Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Learn how low float, high FDV can hide dilution risk.

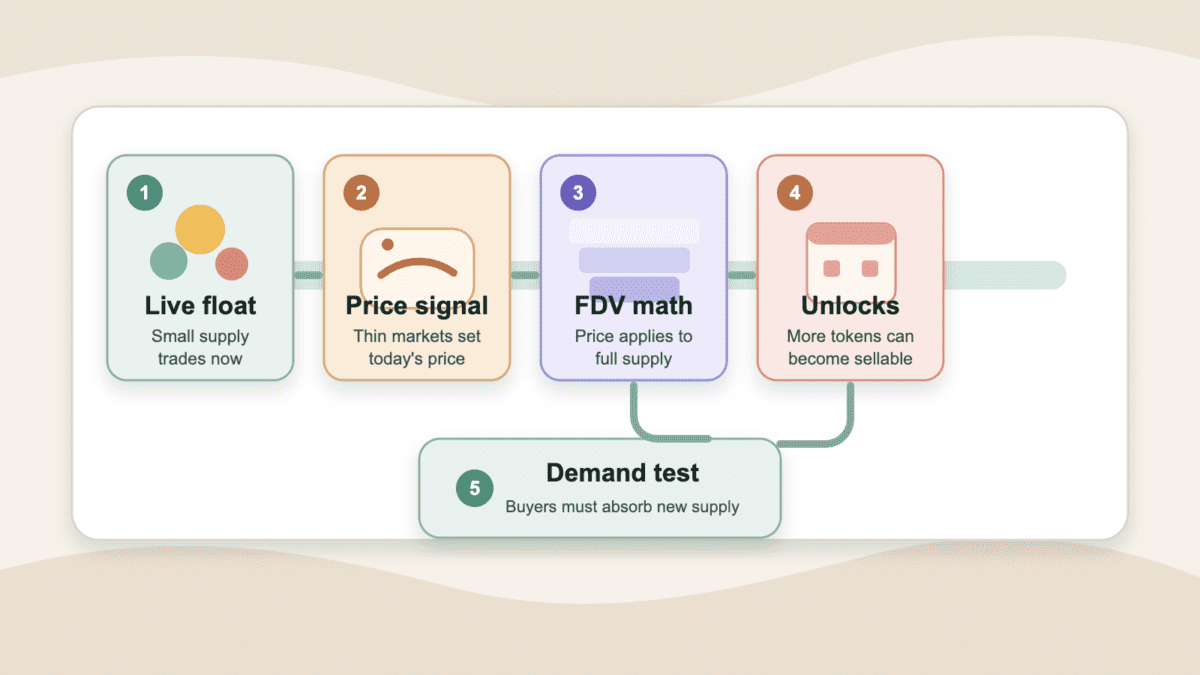

In crypto, low float, high FDV means only a small share of a token trades today while the current price implies a much larger full-supply value.

That gap explains why the phrase keeps showing up on social feeds, exchange listings, and token unlock dashboards. It does not prove a scam by itself. It tells you to compare the live market with the supply that may hit later.

The term is useful because it slows down a very common mistake: treating a cheap-looking market cap as proof that the token is actually cheap.

When a token already prices future supply the market cannot realistically absorb, the risk sits in the structure, not trader mood.

Low float, high FDV in crypto describes a token with small tradable supply and a large implied full-supply valuation. Float means the tokens that can actually trade now. FDV means fully diluted valuation: the current token price multiplied by the full token supply used for valuation.

That sounds abstract until the numbers meet a launch chart. Suppose a token trades at $0.10 with 100 million tokens circulating. Its circulating market cap is $10 million. If the project has 10 billion tokens in total, the FDV is $1 billion.

So the public market may see a $10 million token. The full supply says the market is already pricing a $1 billion project.

That mismatch is the point. A low-float token can look small and early because only a limited public slice is trading. But once the same price is applied to future team, investor, treasury, and incentive supply, the implied valuation can already be ambitious.

The phrase became popular because many new tokens launched with tiny public floats, large locked allocations, and high implied valuations. Traders started using low float, high FDV as shorthand for a simple warning: the visible market may not be the whole market.

