Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Understand LSTfi before chasing extra staking yield.

LSTfi is the use of liquid staking tokens in DeFi strategies, usually to keep staking exposure while adding lending, borrowing, liquidity, yield-token, collateral, or restaking-adjacent use cases.

That can make staked capital more flexible. But it also stacks risks that plain staking does not carry: token design, issuer controls, smart contracts, liquidity depth, oracle pricing, liquidation rules, bridges, wallets, and taxes.

Ask what the token represents, where the extra yield comes from, and whether you can leave cleanly when the dashboard stops looking polite.

LSTfi in crypto means liquid staking token finance. It describes DeFi activity that uses liquid staking tokens, not a single asset, app, or guaranteed passive-income product.

The acronym usually appears after someone already understands staking. A user stakes a proof-of-stake asset, receives a liquid staking token, then uses that token somewhere else. LSTfi is the “somewhere else” part.

For receipt-token mechanics, the SEC’s 2025 liquid staking statement helps draw the line. It treats liquid staking receipt tokens separately from later crypto-app use. That split is the core of LSTfi: the staking receipt exists first, and DeFi strategies around that receipt come after.

Common examples include stETH, rETH, eETH, weETH, JitoSOL, and mSOL. Those names are not endorsements. They simply show the kinds of wallet assets that can move into lending markets, liquidity pools, collateral systems, fixed-yield markets, or other DeFi routes.

The mistake to avoid is reading “LSTfi” like a ticker. There may be tokens with similar letters, but the category is broader than any one coin. LSTfi is closer to “DeFi around LSTs” than “buy this asset.”

That distinction keeps the risk discussion honest. If you buy a token, price action may be the main issue. If you use an LST inside DeFi, the position may depend on staking rewards, issuer redemption, smart contracts, market depth, collateral settings, and your own wallet approvals.

The clean LSTfi meaning is simple. The harder job is checking the stack underneath it.

