Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A clear guide to infra coins, INFRA ticker confusion, and token risk.

An infra coin is a cryptocurrency tied to blockchain infrastructure, such as networks, oracles, data layers, RPC services, wallets, storage, compute, payments, or cross-chain rails.

The phrase usually describes a broad category, not one official asset class. Uppercase INFRA can also refer to a specific ticker, including Bware’s INFRA token. So before trading anything with that name, verify the exact chain, contract, market, and liquidity.

Infrastructure can sound serious. Sometimes it is. But a serious service can still have a weak token attached to it, which is where the expensive mistakes usually begin.

An infra coin in crypto is a coin or token connected to the systems that help blockchains, apps, wallets, and markets run. It can sit behind transaction processing, data feeds, storage, compute, developer access, cross-chain movement, payments, or user security.

The phrase is community shorthand. It is not a legal category, a rating, or proof that the token has durable demand. Traders often use it when they want exposure to the “picks and shovels” side of crypto instead of a meme, game, or single app.

That broad label covers very different assets:

The label is useful when it points to a real job. An infra coin should support something other crypto users, builders, or apps need. The risky part is the gap between “the service is useful” and “the token captures value.”

Follow that gap closely. A project can provide real infrastructure while customers pay in stablecoins. Fees may flow to operators, emissions can dilute holders, or the token may have only a loose governance role. The hard work is finding out what the coin actually does inside the system.

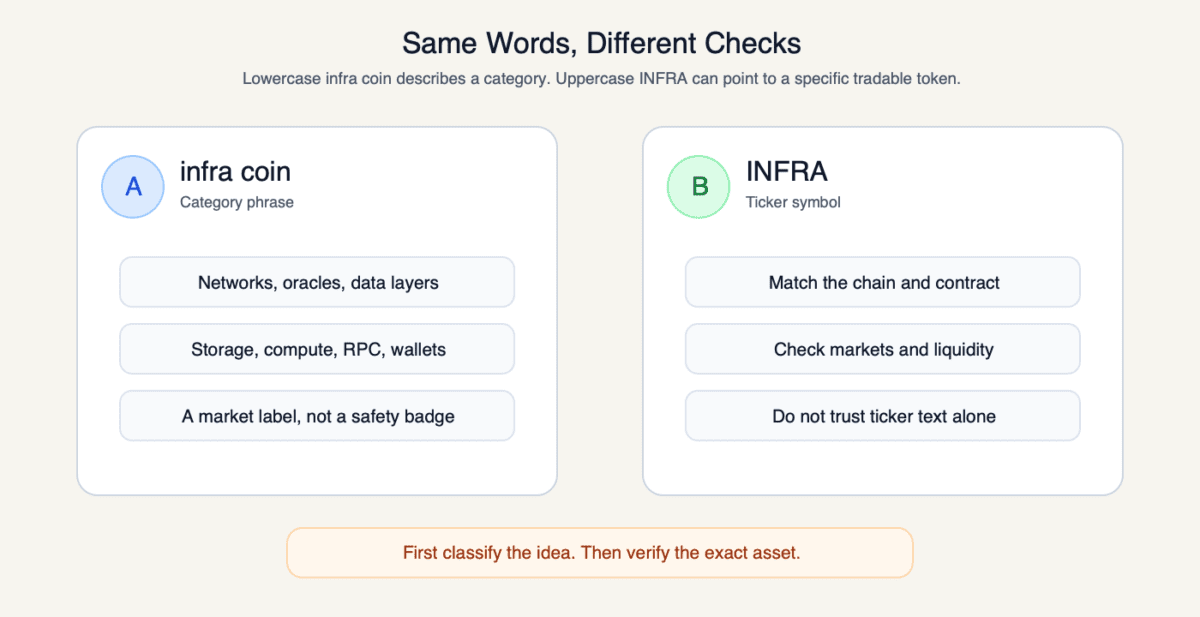

Infra coin and INFRA token can mean different things. Lowercase “infra coin” usually means a broad infrastructure category, while uppercase INFRA is a ticker symbol that can point to one specific asset or to unrelated assets using similar names.

Bware is one example of that ticker confusion. On June 21, 2026, CoinGecko listed Bware with the INFRA ticker, contract details, and $28.67 in 24-hour trading volume. That verifies one asset, not every INFRA-looking page.

Ticker text is weak identity. Many tokens can share a symbol. Copycat contracts can also use familiar words to look safer than they are. The asset identity comes from the official source, chain, contract address, explorer record, market pair, and liquidity venue.

Use this split before you react:

Keep the split simple. Category language helps users understand the theme. Ticker language needs verification before a wallet signs or an exchange order goes live.

An infra coin counts as infrastructure when the asset is tied to a system other projects or users rely on. That can mean the base network, the data layer, the access layer, the storage layer, or the tools that help people move and protect assets.

The same coin can sit in more than one bucket. Ethereum is a base network and settlement layer. Chainlink is often discussed as oracle infrastructure. Celestia is tied to data availability. Filecoin and Arweave point toward storage. Render and Akash point toward compute.

