. If the old range left you mostly in one asset, resetting the position may confirm that inventory shift.

Ask a narrower question before waiting: what relative price path would close the gap, and am I willing to wait for it? If the answer depends on wishful chart yoga, write that down before adding more funds.

Fees can offset impermanent loss when trading volume and rewards are large enough to beat the underperformance gap. They can also fail to offset it when price divergence is sharp, volume dries up, or rewards lose value.

That is why displayed APY is not net profit. The number may include trading fees, token incentives, boosted rewards, or short-term campaigns. It may not include the price path that created impermanent loss.

Fee math starts with actual volume, not headline liquidity. A pool can have plenty of capital parked and still produce thin fees if few traders use it. A smaller pool with real turnover may pay more, although it can also bring more slippage and execution risk.

Several inputs decide whether fees have a real chance:

Count rewards separately from fees. Trading fees come from activity in the pool. Incentive tokens come from a program that can slow, end, or dump. Mixing them together can make a shaky APY look cleaner than it is.

Liquidity incentives often sit beside farming rewards, where protocols pay users to supply capital or perform activity. That can help LP returns, but it can also attract short-term capital that leaves when rewards slow.

So the question is not “does the pool pay fees?” Most do. The question is whether the pool pays enough after impermanent loss, costs, and reward-token risk. A big APY on a weak pair can be a coupon attached to a trapdoor.

You reduce impermanent loss risk by choosing pools where relative prices are less likely to diverge sharply, then sizing the position so a bad path does not wreck the account. You cannot remove the risk from standard AMM liquidity.

Correlated pairs usually carry lower impermanent loss risk. Stablecoin pairs, ETH/stETH-style pairs, and wrapped-asset pairs can move together more closely than ETH paired with a small volatile token. But lower price-divergence risk does not mean low total risk.

Useful risk reducers include:

> A stablecoin pool can still suffer depeg, bridge, platform, or smart-contract risk. Boring assets can still find creative ways to become exciting at the worst time.

Be especially careful with new-token pools that advertise rich incentives and thin real demand. High rewards can mask weak buyers, insider supply, or a setup where later LPs become new-token exit liquidity for earlier sellers.

The practical goal is risk reduction, not risk deletion. If both tokens are assets you would happily own, the pool has real trading demand, and the fee path can beat several downside scenarios, impermanent loss becomes a tradeoff you can evaluate instead of a surprise bill.

Impermanent loss in concentrated liquidity pools can feel sharper because your capital sits inside a chosen price range. You may earn more fees while price trades inside the range, but you also take more active range risk.

Uniswap v3, CLMMs, DLMMs, and automated LP vaults all push users toward range decisions. A narrow range can improve fee density. It can also leave you out of range, heavily tilted toward one asset, or forced to rebalance after a fast move.

Picture an ETH/USDC position with a tight range around the current price. If ETH rallies above the range, your position may end up mostly in USDC. If ETH sells below the range, it may end up mostly in ETH. The position did not explode. It changed inventory.

Concentrated liquidity adds several questions:

Advanced LPing can become PvP DeFi markets rather than passive income. Better tools, faster rebalancing, lower costs, and sharper range selection can give skilled users an edge.

Automation helps, but it does not make the risk vanish. A vault may rebalance efficiently while still locking in changes you would not have chosen manually. Read the strategy as market making with rules, not a magic box that turns volatility into rent.

Impermanent loss belongs to liquidity provision, not every DeFi yield strategy. Staking, lending, and holding have different return sources and different failure paths.

This comparison helps beginners decide whether LPing is the right first DeFi step. LPing can earn trading fees and rewards, but it asks you to accept changing token balances. Staking, lending, and holding each keep a different risk profile.

Use the table to separate the strategies:

| Strategy | Main Risk To Understand |

|---|---|

| Holding | You keep the asset mix, but you take full price exposure. |

| Staking | You earn protocol rewards, but face validator, lockup, slashing, or issuer risk. |

| Lending | You earn borrow demand, but face collateral, liquidation, platform, and rate risk. |

| Liquidity provision | You earn fees or incentives, but face impermanent loss and pool design risk. |

| Concentrated liquidity | You may earn denser fees, but range and rebalancing choices become active risks. |

LPing is often presented as passive income. That is only partly true. A basic stable pair may require light monitoring. A volatile concentrated-liquidity position can behave like active market making with a friendly interface and a sharp edge.