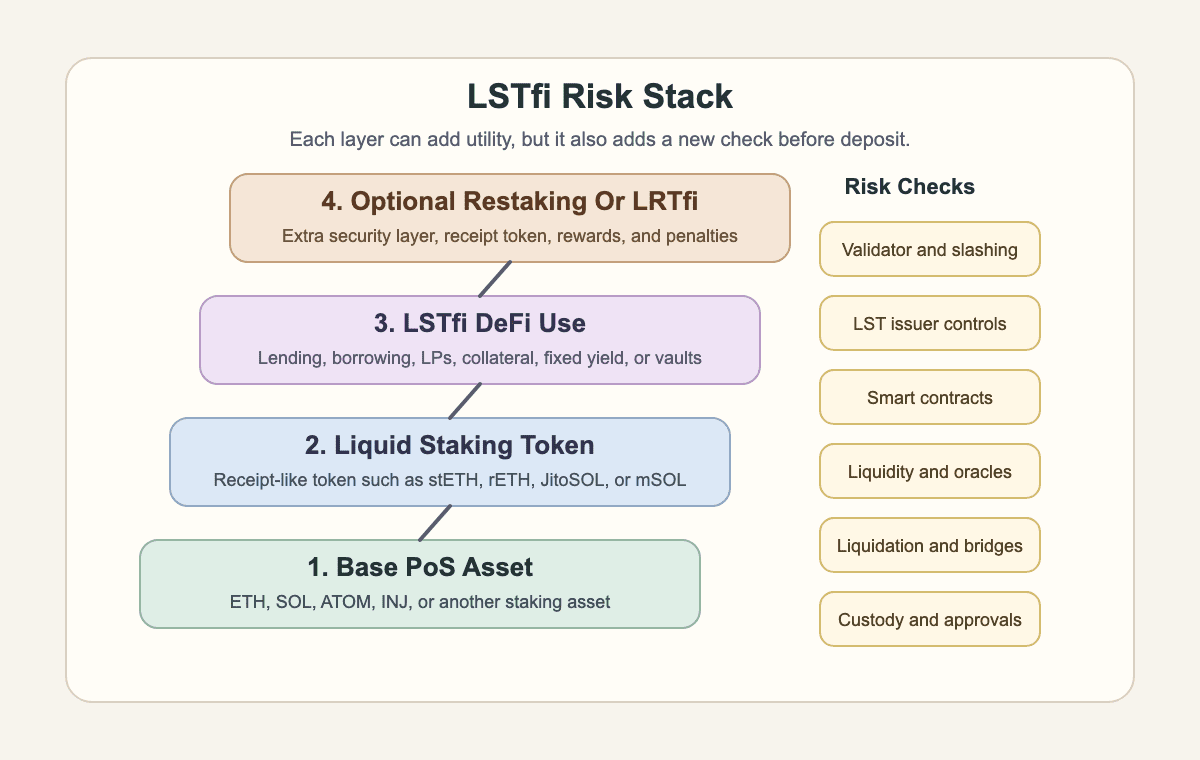

LSTfi starts when a staked asset becomes a transferable token. The user keeps staking exposure, but the position now has a token that can move through wallets, markets, and DeFi apps.

The base flow is easy to picture. A user stakes ETH, SOL, ATOM, INJ, or another proof-of-stake asset through a liquid staking route. The protocol issues an LST. The LST may reflect rewards through a changing exchange rate, a rebasing balance, or another token-accounting model.

Use the term map before the acronyms pile up.

| Term | What It Means |

|---|---|

| Native staking | The base asset is staked or delegated to help secure a proof-of-stake network. |

| Liquid staking | The user receives a transferable token that represents the staked position. |

| LST | The liquid staking token itself, such as a staking receipt or reward-bearing token. |

| LSTfi | DeFi use cases built around LSTs, including lending, collateral, LPs, and yield markets. |

| Restaking | Staked exposure is used to help secure additional services or networks. |

| LRTfi | DeFi use cases built around liquid restaking tokens, which add another layer above LSTs. |

The LST is the bridge between staking and LSTfi. Without that receipt-like token, there is no portable asset to use in a DeFi route.

The exit path also starts here. A user may sell the LST in a secondary market, redeem through the issuer, or unwind a DeFi position first. Those routes can behave very differently under stress.

So LSTfi should not be reduced to “staking, but more yield.” It is staking exposure plus a token wrapper plus DeFi use. Each layer needs its own answer before capital moves.

LSTfi protocols create extra yield by putting liquid staking tokens to work inside DeFi. The extra return may come from real market activity, temporary incentives, borrowed exposure, or a mix that looks cleaner on a dashboard than it feels during stress.

Start with the base reward. A liquid staking token may already track staking rewards from the underlying network. LSTfi then adds another source, such as lending income, liquidity-pool fees, collateralized borrowing, fixed-yield markets, yield tokenization, index products, protocol incentives, or points.

The yield source sets the failure mode.

| Yield Source | What Can Change |

|---|---|

| Base staking rewards | Network conditions, validator performance, fees, slashing, and protocol cuts can change returns. |

| Lending demand | Borrow rates can rise, fall, or vanish when demand changes. |

| Liquidity-pool fees | Fees depend on volume, pool depth, imbalance, slippage, and depeg stress. |

| Stablecoin minting | Collateral ratios, liquidation rules, oracle pricing, and redemption demand can change quickly. |

| Fixed-yield markets | Pricing depends on maturity, market depth, implied yield, and exit liquidity. |

| Incentives and points | Rewards may be temporary, delayed, diluted, or worth less than users hoped. |

| Borrowed loops | Leverage can lift returns, but it also tightens liquidation buffers. |

This is where yield farming can enter the picture. A user may supply an LST to earn rewards, points, or fee share. That can be legitimate. It can also become a rewards chase where the extra yield disappears before the risk does.