None of those labels turns the token into a buy list.

Use function first, branding second:

| Infrastructure Function | What The Coin Or Token Is Trying To Support |

|---|---|

| Layer 1 network | Blockspace, settlement, security, and transaction fees. |

| Layer 2 network | Cheaper or faster execution on top of another chain. |

| Oracle | External prices, events, and data for smart contracts. |

| Data availability | Data publication for rollups and modular chains. |

| RPC and node services | Developer access to blockchain data and transaction submission. |

| Storage and compute | Decentralized files, hosting, GPU work, or cloud-like resources. |

| Cross-chain messaging | Asset movement, messaging, or coordination between chains. |

| Wallets and payments | User access, signing, account tools, and payment rails. |

This table is a sorting tool, not a ranking system. A token can look like infrastructure because it uses serious words. The real check is whether users need the network and whether the token has a meaningful role inside it.

Some infrastructure tokens support builders directly. Others support traders, validators, wallets, app chains, data consumers, or end users who never see the plumbing. That hidden role can be valuable, but it can also make token value harder to trace.

Traders like infra coins because they offer a clean story: if crypto keeps growing, the tools underneath it should benefit. That “picks and shovels” idea is easy to understand. It is also much easier to repeat than a dense protocol design.

The story can also feel more serious after meme fatigue. A token tied to oracles, data availability, compute, storage, or scaling sounds like a business case with fewer cartoon hats. The chart may still behave like an altcoin with a helmet on.

Infra coins often attract attention for several reasons:

That rotation is where narrative coin risk shows up. An infra coin can rise because traders believe infrastructure is the next category to catch bids, not because the project just proved fresh demand.

The broader crypto meta also shapes the move. AI compute, DePIN, data availability, L2 scaling, and cross-chain tooling can each become the market’s favorite infrastructure story for a while.

But narratives can outrun usage. If the token moves only because the label is hot, the trade can become crowded before the product catches up. Good infrastructure stories still need one plain check: who actually needs the token?

A useful project can still be a weak infra coin when the token does not capture enough value from the service. The infrastructure may work. Customers may use it. Builders may respect it. The token holder can still get diluted, ignored, or used as someone else’s exit.

Value capture is the main issue. Fees may go to node operators, validators, a treasury, stablecoin payments, cloud bills, or service providers. If the token is not required for payment, security, collateral, staking, burns, buybacks, or meaningful governance, its link to product usage can be thin.

Good signs usually connect the token to actual demand:

Red flags point the other way:

This is also where exit liquidity risk enters. A credible infrastructure story can bring late buyers after early holders already have large gains, vesting supply, or better information.

The difference between an infra coin and a utility token can be subtle. A utility token has a defined role inside a system. An infra coin is a broader market label. A token can be both, but the role has to be real enough to survive beyond a slide deck and a staking page.

After “the project is useful,” ask the duller question. How does usefulness become token demand? Who pays? Who receives value? What new supply is coming? That is where many impressive-sounding tokens get less impressive.

Checking an infra coin before you buy means looking past the category label and reading the market structure. You want to know whether the asset has real use, enough liquidity, a fair supply setup, and a token role that makes sense.

Start with the boring numbers. Boring is good here. Market cap, FDV, circulating supply, volume, spread, exchange support, unlock schedule, and holder concentration tell you whether the trade can absorb normal buying and selling pressure.

Use this checklist before trusting the story:

| Check | What It Tells You |

|---|---|

| Market cap and FDV | Whether current float hides a much larger future valuation. |

| Circulating supply | How much supply can trade today. |

| Token unlocks | Whether new supply may hit the market soon. |

| Volume and spread | Whether entry and exit are likely to be clean. |

| Exchange depth | Whether the market is active beyond one thin venue. |

| Holder concentration | Whether a few wallets can dominate selling pressure. |

| Product status | Whether the infrastructure is live or mostly promised. |

| Token role | Whether users need the coin, or only the brand does. |

| Revenue or fees | Whether usage has measurable economic weight. |

| Developer and customer activity | Whether builders still care after the first launch cycle. |

A cheap unit price is not a bargain by itself. A token at a few cents can still be expensive if FDV is high, float is low, liquidity is shallow, and unlocks are waiting around the corner.

Also check whether the project is still alive. A token can keep trading after the product stalls, the market thins, or the team stops shipping. That is where dead coin risk becomes relevant even for respectable infrastructure labels.

The best pre-buy check is a plain sentence: “This token captures value because…” If the answer depends on vague future adoption, influencer conviction, or a tracker category, risk is still doing most of the talking.

Verifying an INFRA coin contract and market means proving that the asset in front of you is the intended token, on the intended chain, with real liquidity. A ticker alone is not identity.

Start from the strongest source available. Use the official project site, then a major tracker, then the block explorer, then the exchange or DEX market. The contract address, chain, symbol, token name, market pair, and explorer page should all agree.

Before importing or swapping, check these items:

If you manually add a token to a wallet, slow down. Basic wallet setup discipline helps here: use official links, test with small size, avoid random import prompts, and review approvals after any risky interaction.