It is a warning signal, not a verdict. A strong project can launch with locked supply and still grow into its valuation. A weak one can use a small float to create the illusion of scarcity while future supply waits quietly in the wings.

Low float, high FDV differs from market cap because market cap only values the supply currently counted as circulating. FDV estimates what the token would be worth if the full supply carried the same price.

That split is sharpest near launch. A token can have a small circulating market cap, a low unit price, and still carry a full-supply valuation that already assumes major success. The cheap-looking price is often the least useful number on the screen.

Here is the clean split:

| Metric | What It Tells You |

|---|---|

| Token Price | The current market price for one token |

| Circulating Supply | The token supply counted as live and tradable now |

| Market Cap | Token price multiplied by circulating supply |

| Max Or Total Supply | The wider supply used to estimate future dilution |

| FDV | Token price multiplied by max or total supply |

| Market Cap To FDV Ratio | How much of the full valuation is already circulating |

A simple ratio helps here. If market cap is $100 million and FDV is $1 billion, the market cap to FDV ratio is 0.10. Only about one-tenth of the implied full valuation sits in circulating market cap.

CoinGecko Research defines low float in its top-300 study as a market cap to FDV ratio from 0 to 0.49. It found that 21.3% of the top 300 crypto assets by market cap fell into that low-float bucket in its updated study. The same update reported that only 24.7% of the top 300 were fully diluted. That is another reason to read the ratio before trusting a cheap-looking market cap.

Use the ratio as a starting point, not a verdict. A low ratio tells you to inspect the unlock schedule, recipients, liquidity, and demand. It cannot tell you whether the token goes up tomorrow.

Low float, high FDV tokens can pump first because the tradable supply is small. When a token has limited float and enough launch attention, even moderate demand can move the price quickly.

That early move can feel like proof that the market loves the project. Sometimes it is. But thin liquidity, small order books, airdrop demand, listing hype, and reflexive buying can also do the heavy lifting.

Launch-day pumps often come from a few ingredients working together:

That is when normie inflow can add fuel. Public demand may arrive after a listing, a viral chart, or a simple story that spreads faster than the tokenomics.

Low float can amplify upside, but it also amplifies the reversal. If the price rises on shallow liquidity, sellers do not need huge size to move it down later. The chart can look strong while the market beneath it is still ankle-deep.

So a launch pump should lead to better questions. How much supply is actually liquid? Who owns the rest? When does it unlock? And can the market absorb selling without turning the chart into a very expensive lesson?

Low float, high FDV unlocks create dilution risk because more tokens can become available after the market has already priced the smaller float. The risk is new supply meeting weak demand.

Locked supply can belong to teams, investors, treasuries, market makers, foundations, advisors, or incentive programs. Some allocations unlock in one cliff. Others release linearly over months or years. Either way, the market must decide who absorbs the added supply.

An unlock does not mean every recipient sells immediately. Teams may hold, investors may have longer horizons, and treasuries may distribute supply through grants or rewards. But more available supply changes the risk because more holders gain the option to sell.

Use this unlock signal table before assuming the schedule is harmless:

| Unlock Signal | Why It Changes The Risk |

|---|---|

| Next Unlock Size | A large release can pressure price if demand is thin |

| Recipient | Team, investor, treasury, and incentive supply carry different selling incentives |

| Cadence | Cliffs can shock the market, while linear releases can create steady pressure |

| Market Depth | Thin books or pools make new selling harder to absorb |

| Demand Evidence | Usage, fees, volume, or real buyers help offset added supply |

The painful version happens when public buyers hold the live float while earlier, cheaper, or locked holders gain liquidity later. That can create the classic bagholder trap: late holders keep waiting while better-positioned supply finds exits.

The fix is simple, if not always pleasant. Read the unlock calendar before buying. Then compare each future release with volume, liquidity, and the reason anyone would still want the token when that supply arrives.

Low float, high FDV becomes a real red flag when the token needs perfect future demand just to justify the launch valuation. Fragile assumptions leave buyers with little room for error.

The strongest warning signs come in clusters. A low circulating percentage alone may be manageable. A low circulating percentage, giant FDV, near-term cliffs, weak usage, thin liquidity, insider-heavy allocation, and loud paid hype is a different beast entirely.