Protocols such as Pendle, Lybra, Prisma, Curve, and Aave show common patterns. Pendle-style markets can separate principal and yield. Lending markets can accept LSTs as collateral. Liquidity venues can pay trading fees. Stablecoin-style systems can let users mint debt against LST backing.

None of those routes are automatically passive income. The label may sound sleepy. The plumbing is not. The user still needs to know who pays the yield, what asset pays it, when it can change, and what happens if incentives stop.

The honest LSTfi yield check is simple: separate network rewards, user-paid fees, token emissions, points, and borrowed exposure. If the APY blends them into one shiny number, slow down.

LSTfi, LSTs, and LRTfi are related, but they are not the same layer. LSTs are the asset. LSTfi is the DeFi use case around that asset. LRTfi adds restaking exposure and usually more moving parts.

The confusion is understandable. The same wallet can hold stETH, use it as collateral, receive a restaked token, then deposit that token into another strategy. The labels pile up because the position does too.

Before comparing yields, name the layer. That habit prevents bad decisions dressed up as acronym fluency.

An LST is a liquid staking token. It represents staked exposure through a protocol, service, or smart contract route.

The user may hold the LST without doing anything else. In that case, the main checks are issuer design, validator exposure, reward accounting, redemption, liquidity, and custody.

LSTfi begins when the LST enters DeFi. The token may be lent, borrowed against, pooled, tokenized, used as collateral, or placed into a vault.

This layer changes the risk. The user now cares about smart contracts, oracles, collateral limits, liquidation thresholds, pool depth, and how the position can be unwound.

LRTfi appears when liquid restaking tokens enter DeFi. EigenLayer and Ether.fi are common examples in Ethereum discussions, but the important point is the added restaking layer.

An LRT can represent restaked exposure. Then LRTfi uses that token in DeFi. That means a position may depend on staking, the LST route, restaking rules, operators, reward programs, the LRT issuer, and the DeFi market.

This does not make LRTfi automatically worse. It makes it heavier. A heavier stack can still be useful, but the yield needs to pay for more risk.

LSTfi liquidity decides how hard a user can leave when conditions worsen. A liquid staking token can be transferable without being easy to exit at full value. “Liquid” is not a promise of deep markets, instant redemption, or zero slippage.

There are usually two broad exit paths. A user can sell the LST in a market, or redeem through the issuer if that route is open. DeFi use adds a third step because the user may need to withdraw collateral, repay debt, remove liquidity, or unwind a vault first.

> A discount does not always mean the LST is unbacked. It can also reflect exit queues, weak pool depth, market stress, redemption timing, or buyers demanding a bigger safety margin.

That is where exit liquidity becomes practical. If a pool is thin, a large sale can move the price. If everyone wants out at once, the first exits may be cleaner than the late exits. If a lending market prices the LST through an oracle, a market discount can also pressure collateral positions.

Depeg language can be misleading here. An LST is not always designed to trade at a hard one-to-one price every second. Some tokens accrue rewards through an exchange rate. Others may have wrapped versions. But a sharp discount can force a weaker sale and change what the position can recover right now.

A stressed LSTfi exit can create a chain reaction:

Inspect liquidity before depositing. Check market depth, redemption timing, withdrawal queues, oracle method, pool concentration, bridge route, and what happens if the token trades at a discount for longer than expected.

If the exit route only looks good on a quiet day, assume it may fail when conditions get loud.

LSTfi risks start with ordinary staking risk, then add token, protocol, market, and wallet risk. A position can lose money even if the underlying proof-of-stake network keeps running.

The risk stack begins at the validator layer. Poor validator performance, slashing, or issuer failures can affect the value behind an LST. Then DeFi adds smart contracts, collateral rules, oracles, liquidity, governance controls, and possible bridge exposure.