If you mainly want exposure to one token, holding may fit better. If you want protocol participation, staking may be cleaner. If you want yield from borrower demand, lending has its own checklist. If you want fees from trading activity and accept inventory drift, LPing becomes worth studying.

Before you provide liquidity with impermanent loss risk, decide whether you would still want both assets after the pool changes your mix. If you only like one side, the pool can quietly move you into the side you dislike.

Then test the pool like a position, not a coupon. The APY is one input. Pair quality, volume, fee tier, reward source, contract risk, wallet permissions, range plan, and exit plan all shape the outcome.

Also decide what would make the pool wrong. A deposit plan without an exit rule is just a yield dashboard doing the thinking for you. If the token pair, fee tier, or reward program changes, you need to know whether you wait, rebalance, or leave.

Run this checklist before depositing:

Wallet hygiene deserves its own line. LP tools may ask for approvals, contract interactions, and position-management permissions. Keep wallet permissions tidy, especially if you try several pools, chains, or vault interfaces.

Do the checklist in writing if the position is meaningful. The point is not ceremony. It forces the pool to beat the boring alternative before the APY starts negotiating.

Start smaller than the dashboard tempts you to start. If the position is confusing at $100, it will not become clearer at $10,000. It will only become louder.

Impermanent loss sits near several DeFi concepts, but mixing them together makes the LP decision fuzzy. Farming explains why protocols may pay extra incentives on top of fees. That helps when rewards have real demand, and misleads when the reward token is the thing being unloaded.

Exit liquidity traps are useful context for new-token pools with huge rewards and thin buyers. The point is not that every LP pool is predatory. It is that incentive-heavy pools can move risk from early sellers to later capital providers.

Competitive LP dynamics are the third idea to keep separate. Better tools, faster rebalancing, and lower costs can give advanced LPs an edge, especially in concentrated ranges. That does not make simple pools useless. It just means passive-income framing deserves a raised eyebrow.

Impermanent loss is the gap between what your liquidity pool position is worth and what the same starting tokens would be worth if you held them. It usually appears after the two assets move to a different price ratio.

Impermanent loss is a real underperformance versus holding. It becomes realized when you withdraw while the token ratio is still different from your deposit ratio. Before withdrawal, the gap can shrink if relative prices move back.

Yes. Impermanent loss can happen when prices go up because the comparison is against holding. If one token rises sharply, the pool may leave you with less of that outperforming token than a hold-only wallet would have kept.

You usually reduce impermanent loss rather than avoid it completely. Correlated assets, stable pairs, wider ranges, careful sizing, strong volume, and realistic fee assumptions can help, but every pool still has its own tradeoffs.

Impermanent loss can happen in stablecoin pools, but it is usually smaller when both pegs hold. The bigger danger may be depeg risk, bridge risk, platform risk, smart-contract risk, or rewards that fade after incentives slow.

Liquidity providing can be worth it when fees, incentives, and pool quality beat the hold-only outcome after costs. It is weaker when APY depends on volatile rewards, thin demand, narrow ranges, or assets you would not want to hold.

Start with the hold-only comparison. Before entering a pool, write down the value of the tokens you would hold outside the pool. That becomes your baseline.

If the pool is ETH/USDC, that baseline is simple. If it is two volatile tokens, write down both token counts and the starting price ratio. You are preserving the comparison, not predicting the chart.

Then use an impermanent loss calculator for several price paths. Test a rally, a selloff, and a sideways case. Add fees, rewards, gas, slippage, and any range-management costs by hand.

Keep the numbers conservative. Use realistic costs and assume rewards may be worth less by the time you claim them. A scenario that needs perfect timing, zero costs, and a friendly reward token is not a plan. It is a brochure.

Use a short action list before you deposit:

Then decide how often you will check the position. Simple pools may need occasional review. Concentrated ranges, vaults, and volatile pairs need more attention because the pool can drift into very different exposure.

The quiet rule is the best one: if a pool only looks good because the APY is huge, slow down. Good liquidity positions survive basic questions. Bad ones need you dazzled.