Watch for these red flags before making market cap the main number:

That is when exit liquidity risk becomes more than a meme insult. If the public market mostly exists to absorb supply from earlier holders, the setup is structurally unfriendly to late buyers.

Still, keep the accusation precise. Low float, high FDV is not the same as a hard rug, where liquidity disappears, selling is blocked, or the project fails through direct abuse. It is usually a valuation and supply risk first.

The red flag becomes stronger when the team sells optimism while hiding the supply math. A good project can explain float, FDV, vesting, and demand clearly. A weak one hopes you stare at the green candle instead.

Low float, high FDV is not automatically fatal when the locked supply is transparent, long-dated, and matched by real demand. Risk can be priced. Hidden or ignored risk usually cannot.

Some projects start with small float because they need vesting, grants, security budgets, liquidity programs, or long-term contributor incentives. That structure can be reasonable when the schedule is clear and the valuation has not run far ahead of usage.

Better setups usually share several traits:

There is also a difference between a risky structure and abusive behavior. A low-float token can disappoint without being a soft rug. A soft rug involves slow value extraction, fading delivery, or insider behavior that keeps hope alive while exits worsen.

“Not fatal” does not mean “cheap.” It only means the structure needs evaluation. If the project must grow perfectly for years just to make the FDV look sensible, you are not early because the unit price has extra zeros.

Ask what would make future holders want the token after each unlock. If the answer is only “more hype,” the risk is still doing push-ups in the corner.

To check low float, high FDV before buying, compare market cap, FDV, unlocks, recipients, liquidity, holder concentration, and demand in one pass. One attractive number should not do the thinking.

Start with the market cap to FDV ratio. A low ratio tells you that much of the implied valuation sits outside the live circulating supply. Then read the unlock schedule and ask who gets supply next.

The check is short, but each step needs a real answer:

This table keeps the workflow grounded:

| Question | What It Changes |

|---|---|

| What Is The Market Cap To FDV Ratio? | It shows how much supply is still outside the live market |

| When Is The Next Unlock? | Timing can turn future dilution into near-term pressure |

| Who Receives The Tokens? | Teams, investors, and incentive programs have different motives |

| How Deep Is Liquidity? | Thin books can make even modest selling move price |

| What Supports Demand? | Usage, fees, volume, or adoption help absorb supply |

| What Would Break The Thesis? | A clear invalidation point prevents hope from replacing analysis |

The last row is where a conviction play differs from blind holding. Conviction needs evidence that can survive new supply. It is not a vibe with a vesting cliff.

Do not stop at one dashboard. Coin listings, unlock trackers, project tokenomics pages, block explorers, exchange order books, DEX pools, and holder data each show a different part of the risk. The strongest signal appears when several sources point to the same concern.

And be careful with unit price. A token at $0.02 can still be expensive if the full supply implies a huge FDV and future demand is thin. Cheap per token is not the same as cheap ownership.

Low float, high FDV tokens differ from fair launches and memecoins because future supply overhang is usually the central concern. In a fairer launch, more supply may trade from the start.

That is why some traders prefer fully circulating tokens. They would rather face open-market chaos than hidden vesting cliffs. It is a reasonable preference, but it does not make every fair launch safe.

The tradeoff looks like this:

| Launch Style | Main Tradeoff |

|---|---|

| Low Float, High FDV | Smaller live supply can support price, but future unlocks can dilute holders |

| Fair Launch | More open access can reduce insider overhang, but bots may dominate early trading |

| Launchpad Token | Distribution can be organized, but allocations and vesting still need checking |

| Memecoin | Supply may be fully circulating, but demand can vanish fast |

| Community Relaunch | Holders may coordinate recovery, but liquidity and trust may already be damaged |

Memecoins need their own warning label. A fully circulating meme token may avoid future team or investor unlocks, but it can still carry bundled wallets, bot sniping, fake volume, thin pools, paid promotion, and demand that vanishes fast.

That is the difference from many VC-backed launches. Meme-token risk often comes from speed, liquidity, wallet behavior, trading in the trenches, and attention decay. Low float, high FDV risk usually comes from valuation, locked supply, and future sell pressure.