Use this checklist before treating any LSTfi route as “just staking.”

| Risk | What To Check Before Depositing |

|---|---|

| Validator or slashing risk | Who selects validators, how losses are handled, and whether risk is spread across operators. |

| LST issuer risk | Redemption rules, fees, token model, audits, admin controls, and incident history. |

| Smart contract risk | Audits, bug bounties, upgrade powers, dependency contracts, and public monitoring. |

| Oracle risk | How the LST is priced during discounts, market stress, or low-liquidity periods. |

| Collateral and liquidation risk | Borrow limits, health factors, liquidation thresholds, and repayment routes. |

| Liquidity and depeg risk | Pool depth, redemption timing, withdrawal queues, and secondary-market slippage. |

| Bridge exposure | Whether the token or strategy depends on a bridge, wrapped asset, or remote chain. |

| Custody and wallet risk | Wallet approvals, hardware-wallet support, signing flow, and fake front-end risk. |

| Tax and records | Swaps, rewards, deposits, redemptions, sales, borrow events, and local reporting rules. |

| Incentive unwind risk | Whether yield depends on points, token emissions, or campaigns that can fade. |

Custody deserves more attention than it usually gets. LSTfi users may sign approvals, interact with several contracts, bridge assets, and manage a position from a hot wallet. Treat wallet setup as part of the risk stack, not just where the token sits.

A clean setup can reduce obvious mistakes, but it does not make the strategy safe by itself. Position size is another risk control. A small spot position in an LST is not the same as an LST used as collateral in a borrowed loop. The second position has a liquidation clock. It may need fast action when markets are already rude.

Tax treatment also varies by country, so this cannot replace local advice. The recordkeeping point is simple. Track deposits, swaps into LSTs, rewards, sales, redemptions, borrow events, and liquidations. The spreadsheet is boring until you need it. Then it becomes suddenly charming.

The strongest LSTfi risk habit is naming every layer. If you cannot identify the base asset, issuer, contracts, oracle, collateral rules, exit path, and custody setup, the yield number is ahead of the homework.

LSTfi is not only for Ethereum, but Ethereum is the main reference point for many users. Most well-known LSTfi examples, search results, and restaking comparisons still lean heavily toward ETH, stETH, rETH, and related DeFi markets.

That makes Ethereum the clean teaching example. ETH has deep staking culture, large liquid staking brands, lending markets, liquidity pools, restaking routes, and a lot of acronym debris for users to step around.

But the LSTfi pattern can appear anywhere liquid staking tokens are accepted in DeFi. Solana users may see JitoSOL or mSOL. Cosmos-style networks, Injective, and other proof-of-stake systems can also support liquid staking tokens and DeFi integrations, depending on the chain and app design.

The chain changes the checklist. On Ethereum, users may focus on LST issuer quality, lending markets, restaking links, and gas costs. On Solana, Cosmos, or another network, users may focus on validator set design, DEX liquidity, wallet support, bridge routes, app maturity, and redemption flow.

So the answer is broader than one chain. LSTfi is a category. Ethereum has the loudest examples, but the logic follows the token. If a liquid staking token can move into DeFi, an LSTfi-style strategy can exist around it.

The key is not the chain logo. It is whether the LST has real backing, clear redemption, useful liquidity, and DeFi integrations that you can inspect without needing a detective board.

Evaluating an LSTfi strategy means separating the base staking position from the DeFi strategy layered on top. The goal is to know what you hold, what can change, and how you leave.

Start with the boring questions. They are the ones that save money. What asset is staked? Who issues the LST? How does the token reflect rewards? Can you redeem directly? Where can you sell? What contracts, bridges, or oracles sit between entry and exit?

Run the checklist before sizing up:

Then test small. A small deposit can reveal signing steps, token receipt behavior, withdrawal timing, reward display, and dashboard quirks before real size enters the position.

Position sizing belongs here too. A complex LSTfi stack is a poor place for a first run at full size. Even if the strategy is sound, a crowded exit, oracle update, or temporary depeg can punish size faster than a calm thesis can explain it.