Keep the warning short. INFRA text on a page does not prove Bware. An infra coin label does not prove a safe market. Contract, chain, and liquidity checks do the real work.

When anything conflicts, pause. A different chain, a mismatched contract, thin liquidity, a weird explorer record, or a pool with almost no activity is enough reason to step back.

Infra coin examples are most useful when grouped by function. A ranked list can make every token look comparable, but infrastructure categories solve very different problems.

Use examples as teaching aids, not endorsements. Chainlink, Ethereum, Solana, Celestia, Arbitrum, Filecoin, Arweave, Internet Computer, Render, Akash, Hedera, and XRP-related payment rails can all appear in infrastructure conversations. The reasons are different, which is the point.

The cleaner grouping looks like this:

One token can touch more than one function. A network might support payments and smart contracts. A compute project might also be part of an AI narrative. A DePIN project might have infrastructure use and speculative category demand at the same time.

Examples should not become a leaderboard. Do not ask which infra coin is best from the label alone. Ask what infrastructure job the asset claims, whether the product is live, and whether the token captures the demand it points to.

Infra coin risks often hide behind serious language. The label can make a speculative altcoin feel sturdier than it is, especially when the project talks about nodes, validators, data, enterprise users, or developer tools.

The main traps are not exotic. They are liquidity, supply, value capture, copycat tickers, and products that sound more live than they are. Crypto has a special talent for making unfinished plumbing look like a skyscraper lobby.

Watch these risks closely:

Slow abandonment deserves its own note. When updates fade, delivery weakens, liquidity thins, and holders keep waiting for “the real launch,” the pattern can start to resemble soft rug signs without one dramatic collapse.

Infra coins are not automatically safer than meme coins. They may have more technical substance, but they still carry altcoin risk, market-cycle risk, liquidity risk, and token-design risk.

That does not make the category useless. It means the serious story should raise your standards, not lower your guard.

Infra coin terms help users separate the infrastructure story from the token risk. The goal is not to memorize jargon. The goal is to ask cleaner questions before money gets involved.

Narrative coin describes a token whose demand is strongly shaped by a market story. Infra coins can become narrative coins when traders chase the infrastructure theme before usage proves the token’s role.

Crypto meta is the broader market playbook. When infra becomes the meta, attention can spread across oracles, L2s, data availability, compute, DePIN, and storage even when those projects have different economics.

Exit liquidity means late buyers give earlier holders a way out. It can happen in serious categories too, especially when vesting supply, crowded narratives, and thin order books meet at the wrong time.

Dead coin risk is the chance that a token stays visible on trackers while product activity, market depth, and community interest decay. Wallet setup is the safety layer around contract imports, approvals, and custody mistakes.

Translate the terms into actions before you trust them:

These terms help most when they slow the trade down. If a phrase makes the asset sound inevitable, translate it into a check: product live, token needed, supply known, liquidity real, contract verified.

That habit keeps the core distinction intact. Infrastructure can be real, but the token still needs proof. A good phrase should make research sharper, not standards softer.

INFRA coin can refer to Bware’s INFRA token. The phrase can also be used loosely for other assets or for infrastructure coins as a category.

Check the official source, chain, contract address, tracker page, explorer, and market pair before assuming any INFRA ticker is Bware. Same symbol does not mean same asset.

Infra coins can have more technical substance than meme coins. They are not automatically safer.

They still face altcoin risk, liquidity risk, unlock pressure, weak token value capture, and market narratives that can reverse quickly. Serious branding is not a risk control.

An infra coin can go down when product usage does not create enough token demand. New supply, weak liquidity, or a crowded narrative can also overwhelm buyers.

The project may keep serving customers while the token struggles. That can happen if fees bypass the token, emissions dilute holders, or early holders sell into later demand.

Check an INFRA coin contract by matching the official project link, tracker page, chain, contract address, explorer record, and market pair.

Do not rely on the ticker alone. If the contract, chain, or liquidity venue does not match, pause before importing the token or signing a swap.

Useful infra coin examples include oracles such as Chainlink, L1s such as Ethereum and Solana, data availability projects such as Celestia, and storage or compute projects such as Filecoin, Arweave, Render, and Akash.

Use them as category examples, not as a buy list. The key question is what job the infrastructure performs and whether the token captures real demand from that job.

Start with classification, not a buy button. Decide whether you are looking at a broad infrastructure category, a specific INFRA ticker, or a token borrowing the same words to look credible.

Then work through a short process:

The best infra coin research feels a little slow. That is fine. Infrastructure tokens are sold with big, serious words, and big words are cheap.

A good asset should survive simple questions. What does it support? Who uses it? Why does the token need to exist? Can you enter and exit cleanly? If those answers are fuzzy, the infrastructure label is not doing enough work.

You can also separate research from timing. A token can be worth watching while still being too thin, too crowded, or too unclear for your own risk. Keeping a watchlist is different from forcing a position.

If the checks improve later, you can revisit the idea with better information. If they do not, you avoided buying a serious-sounding label with a weak market behind it. That is a good outcome too.