Neither model is pure. Some VC-backed tokens have fairer public terms than their critics admit. Some fair launches are basically chaos with a logo. The useful move is to inspect the supply, liquidity, and incentives instead of picking a tribe.

Low float, high FDV sits near several crypto terms that describe different parts of the same risk cycle. Keeping them separate makes the warning sharper and prevents every bad token launch from becoming one vague accusation.

Exit liquidity describes demand that lets someone else leave a position. It is the social fear behind many low-float complaints, especially when earlier holders have cheaper entries.

A bagholder describes the person left holding after the easy exit has passed. In low-float tokens, that can happen when public buyers ignore future supply and keep waiting after unlock pressure changes the market.

Soft rug describes slow value extraction or trust decay. It can overlap with low-float launches, but it is not the same thing. A token can have weak tokenomics without proving insider abuse.

Hard rug is different again. That term belongs to more direct destructive behavior, such as removed liquidity or blocked selling. Low float, high FDV is a supply and valuation structure first.

Fair launch is the cleaner comparison term when the debate is about access. A fair launch may reduce insider overhang, but it can still leave users with thin liquidity, bot-heavy trading, or a token that has no demand once the first rush fades.

Keep the terms separate. Exit liquidity describes who buys the sell pressure. Bagholder describes who gets stuck after the move. Soft rug and hard rug describe different kinds of project failure. Low float, high FDV describes the supply and valuation setup that can make those outcomes easier to miss.

Low float, high FDV is not automatically a scam. It describes a token supply and valuation setup, not proof of fraud, theft, or bad intent.

The risk becomes more serious when a project hides vesting, relies on hype, has thin liquidity, and lets insiders sell into public demand. That pattern can be abusive even if the phrase itself is only a warning.

Low float, high FDV tokens can dump after launch because early price action is often built on small tradable supply and thin liquidity. When demand cools or more supply unlocks, the market has to absorb more selling pressure.

The dump is not always caused by fraud. It can come from airdrop selling, investor unlocks, weak demand, poor liquidity, or buyers realizing the FDV was already stretched.

A higher market cap to FDV ratio usually means less future supply overhang. A ratio near 1 means the token is close to fully diluted, while a very low ratio means much of the supply is still outside circulation.

There is no universal safe number. A low ratio needs extra checks around unlock timing, recipients, liquidity, and demand. A high ratio can still be risky if the token has no real market.

Circulating supply is too low when the live float is small enough that price discovery feels artificial and future unlocks could overwhelm normal demand. The exact line changes by token.

As a rough check, compare circulating supply with total supply, then compare the next unlock with trading volume and liquidity. A small float with deep demand is different from a small float propped up by one loud launch week.

Yes, a low float, high FDV token can still go up if demand grows faster than future supply pressure. Strong usage, deep liquidity, transparent vesting, and reasonable valuation can support a token through unlocks.

But upside does not erase dilution risk. If the price already assumes a large future valuation, the token needs real demand to keep proving the market right.

Memecoins are not automatically safer than low float, high FDV tokens. A fully circulating supply can remove future unlock risk, but it does not remove liquidity risk, wallet concentration, fake volume, or demand collapse.

The safer setup is the one you can actually understand. Check supply, ownership, liquidity, and the reason people would keep buying after the first hype wave fades.

Start with low float, high FDV by refusing to read market cap alone. The token’s live valuation is only half the picture when future supply is still waiting to trade.

Then make the unlock schedule part of the first read, not a cleanup step after you already bought. A token can survive a large FDV when the schedule is transparent, liquidity is deep, and demand has a real reason to keep showing up.

Also decide what you need to see before the next unlock. That could be deeper liquidity, clearer recipient behavior, stronger usage, or a valuation that moves closer to peers. If the answer is only another influencer thread, the trade is leaning on attention, not demand.

Run these checks before buying or holding through an unlock:

After that, compare the answer with your time horizon. A short-term trader may care most about the next cliff and order-book depth. A long-term holder needs the full vesting path, recipient incentives, and evidence that the token can still earn attention after the launch glow fades.

If those answers are clear, you can evaluate the risk with open eyes. If they are missing, vague, or buried under hype, that is the market telling you something before the chart does.