The standard is not perfection. Crypto rarely offers that. It is whether you can explain the strategy, monitor the weak points, and exit without relying on one friendly market condition.

If the answer is no, the strategy may still be interesting. It just belongs in the watchlist, not the wallet.

LSTfi gets easier once the nearby concepts are separated. Liquid staking creates the transferable staking receipt. LSTfi puts that receipt into DeFi. Restaking and LRTfi add another security layer and another tokenized claim.

Yield farming explains why some LSTfi routes pay incentives or points. Exit liquidity explains why a token can be tradable but still hard to sell cleanly under stress. Wallet custody explains why approvals, hardware wallets, browser safety, and contract permissions matter when the strategy spans several apps.

Position sizing ties those ideas together. A user holding a small LST balance has one risk profile. A user borrowing against that LST, looping it, bridging it, and chasing points has a different profile, even if the asset ticker looks familiar.

The related terms are not trivia. They are the control panel. If you understand the LST, the yield source, the exit route, and the custody setup, LSTfi becomes much less foggy.

For this path, two next stops help:

If those pieces still feel vague, stay with plain staking or simple liquid staking until the route makes sense. Missing a few points of yield is cheaper than learning the acronym after the liquidation.

No. LSTfi is not one cryptocurrency. It is a category of DeFi activity that uses liquid staking tokens.

Some tokens, protocols, or tickers may use similar letters, but the term usually refers to liquid staking token finance. Call it a strategy category until a specific asset is named.

Liquid staking creates the LST. LSTfi uses that LST inside DeFi strategies.

For example, holding an LST after staking is liquid staking exposure. Supplying that LST to a lending market, liquidity pool, stablecoin system, or fixed-yield market moves into LSTfi.

LSTfi uses liquid staking tokens. LRTfi uses liquid restaking tokens, which usually add restaking exposure above the staking layer.

That extra layer can add reward paths, but it can also add operator, restaking, slashing, withdrawal, and token-wrapper risk. The acronyms are close. The stacks are not identical.

Yes. An LSTfi position can lose money through token price moves, slashing, smart contract bugs, thin liquidity, depegs, liquidations, bridge failures, bad approvals, or tax friction.

The highest-risk version is usually not simple holding. It is an LSTfi position that adds borrowing, looping, cross-chain exposure, or collateral rules that can force an exit.

If a liquid staking token depegs, it trades below the value users expect from its backing or redemption route. That can create losses for sellers and stress for collateral users.

A depeg does not always prove the LST is unbacked. It can reflect exit queues, weak liquidity, market panic, or uncertainty. Still, a discount can force a faster sale, tighter borrowing terms, or a rushed liquidation step.

LSTfi can create taxable events depending on your jurisdiction and the exact transaction. Swaps, staking receipts, rewards, sales, redemptions, borrow-related events, and liquidations may be treated differently.

Do not guess from a dashboard. Keep records for each step and check local rules with a qualified tax professional, especially before using larger positions or multi-protocol strategies.

Start with the LST, not the yield. If you do not understand how the staking token is issued, backed, rewarded, redeemed, and traded, the DeFi layer is already too early.

Go in layers, not in excitement. First confirm the staking token behavior, then confirm the strategy behavior, and only then size the position.

Use this practical start order:

If a strategy fails this checklist on paper, stop there and keep the position in plain staking mode for now. If it passes, start with a small test size and run through one full cycle, including unwind steps, before adding size.

Then move through the strategy in plain order:

Keep the first attempt boring. Use one chain, one wallet, one strategy, and one exit route you can explain. Complexity should earn its place.

LSTfi can be useful when it turns staked exposure into productive DeFi collateral without hiding the risk. It becomes dangerous when the only clear part is the APY.

Extra yield is not a personality trait. Make it pass the checklist first.